Wealthsimple FHSA 2026: Limits, Eligibility & The $0 Opening Trick

Start the carry-forward clock with a $0 deposit, defer deductions to a higher bracket, and use the RRSP exit if you never buy. The mechanics most guides skip.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

TL;DR: The FHSA gives you a tax deduction on the way in and tax-free withdrawals on the way out — the only Canadian account that does both. Wealthsimple offers $0 commissions and $0 transfer-out fees. The $40,000 lifetime limit generates up to $13,200+ in tax savings depending on your bracket.

- $8,000 annual limit with carry-forward on unused room (after opening)

- Open with $0 now to start the contribution room clock — every year without an account is $8,000 lost

- If you never buy, the full balance rolls into your RRSP without using contribution room

This guide covers the 2026 contribution limits, carry-forward math, eligibility rules, the $0 opening strategy that locks in extra room, Wealthsimple’s fee structure, and the exit strategies that make the FHSA a win even if you never buy a home.

What is the FHSA and why does it matter?

The First Home Savings Account (FHSA) launched on April 1, 2023 as a registered account designed specifically for Canadians saving for their first home. The FHSA combines the two strongest features of existing registered accounts: contributions reduce your taxable income the same way an RRSP does, and qualifying withdrawals come out entirely tax-free the same way a TFSA works.

As David Chilton, bestselling author of The Wealthy Barber, put it, the FHSA is “the greatest deal in the history of Canadian savings.”1

For a Canadian in the 33% combined marginal tax bracket, an $8,000 FHSA contribution generates approximately $2,640 in tax savings — money that can be reinvested or applied directly to the down payment fund. Those savings compound year after year across the $40,000 lifetime contribution limit, creating a total tax reduction worth $13,200 or more depending on your bracket.

No other account does this. An RRSP gives you the deduction but taxes the withdrawal. A TFSA gives you tax-free growth but no deduction on the way in. The FHSA gives you both, plus a built-in safety net (the RRSP rollover) if your plans change.

In Quebec, the FHSA is known as the CELIAPP (Compte d’épargne libre d’impôt pour l’achat d’une première propriété). The federal rules are identical, but Quebec residents receive an additional RL-32 tax slip alongside the federal T4FHSA. Wealthsimple automatically generates both slips — no manual calculation required.

Who qualifies for the FHSA?

The FHSA is available to any Canadian resident who is between 18 and 71 years old and qualifies as a first-time home buyer under the CRA’s definition.2 You are considered a first-time home buyer if you have not lived in a qualifying home that you or your spouse/common-law partner owned as a principal residence in the current calendar year or the four preceding years.

Three situations that trip people up:

- Your spouse owns a home you’ve never lived in. You are still eligible. The test is whether the home was your principal residence, not whether your partner holds title. A spouse’s rental property or pre-relationship home you never occupied does not disqualify you.

- You inherited a share of a family cottage. Owning a fractional share of a property does not disqualify you if you never lived in it as your principal residence. A vacation cottage used seasonally while you rent an apartment downtown leaves your eligibility intact.

- You’re on a work permit (SIN starting with 9). Tax residency, not immigration status, determines eligibility. If the CRA considers you a Canadian resident for tax purposes — which most full-time workers with a Canadian home and SIN are — you can open and fund an FHSA.

For more thorough scenarios — including divorce settlements, inherited cottages, and work-permit residency — see our FHSA eligibility edge cases guide.

What are the FHSA contribution limits for 2026?

The FHSA contribution limit for 2026 is $8,000 per year, with a $40,000 lifetime maximum. Unused contribution room carries forward to the next year, capped at an additional $8,000 of carry-forward. That means the most you can ever contribute in a single year is $16,000 — one year’s fresh room plus one year of carried-forward room.

Unlike the TFSA, FHSA room does not accumulate automatically. Your contribution room only starts building from the year you open the account. If you have never opened an FHSA, you have $0 of room right now regardless of how long the program has existed.

This makes the timing of account opening the single most important decision with the FHSA.

The $0 opening trick

The optimal move for anyone who might buy a home in the next 15 years is to open an FHSA immediately with a $0 deposit.2 The moment the account is registered with a financial institution, the CRA grants you $8,000 of participation room for that calendar year. If you don’t contribute, that $8,000 carries forward.

Here is what this looks like in practice:

| Year | Action | New Room | Carry-Forward | Total Available Room |

|---|---|---|---|---|

| 2025 | Open account, deposit $0 | $8,000 | $0 | $8,000 |

| 2026 | Receive bonus, contribute $16,000 | $8,000 | $8,000 | $16,000 |

| 2027 | Regular contributions resume | $8,000 | $0 | $8,000 |

If the same person waited until January 2026 to open, their maximum 2026 contribution would be capped at $8,000. The $8,000 of 2025 room would be permanently forfeited — a loss worth up to $2,640 in future tax savings (at a 33% marginal rate).

How does the FHSA tax deduction work?

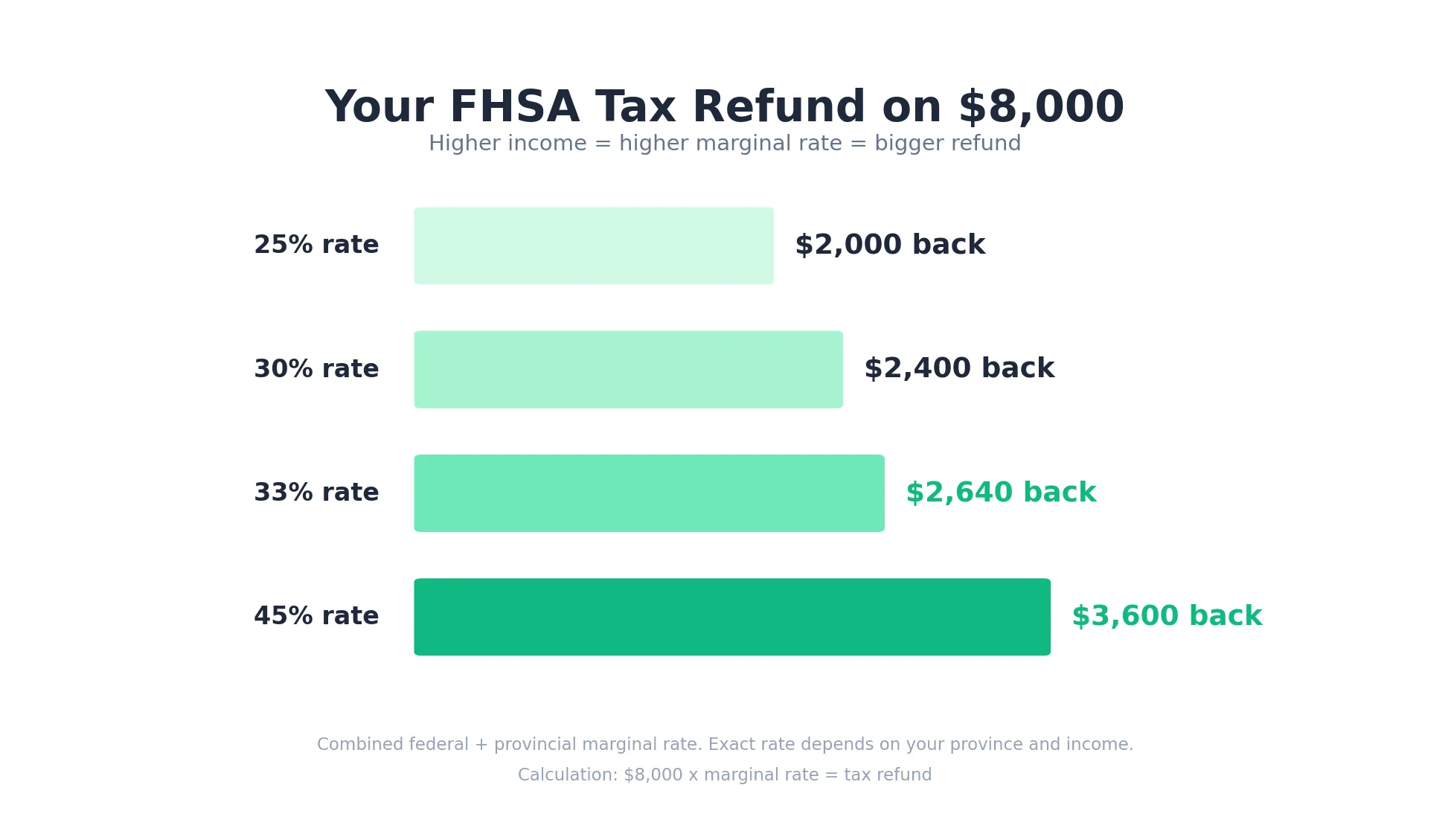

The Wealthsimple FHSA tax deduction works identically to a Wealthsimple RRSP deduction: every dollar you contribute reduces your taxable income for the year, and the tax savings scale with your marginal tax rate. An $8,000 contribution saves roughly $2,000 at a 25% rate, $2,640 at 33%, or $3,600 at 45%.

As Jamie Golombek, Managing Director of Tax and Estate Planning at CIBC Private Wealth, summarized in a Yahoo Finance Canada interview, “The FHSA is the best of everything” — combining the RRSP’s tax deduction with the TFSA’s tax-free withdrawals.3

At a 33% marginal rate, one $8,000 FHSA contribution puts $2,640 back in your pocket at tax time.

The deduction deferral strategy

Here is where the FHSA gets tactically interesting. You are not required to claim the deduction in the same year you contribute. This matters enormously for anyone currently in a low tax bracket — medical residents, articling law students, junior developers, recent graduates — who expect significantly higher income within a few years.

The strategy: contribute now to get the money into the tax-free compounding environment immediately. Report the contribution on Schedule 15 of your tax return. But on Line 20805, claim $0 as your FHSA deduction. Carry the deduction forward to a future year when your marginal rate has climbed from 20% to 40%+.

The result is that you capture full time-in-market returns and maximize the dollar value of the tax refund. An $8,000 deduction claimed at a 20% rate returns $1,600. That same deduction claimed three years later at a 45% rate returns $3,600 — an extra $2,000 from pure timing.

Tax season note: the T4FHSA slip may not appear immediately in the CRA’s Auto-fill my return service. You can usually find it sooner in the Wealthsimple app under Documents → Tax Documents before it syncs with the CRA. Also worth noting: the FHSA contribution room displayed on your CRA My Account portal can lag by several months. Track your own contributions through the Wealthsimple app’s net deposits figure rather than relying on the CRA dashboard during the year.

How do you open an FHSA on Wealthsimple?

Opening a Wealthsimple FHSA takes approximately 5 minutes through the mobile app or web dashboard. Wealthsimple offers two account architectures:

Self-Directed FHSA — $0 commissions on all Canadian and US-listed stocks and ETFs. You choose and manage your own investments. Limited to one self-directed FHSA per person on the platform.

Managed FHSA — Wealthsimple’s robo-advisor builds and rebalances a diversified portfolio based on your risk profile and timeline. Management fee of 0.5% (or 0.4% with Wealthsimple Premium). You can open multiple managed FHSAs with different risk levels.

Steps to open

- Log into Wealthsimple (or create an account using a referral code 9C6DMQ for a $25 cash bonus on your first deposit)

- Select “Add Account” and choose FHSA from the registered account options

- Choose self-directed or managed based on your investment comfort level

- Confirm your eligibility — the app walks you through the first-time home buyer declaration

- Fund the account — deposit via bank transfer, or transfer from another institution (Wealthsimple reimburses transfer-in fees on transfers of $25,000+)

Check our Wealthsimple promotions page for additional bonuses you can stack with the referral code.

We verified that Wealthsimple registers the account with the CRA almost instantly upon opening. This immediately locks in your $8,000 of room for the current year, even if you leave the balance at $0.

One detail to plan around: new deposits to the FHSA typically trigger a 5-business-day settlement hold before the funds are available to invest. If you are contributing close to a year-end deadline, deposit at least a week early to ensure the contribution registers in the correct tax year.

Important for self-directed users: uninvested cash sitting in your Wealthsimple FHSA earns 0% interest. Unlike a bank FHSA savings account, you need to actually purchase investments — even a money market fund or savings ETF — to generate any return on your balance.

Can you use the FHSA and HBP together?

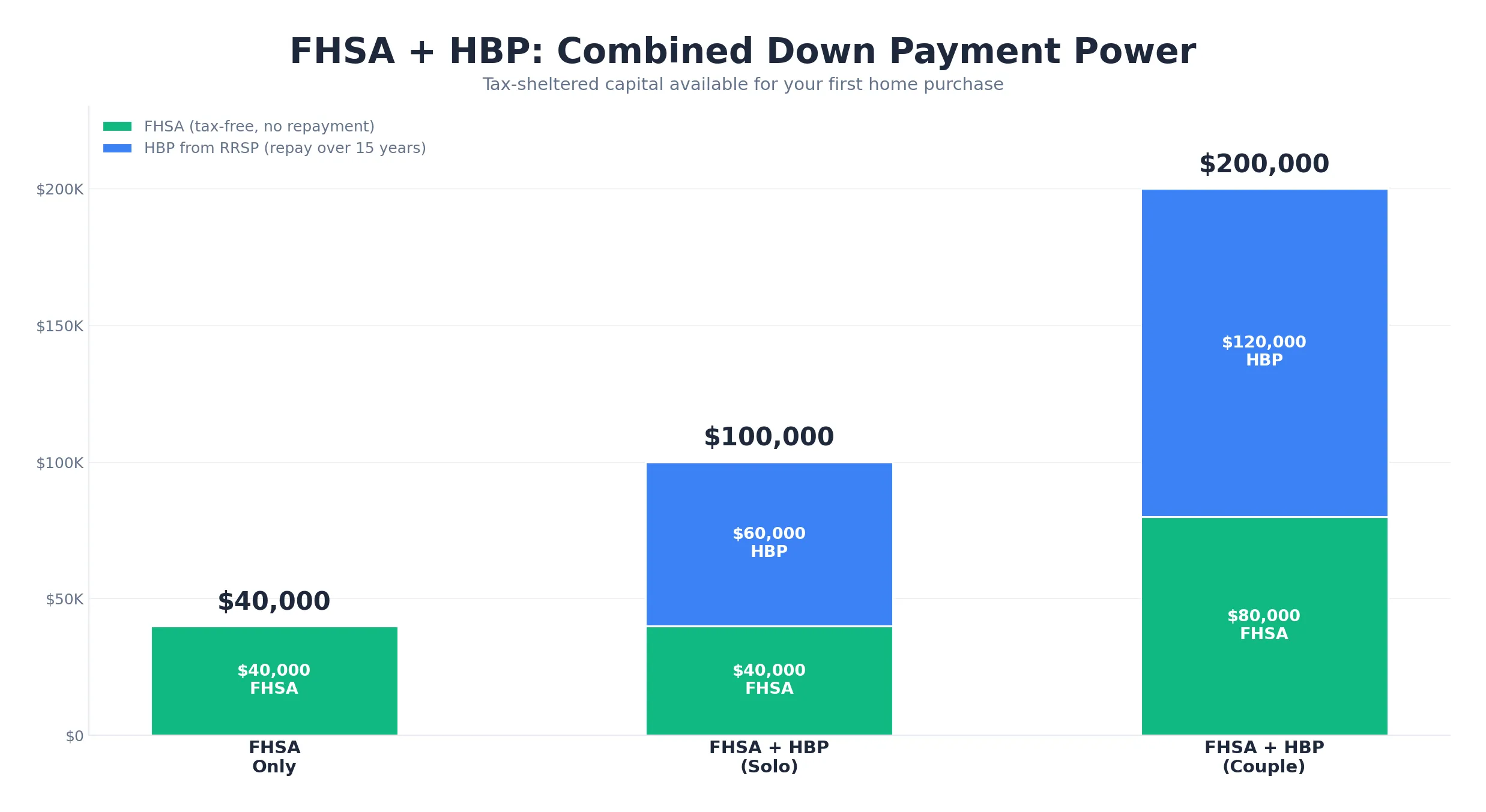

Yes — the CRA explicitly allows you to use both the FHSA ($40,000 tax-free) and the Home Buyers’ Plan ($60,000 RRSP loan) for the same qualifying home purchase.4

The combined math for a solo buyer:

| Vehicle | Maximum | Tax on Contribution | Tax on Withdrawal | Repayment Required |

|---|---|---|---|---|

| FHSA | $40,000 | Fully deductible | Tax-free | None |

| HBP (from RRSP) | $60,000 | Fully deductible | Tax-free (loan) | 15 years |

| Combined | $100,000 | Deductible | Tax-free | HBP portion only |

A couple optimizing together reaches $200,000 in tax-sheltered down payment capital. In Toronto, Vancouver, or Montreal, that is the difference between a 5% down payment requiring CMHC insurance and a 20% down payment without it.

The critical distinction: the FHSA withdrawal is permanent and free. The HBP withdrawal is a loan from your own RRSP that must be repaid over 15 years, or the unpaid annual minimum gets added to your taxable income.

We break down the full strategy, including carry-forward optimization and the repayment math, in our FHSA + HBP down payment strategy guide.

What are the FHSA withdrawal rules?

Wealthsimple FHSA withdrawals fall into two categories: qualifying withdrawals for a first home purchase (completely tax-free) and non-qualifying withdrawals (fully taxable as income).

Qualifying withdrawal (tax-free)

A qualifying withdrawal for a first home purchase is completely tax-free.5 To qualify, you must:

- Be a first-time home buyer at the time of withdrawal (same four-year test as opening)

- Have a written agreement to buy or build a qualifying home in Canada

- Intend to occupy the home as your principal residence within one year of buying or building it

- Have held an FHSA for at least one year (your account must have been open for a minimum of one calendar year)

There is no repayment obligation. The money leaves the FHSA and goes to you permanently, tax-free. Unlike the HBP, you do not owe anything back.

No repayment, no strings. The FHSA qualifying withdrawal is yours to keep — contributions and growth included.

A practical timing note: real estate lawyers typically require closing funds (bank draft or wire) several days before the closing date. Since Wealthsimple FHSA withdrawals can take 2–5 business days to reach your chequing account, initiate the withdrawal at least 10 business days before your closing date.

Non-qualifying withdrawal (taxable)

Any withdrawal that does not meet the qualifying criteria is fully taxable as income in the year of withdrawal. Wealthsimple issues a T4FHSA slip, and the full amount is added to your taxable income. This includes withdrawing to fund a non-Canadian purchase, withdrawing without a written purchase agreement, or withdrawing when you do not meet the first-time buyer test.

What happens if you never buy a home?

The Wealthsimple FHSA is not wasted even if you never buy a home — you can transfer the entire balance, including all investment growth, directly into your RRSP without consuming contribution room. The account must close by December 31 of its 15th anniversary year (or when you turn 71, whichever comes first), but you are not forced into a taxable liquidation.

Your options:

- Transfer to your RRSP — The entire FHSA balance, including all investment growth, can move directly into your RRSP. This transfer does not consume your RRSP contribution room. If you have $0 of RRSP room and $80,000 in your FHSA (from $40,000 of contributions that doubled), you can roll the full $80,000 into your RRSP with no penalty and no over-contribution.

- Transfer early — You do not have to wait 15 years. If you decide at year 5 that homeownership is not for you, transfer the balance immediately.

- Transfer to an RRIF — For older account holders approaching retirement, a direct transfer to a RRIF is also permitted.

We tested the RRSP rollover process and found it’s handled entirely through the app’s internal transfer interface — no paper T2033 forms, no medallion signatures, no mailing documents. Because both accounts are held within the same trustee environment, the transfer typically completes within days.

For the full breakdown of exit strategies including the non-resident scenario, see our FHSA exit strategy guide.

What are the Wealthsimple FHSA fees?

Wealthsimple charges $0 for commissions, account opening, maintenance, and transfer-out fees on the self-directed FHSA — the same zero-commission model that applies across all their registered accounts.

| Fee Type | Wealthsimple FHSA |

|---|---|

| Account opening | $0 |

| Commissions (stocks & ETFs) | $0 |

| Account maintenance | $0 |

| Inactivity fee | $0 |

| Transfer out to another institution | $0 |

| Managed portfolio fee | 0.4% – 0.5% |

| Currency conversion (USD trades) | 1.5% (or $0 with Premium) |

The $0 transfer-out fee is a significant competitive advantage. Users testing the FHSA on Wealthsimple face zero financial risk — if they decide to move to another institution later, the exit is completely free. Most Big Five banks charge $135 to $150 to transfer a registered account out.

For incoming transfers of $25,000 or more, Wealthsimple reimburses the transfer-out fee charged by your previous institution.6

Managed vs. self-directed cost comparison

The managed FHSA’s 0.4-0.5% annual fee covers automated rebalancing, tax-loss harvesting, and portfolio construction. On a $40,000 balance, that is $160-$200 per year. For comparison, purchasing a single all-in-one ETF like XEQT or VEQT in the self-directed FHSA costs $0 in commissions and carries only the underlying ETF’s MER (approximately 0.20%).

For most investors comfortable choosing one or two broad ETFs, the self-directed option saves roughly $120-$160 per year on a fully funded FHSA. For context on how Wealthsimple’s managed portfolio fees compare across account types, see our RRSP match comparison.

One hidden cost in the self-directed FHSA: unlike an RRSP, the FHSA is not recognized under the Canada-US tax treaty. If you hold US-listed stocks that pay dividends, the IRS withholds 15% on those dividends automatically — and you cannot recover it. For a pure-Canadian ETF portfolio (XEQT, VEQT), this is a non-issue.

The bottom line

The Wealthsimple FHSA is the strongest tax-sheltered account available to Canadian first-time buyers in 2026. The $8,000 annual deduction, tax-free qualifying withdrawals, and RRSP rollover safety net create a no-lose structure: you either buy a home tax-free or you get bonus RRSP room above your normal limit.

The single most important action is opening the account now — even with $0 — to start the contribution room clock. Every year without an open account is $8,000 of room permanently lost.

Combined with the Home Buyers’ Plan, a solo buyer can deploy $100,000 and a couple $200,000 in fully tax-sheltered capital toward a first home. For the full picture of how the FHSA fits alongside your TFSA and RRSP, see our TFSA vs RRSP vs FHSA comparison.

Frequently asked questions

What is the FHSA contribution limit for 2026?

The FHSA contribution limit for 2026 is $8,000 per year, with a lifetime maximum of $40,000. Unused contribution room carries forward to the following year, up to a maximum carry-forward of $8,000. If you opened your account in 2023 and never contributed, your 2026 room would be $16,000 ($8,000 new + $8,000 carry-forward).

Can I open an FHSA if my spouse owns a home?

Yes — as long as you personally have not lived in a qualifying home that you or your spouse owned as your principal residence in the current year or the preceding four calendar years. If your spouse owns a rental property you have never lived in, you are fully eligible. The key test is principal residency, not spousal ownership alone.

What happens to my FHSA if I never buy a home?

Your funds are not lost. You can transfer the entire balance — including all investment growth — directly into your RRSP at any time before the 15-year expiry. This transfer does not consume your RRSP contribution room. It effectively gives you bonus RRSP space above your normal limit.

Can I use the FHSA and HBP together for the same home?

Yes. The CRA explicitly permits using both the FHSA ($40,000 tax-free) and the Home Buyers’ Plan ($60,000 tax-free RRSP loan) for the same qualifying purchase. A solo buyer can deploy up to $100,000 in tax-sheltered capital. A couple can reach $200,000.

Does Wealthsimple charge fees on the FHSA?

Wealthsimple charges $0 for commissions, account opening, maintenance, and outgoing transfers on the self-directed FHSA. The managed (robo-advisor) FHSA carries a 0.4% to 0.5% management fee. There are no inactivity fees and no transfer-out fees.

Can I claim the FHSA tax deduction in a different year than I contribute?

Yes. Like an RRSP, you can contribute to your FHSA now to start tax-free compounding, then carry the deduction forward to a future year when your income and marginal tax rate are higher. Report the contribution on Schedule 15 but claim $0 on Line 20805.

Sources

Footnotes

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.