TFSA vs RRSP vs FHSA: Which Account Should You Open First?

Five real scenarios — from new grad to high-income couple — with the tax bracket math that shows exactly which account order maximizes your refund.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

Choosing between TFSA, RRSP, and FHSA comes down to your homebuying plans and tax bracket.

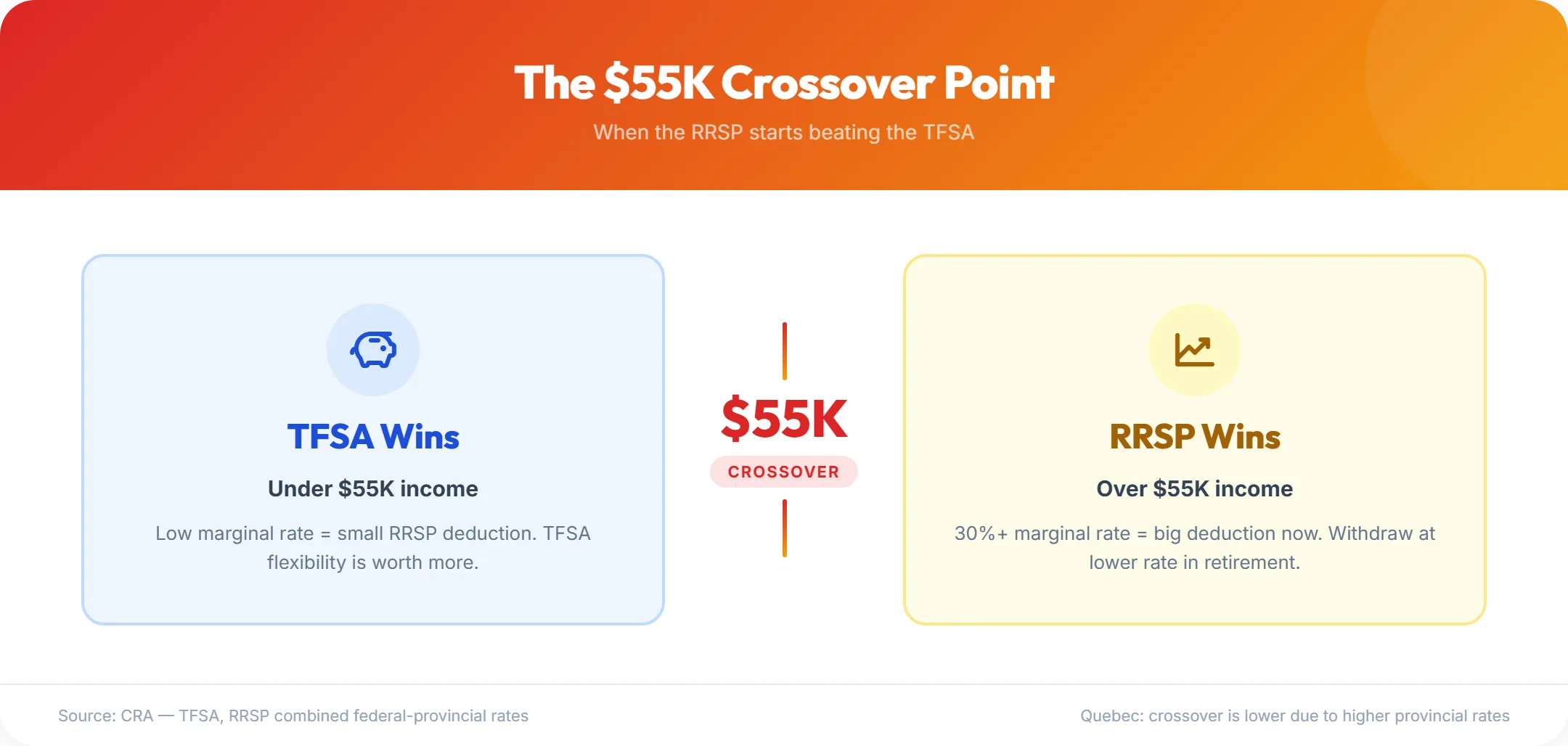

The Bottom Line: Open the FHSA first if you might buy a home within 15 years. Otherwise, TFSA wins under ~$55K income and RRSP wins above it. All three have independent limits — you can contribute to all of them in the same year.

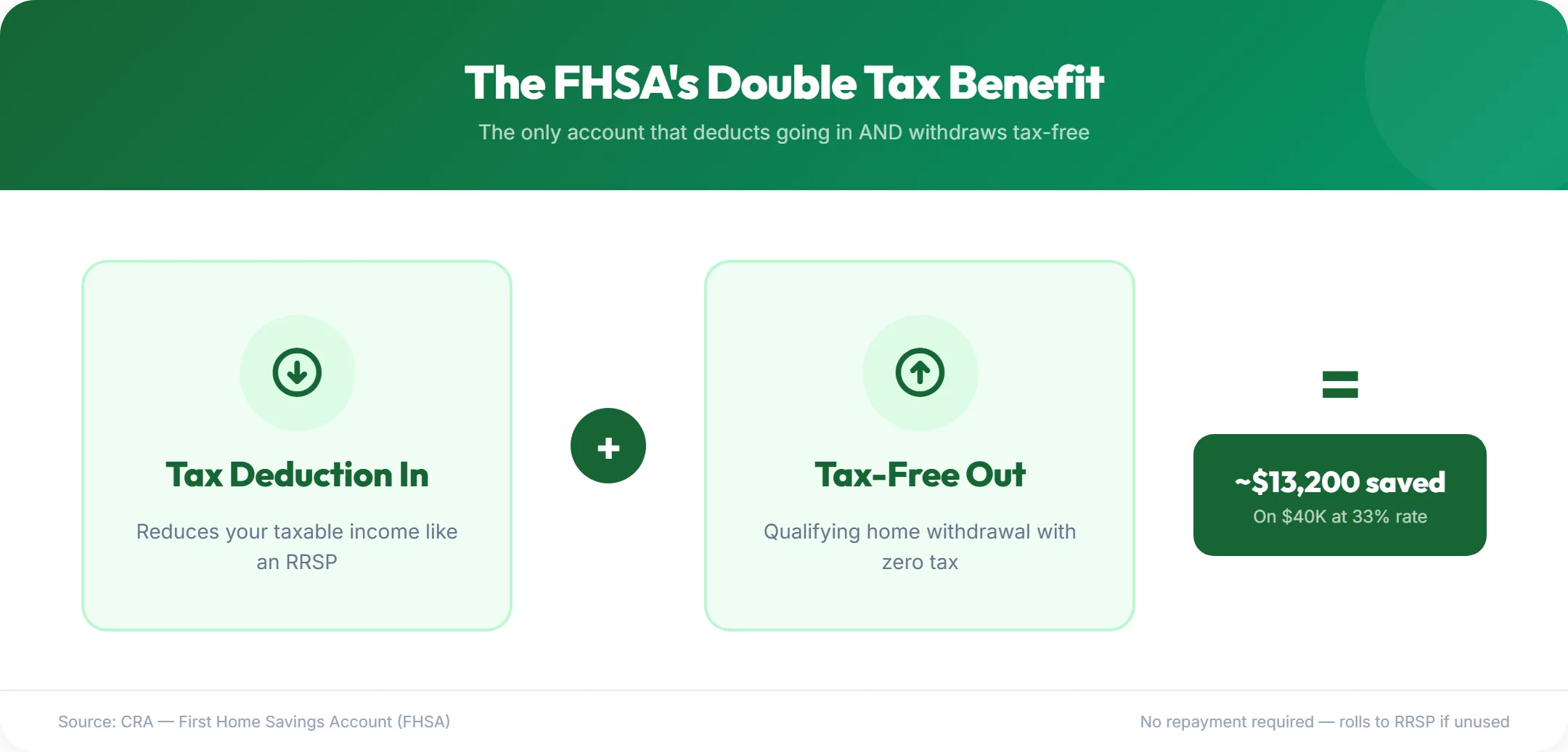

- FHSA is the only account with both a tax deduction and tax-free withdrawals

- Quebec’s higher combined rates shift the RRSP crossover point lower than other provinces

- Unused FHSA funds roll into your RRSP without consuming contribution room

What Are the Key Differences Between TFSA, RRSP, and FHSA?

The TFSA, RRSP, and FHSA all shelter investment growth from Canadian tax, but only the FHSA offers both tax-deductible contributions and tax-free withdrawals.123 The TFSA taxes nothing going in and nothing coming out. The RRSP deducts contributions now and taxes withdrawals later. The FHSA does both — tax deduction going in, tax-free withdrawal coming out — but restricts qualifying withdrawals to a first home purchase.

| Feature | TFSA | RRSP | FHSA |

|---|---|---|---|

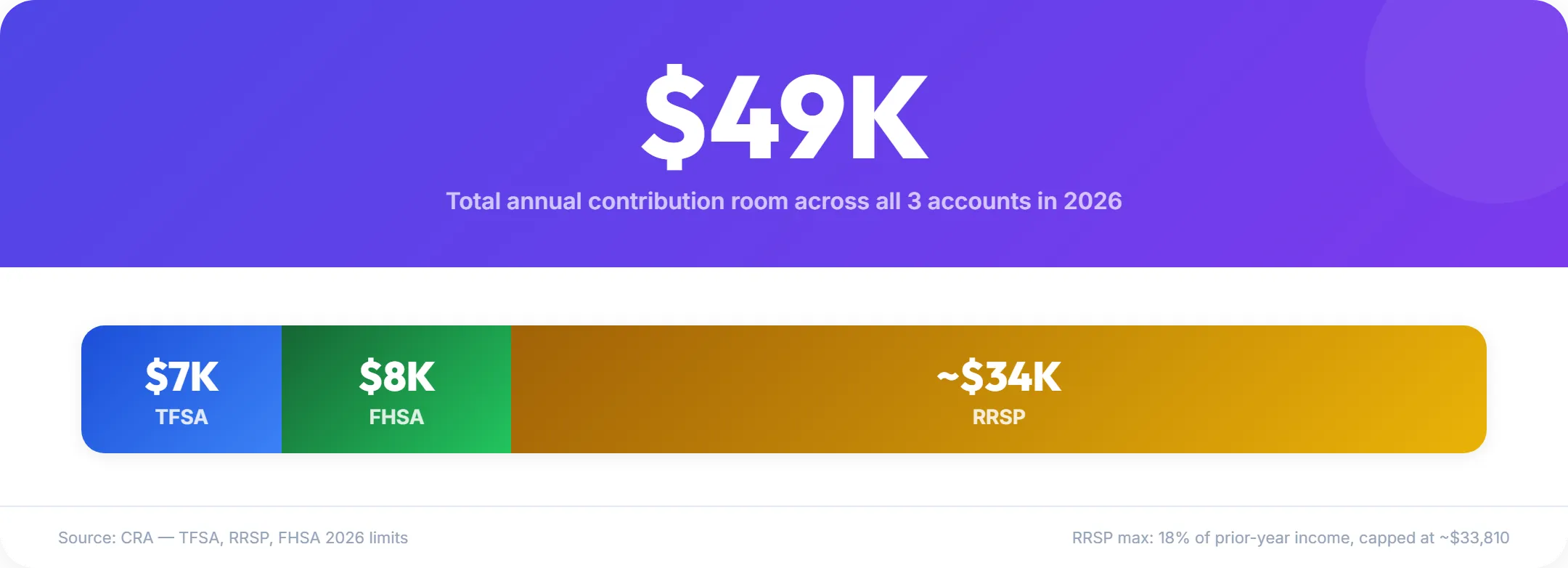

| 2026 Annual Limit | $7,000 | 18% of prior-year earned income (2026 limit: ~$33,810) | $8,000 |

| Lifetime Cap | None (cumulative room grows yearly) | None (based on earned income history) | $40,000 |

| Tax on Contribution | No deduction | Tax-deductible | Tax-deductible |

| Tax on Growth | Tax-free | Tax-deferred | Tax-free |

| Tax on Withdrawal | Tax-free, anytime | Taxed as income | Tax-free for qualifying home purchase |

| Withdrawal Restrictions | None | Taxed; HBP exception for first homes | Qualifying home, or roll to RRSP |

| Eligibility | 18+, Canadian tax resident, valid SIN | Canadian tax resident with earned income | 18–71, first-time buyer, Canadian resident |

| If You Never Use It | Withdraw anytime, no consequence | Taxed on withdrawal in retirement | Transfer to RRSP (no room consumed) |

The TFSA is the most flexible account in the Canadian tax system. Withdrawals are tax-free for any purpose — emergencies, a car, retirement — and contribution room is restored the following January after a withdrawal. The 2026 cumulative limit for someone eligible since 2009 is $109,000.1 Newcomers to Canada receive room only from their year of tax residency onward, not the full lifetime amount.

The RRSP is most powerful for high earners planning to withdraw in retirement at a lower tax rate. The deduction reduces your taxable income now, when your rate is highest, and the tax deferral lets your money compound on pre-tax dollars for decades. The catch: every dollar withdrawn is taxed as ordinary income. The Home Buyers’ Plan (HBP) lets first-time buyers borrow up to $60,000 from their RRSP tax-free, but that amount must be repaid over 15 years or the missed payments are added to your taxable income.

The FHSA combines the best features of both accounts. Contributions reduce your taxable income (like an RRSP), qualifying withdrawals for a first home are completely tax-free (like a TFSA), and there is no repayment obligation.3 If you never buy, the entire balance — contributions and all investment growth — transfers directly to your RRSP without consuming any contribution room. The FHSA exit strategies make it a risk-free way to create extra tax-sheltered space, whether or not you end up buying.

Which Account Should You Open First?

The priority order for opening a TFSA, RRSP, or FHSA depends on whether you plan to buy a home within 15 years and whether your income is above roughly $55,000. These five scenarios cover the most common situations for Canadians deciding between the three accounts in 2026.

Scenario A: You plan to buy a home within the next 5 years

Open the FHSA first. The First Home Savings Account is the single most efficient vehicle for a first home down payment in Canada. The tax deduction on contributions and the completely tax-free qualifying withdrawal create a double benefit no other account matches. At a 33% combined marginal rate, maxing the $40,000 FHSA lifetime limit generates approximately $13,200 in cumulative tax savings — money that is permanently yours with no repayment requirement.3

If you have not opened an FHSA yet, do it now, even with a $0 deposit. Room only accumulates from the year you open the account, and a late-December opening locks in $8,000 — plus another $8,000 on January 1, giving you $16,000 of available room immediately.3

After the FHSA is funded, direct remaining savings into the TFSA for flexible backup capital you can access without tax consequences.

Scenario B: You might buy someday but are not certain

Still open the FHSA first. The FHSA is free optionality with no downside. If you buy, you get the double tax benefit. If you do not buy, you transfer the full balance — contributions plus all growth — into your RRSP without using any RRSP room.3 There is no scenario where opening the FHSA costs you money, and every year you delay costs you $8,000 of permanently lost room.

The worst outcome: you contribute $40,000 over five years, it grows to $60,000, and the entire amount becomes bonus RRSP space that would not otherwise exist. That is the floor, not the ceiling.

One caveat: once the FHSA rolls into your RRSP, that money is locked in a retirement vehicle. If your income is under $55,000 and you think you might need the cash before age 65 for something other than a house, prioritize the TFSA instead to maintain full liquidity.

Scenario C: Not buying a home, income under $55,000

Open the TFSA first. In our analysis, at income below roughly $50,000 to $55,000, the RRSP deduction saves relatively little because your combined marginal rate is low. A $7,000 RRSP contribution at a 20% combined rate saves you $1,400 in tax. That same $7,000 in a TFSA produces no immediate deduction, but every dollar of growth and every future withdrawal is permanently tax-free.

The TFSA also offers flexibility the RRSP cannot match. You can withdraw for any reason without penalty and regain the contribution room the following January. An RRSP withdrawal is fully taxed and you permanently lose that room. For someone in their 20s or early 30s with uncertain future needs, the TFSA’s flexibility is worth more than a modest tax deduction.

If you still have room after maxing the TFSA, then start contributing to the RRSP — especially if you expect your income to grow. We often recommend this strategy: contribute the cash now to begin compounding, but defer the RRSP deduction to a future year when your marginal rate is higher. An $8,000 deduction at 45% returns $3,600 versus $1,600 at 20% — a $2,000 difference from timing alone.

Scenario D: Not buying a home, income above $55,000

Open the RRSP first. Above roughly $55,000 in most provinces, the combined federal-provincial marginal rate exceeds 30%. At that level, a $7,000 RRSP contribution saves you $2,100 or more in tax — significantly more than the opportunity cost of foregoing TFSA flexibility. In Quebec, where combined rates climb faster due to higher provincial brackets, the RRSP advantage kicks in at even lower incomes.

The RRSP works best when your contribution tax rate is higher than your eventual withdrawal tax rate. If you earn $80,000 now and expect to draw $45,000 annually in retirement, the spread between those marginal rates is permanent profit. Every dollar deducted at 30% and withdrawn later at 20% generates a lasting 10-cent gain per dollar contributed, on top of the tax-deferred compounding.

After maxing your RRSP room for the year (check your CRA Notice of Assessment for your exact limit), direct remaining savings into the TFSA for flexible, tax-free growth. For a comparison of which platforms offer the best RRSP experience, see our RRSP broker comparison.

Scenario E: You have already maxed the FHSA

Prioritize TFSA or RRSP based on income, using the same logic as Scenarios C and D. If your FHSA is at its $40,000 lifetime cap or you have contributed the maximum $8,000 for the year, the remaining decision is purely between the TFSA and RRSP — and income is the tiebreaker.

One exception: if you are within a few years of buying your first home and your RRSP has room, consider making additional RRSP contributions earmarked for the Home Buyers’ Plan. Combining a maxed FHSA ($40,000 tax-free) with a full HBP withdrawal ($60,000 from your RRSP) gives a solo buyer $100,000 of tax-sheltered capital for a down payment — or $200,000 as a couple.

One timing note: on Wealthsimple, RRSP Home Buyers’ Plan withdrawals typically process in 2 to 5 business days, though other brokerages can take longer. Initiate the withdrawal as soon as you have an accepted offer. Also note the CRA’s 90-day rule: any funds deposited into your RRSP within 90 days of your HBP withdrawal are not eligible for tax-free extraction.

How Does the Math Work at Different Tax Brackets?

Based on our math, the crossover point where an RRSP pulls ahead of a TFSA falls around $55,000 of annual income in most provinces, though Quebec’s higher combined rates shift it lower.4 An $8,000 contribution to an RRSP or FHSA saves a different dollar amount depending on whether you live in Ontario, Quebec, or elsewhere — and Quebec’s higher provincial rates make the RRSP more attractive at lower incomes than most comparisons acknowledge.

Aaron Hector, Senior Wealth Advisor and Founding Partner at TIER Wealth in Calgary, told Investment Executive:

“The piece a lot of people miss in that [TFSA vs. RRSP] conversation is the family plan. You might be in a middle tax bracket, but when you add on the Canada Child Benefit … you’re probably pushing up into a top marginal tax bracket or approaching it.”5

| Annual Income | Approx. Combined Rate (Ontario) | Approx. Combined Rate (Quebec) | Tax Saved on $8,000 (Ontario) | Tax Saved on $8,000 (Quebec) |

|---|---|---|---|---|

| $45,000 | ~20% | ~27% | ~$1,600 | ~$2,160 |

| $70,000 | ~30% | ~36% | ~$2,400 | ~$2,880 |

| $110,000 | ~32% | ~41% | ~$2,560 | ~$3,280 |

| $150,000 | ~37% | ~50% | ~$2,960 | ~$4,000 |

Combined rates are approximate and include the Quebec abatement. Exact rates depend on available credits and deductions. Source: CRA and Revenu Quebec published brackets.4

What the table reveals: Quebec residents get significantly more value from RRSP and FHSA contributions at every income level. At $70,000, a Quebec resident saves approximately $2,880 on an $8,000 deductible contribution compared to $2,400 for an Ontario resident — a $480 difference on the same deposit. This is why the “RRSP above $55K” rule of thumb applies more aggressively in Quebec: combined marginal rates climb past 30% at lower income levels than in most other provinces.

The crossover in practice: A 28-year-old in Ontario earning $48,000 saves about $1,600 on an $8,000 RRSP contribution. That is real money, but the TFSA gives you tax-free growth on the same $8,000 without locking it away until retirement. Since your withdrawal rate in retirement may be similar to your current rate (many retirees draw $40,000 to $50,000 annually), the RRSP deferral advantage is minimal at this income. The TFSA wins on flexibility.

If that same person earns $75,000, the RRSP contribution now saves roughly $2,400. The tax deferral becomes meaningful — you are deducting at ~30% now and will likely withdraw at ~20% in retirement. The RRSP wins on pure math.

The FHSA resets the entire calculation. If that person might buy a home, the FHSA at 30% saves $2,400 going in and charges $0 coming out — no repayment, no withdrawal tax, no room consumed. For anyone even considering homeownership, the FHSA dominates both the RRSP and TFSA at every income level.

Can You Use All Three Accounts at Once?

Yes, you can contribute to a TFSA, RRSP, and FHSA simultaneously — the combined annual maximum is approximately $48,810 in 2026 (TFSA $7,000 + RRSP max ~$33,810 + FHSA $8,000).123 We rarely see Canadians who can fill all three at once. The practical question we hear most often is how to split a realistic monthly savings budget.

Dave Chilton, author of The Wealthy Barber and former Dragon’s Den panelist, told CBC News:

“There’s nobody out there maximizing their RRSP and their TFSA and their FHSA. Come on, that only happens in books. In real life, that’s not happening. So which way do you go? And whatever path you take, how do you keep your fees down?”6

A practical allocation for $500/month

For someone earning $65,000, not yet a homeowner, with access to all three accounts, the priority order is:

- Employer RRSP match first — if your employer offers matching contributions, contribute at least enough to capture the full match. This is an immediate 100% return and takes priority over everything else

- FHSA second — the double tax benefit and RRSP rollover safety net make every dollar here more valuable than either alternative. At $500/month after employer match, allocate $350/month ($4,200/year toward the $8,000 annual limit)

- TFSA with remaining budget — direct the remaining $150/month ($1,800/year) into the TFSA for flexible, tax-free growth

As income grows, increase your FHSA allocation to the $8,000 annual cap first, then expand the RRSP — particularly once your marginal rate climbs above 30%. Once the FHSA is maxed at $40,000 lifetime, redirect that allocation to the RRSP (if income is above $55,000) or the TFSA (if below).

One nuance most comparison guides miss: you do not have to claim the RRSP or FHSA deduction in the same year you contribute. If you are in a low tax bracket now but expect a raise soon, contribute the cash immediately to start tax-free compounding, then carry the deduction forward to a higher-income year. You report the contribution on your return but choose to claim $0 as your deduction for that year. The dollar value of the deduction scales with your marginal rate, so deferring to a higher-income year can double the refund.

How Does Wealthsimple Handle All Three Accounts?

Wealthsimple offers the TFSA, RRSP, and FHSA in a single app with $0 trading commissions, $0 account fees, and $0 transfer-out fees.7 If you are moving an existing registered account from a Big Five bank, Wealthsimple will reimburse the transfer-out fee your old bank charges (typically $150+), provided you transfer at least $25,000. All three accounts support both self-directed investing (you choose stocks, ETFs, and crypto ETFs) and managed portfolios (Wealthsimple invests for you at a 0.4% to 0.5% management fee).

We tested the process: opening each account takes under 5 minutes, with no minimum deposit. You can fund all three from the same linked bank account, set up automatic contributions on different schedules, and switch between accounts in one tap. If you hold uninvested cash in a Wealthsimple Cash account, transfers into your TFSA, RRSP, or FHSA are instant — even on weekends. For a breakdown of the Core (free), Premium, and Generation tiers, see our tier comparison. For a head-to-head comparison with Canada’s other major discount brokerage, see our Wealthsimple vs Questrade analysis.

In our experience, internal transfers between your Wealthsimple TFSA, RRSP, and FHSA process digitally in a few taps, requiring no paperwork and charging zero fees. This matters most for the FHSA-to-RRSP rollover — if you decide not to buy a home, you submit an RC721 form via DocuSign in the Wealthsimple app and their back office handles the rest within a few business days.

In our testing of transfers from Big Five banks, we experienced a brief gap where the balance showed zero at the old institution before appearing on Wealthsimple — typically a few business days. This is normal and does not mean your money is lost.

Wealthsimple is registered with the Ontario Securities Commission and a member of CIPF, which protects each account up to $1 million if the firm becomes insolvent — the same coverage as any Big Five bank brokerage.

New accounts opened through a Wealthsimple referral code qualify for a cash bonus on the first deposit. Current Wealthsimple promotions include a $25 bonus on a $100 minimum deposit, deposited into your account within 24 hours. Our strategy when opening multiple accounts is to apply the referral code on the first account, then fund subsequent accounts through internal transfers.

Sources

Footnotes

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.