FHSA Exit Strategy: What Happens If You Never Buy a Home

Opened an FHSA but life changed? The RRSP rollover turns your contributions plus growth into bonus retirement room — and non-residents can keep contributing until the 15-year window closes.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

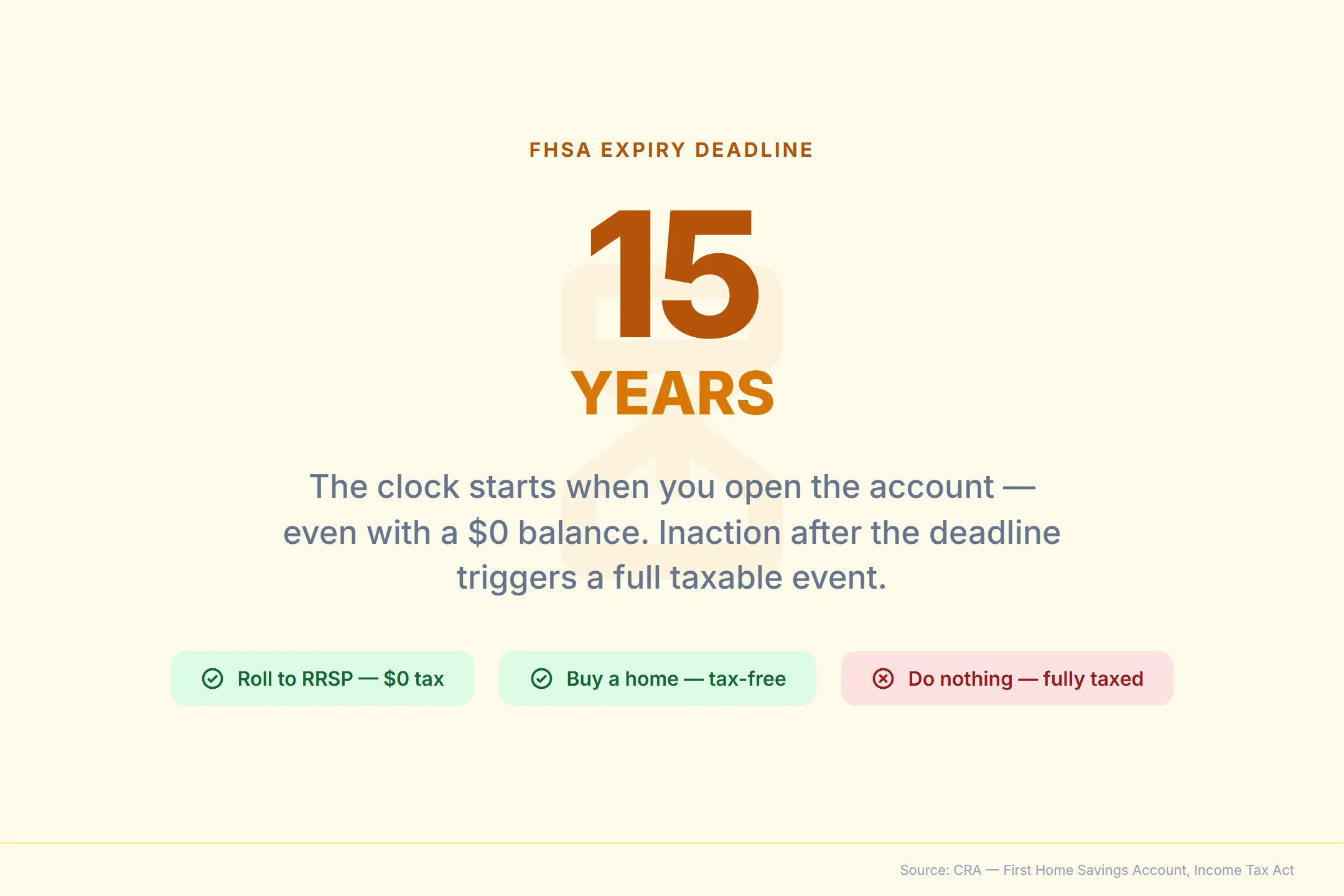

The 15-year clock starts the day you open the account, not the day you max it out.

The Bottom Line: The FHSA is never wasted. Transfer everything — contributions plus growth — to your RRSP without using contribution room. A $40,000 FHSA that grows to $80,000 becomes $80,000 of bonus RRSP space. You have 15 years from opening to act.

- FHSA-to-RRSP rollover is tax-free and independent of your RRSP room

- Wealthsimple handles transfers digitally via DocuSign — no branch visits

- Non-residents can keep their FHSA open and continue contributing until the 15-year expiry

The 15-year wall: when does the FHSA expire?

According to the CRA, the FHSA must be closed by December 31 of the year marking its 15th anniversary, or by December 31 of the year the account holder turns 71 — whichever comes first.1 An FHSA opened in 2023 must be fully resolved by December 31, 2038. An FHSA opened in 2026 has until December 31, 2041. Opening any FHSA — even with a $0 balance — starts the 15-year clock immediately. An account opened to explore the interface and closed the next day has already begun the countdown.

The most common fear around this deadline is that Wealthsimple (or any institution) will force-liquidate the portfolio on January 1 of the following year, dumping the entire balance into your taxable income at your highest marginal rate.

This does not happen automatically. The CRA does not instruct financial institutions to auto-liquidate FHSAs. What happens is that after the deadline, the account “ceases to be an FHSA” in the eyes of the tax code.1 If the funds are still sitting in the account at that point, the full fair market value is deemed taxable income on the holder’s final FHSA return for that year.

The key distinction: the taxable event is triggered by inaction, not by automatic institutional enforcement. As long as the account holder takes one of the three exit actions before the deadline, the tax hit is entirely avoidable.

The three exit paths

| Exit Path | Tax Treatment | Repayment | Best For |

|---|---|---|---|

| Qualifying withdrawal (buy a home) | Tax-free | None | First-time buyers |

| Transfer to RRSP or RRIF | Tax-free | None | Non-buyers, career renters, plan changes |

| Non-qualifying withdrawal (cash out) | Fully taxable as income | None | Last resort only |

We recommend the RRSP rollover in virtually every scenario for someone who does not buy a home.

Does the FHSA to RRSP rollover use contribution room?

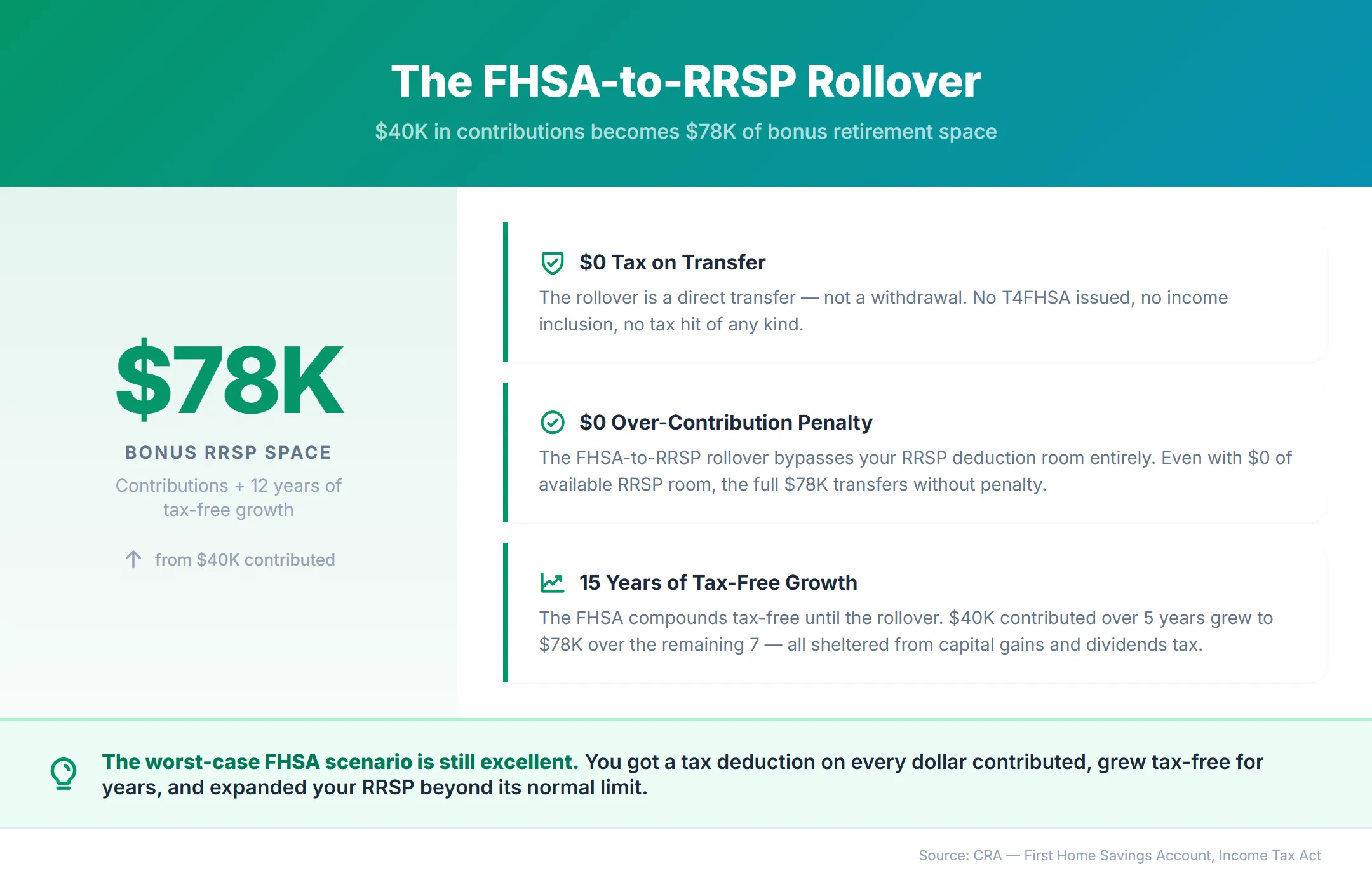

The FHSA-to-RRSP transfer moves the full account balance — contributions plus all investment growth — directly into an RRSP or RRIF, completely tax-free and without consuming any RRSP contribution room.1 This is the critical detail that separates the FHSA rollover from every other registered account transfer in Canada — no other registered account offers a room-independent transfer like this.

Jessica Moorhouse, Financial Educator and Host of the More Money podcast, told The Globe and Mail:

“If you’re eligible for the FHSA, open that up because you’re not stuck. If you decide [not to buy a home] later on, you can port that money over to your RRSP and it doesn’t affect your RRSP room.”2

The significance cannot be overstated. Under normal Wealthsimple RRSP rules, depositing money into an RRSP requires available deduction room — even with programs like Wealthsimple’s RRSP match, every dollar still counts against your room. Exceed your room and you face a 1% monthly over-contribution penalty. The FHSA rollover bypasses this entirely.

Be aware that some support representatives may incorrectly tell you that RRSP contribution room is required for this transfer. It is not — the RC721 form authorizes a direct rollover that is explicitly independent of your RRSP deduction room under the Income Tax Act.

What this means in practice

Consider a 40-year-old who has maximized RRSP contributions throughout their career. They have exactly $0 of available RRSP room. They also have an FHSA that they opened at 28, contributed $40,000 over five years, and let grow untouched for the next seven years. The FHSA balance is now $78,000.

They can transfer the entire $78,000 directly into their RRSP:

- $0 tax on the transfer — it is not a withdrawal

- $0 over-contribution penalty — the transfer is independent of RRSP room

- $78,000 of new RRSP assets — sheltered from tax until retirement decumulation

The FHSA effectively created $78,000 of bonus RRSP space that would not have existed otherwise. For someone already at their RRSP ceiling, this is an enormous expansion of lifetime tax-sheltered savings capacity.

Do you have to wait 15 years to transfer your FHSA to an RRSP?

You can transfer your FHSA balance to an RRSP at any time during the life of the account — there is no requirement to wait until the 15-year expiry.

If you decide at year 3 that homeownership is not part of your plan — perhaps you have committed to renting in a high-cost city, or your career requires frequent relocation — initiate the transfer immediately. There is no benefit to waiting if your decision is final, and transferring earlier means the funds begin compounding within the RRSP’s tax shelter sooner, available for the broader range of RRSP investment options.

Partial transfers are also permitted. If you have $32,000 in the FHSA and want to keep $8,000 as a housing option while moving $24,000 to your RRSP, you can do that. The flexibility is complete.

How do you transfer an FHSA to an RRSP on Wealthsimple?

Wealthsimple handles the FHSA-to-RRSP transfer digitally through a DocuSign form — no paper mailing, no medallion signatures, and no branch visits. Because both the FHSA and RRSP are held within the same trustee environment (Canadian Western Trust via Wealthsimple Investments Inc.), the transfer stays internal.

Steps to transfer FHSA to RRSP on Wealthsimple

- Log into Wealthsimple and navigate to your FHSA account

- Tap Transfer and select your Wealthsimple RRSP as the destination (if you do not have one, open it first — use a referral code 9C6DMQ for a $25 bonus)

- Complete the RC721 form — Wealthsimple sends this via DocuSign for electronic signature

- Wealthsimple processes the transfer — their team handles the rest after you submit the signed form, coding it as a direct rollover (not a taxable withdrawal) for CRA reporting

One detail to watch for: Wealthsimple cannot transfer fractional shares between account types. If you hold partial shares (common with recurring deposits), those fractions will be sold to cash automatically during the transfer. To stay fully invested, consider selling fractional positions to cash before initiating the transfer.

The entire process is digital — no paper forms to print, no mailing, no medallion signatures.3 Because the assets remain within the same institution, the transfer avoids the weeks of inter-institution processing that traditional banks require. If both accounts hold the same investments, an in-kind transfer may be possible.

To re-emphasize: $40,000 in FHSA contributions can grow to $78,000 over 12 years. The full balance transfers to an RRSP without using a dollar of contribution room.

What happens to your FHSA if you leave Canada?

A Canadian who becomes a non-resident can keep their FHSA open and continue contributing until the 15-year expiry — a set of rules that most guides get wrong.

What non-residents can do

A Canadian who becomes a non-resident for tax purposes after opening an FHSA is not forced to close the account.1 The account stays open, the investments continue growing tax-free, and the non-resident can even continue making contributions using any accrued participation room. Those contributions can be deducted against any Canadian-source income they still file for (rental income, residual business income, etc.).

What non-residents cannot do

The restriction is on qualifying withdrawals. A non-resident cannot make a tax-free withdrawal to purchase a home — whether that home is in Canada or abroad. The “qualifying withdrawal” provision requires Canadian tax residency at the time of withdrawal.

The non-resident withdrawal tax

If a non-resident withdraws FHSA funds as cash (rather than rolling to an RRSP), the entire amount is subject to Part XIII non-resident withholding tax — typically 25%, though bilateral tax treaties between Canada and the non-resident’s country may reduce this rate.4

On a $60,000 FHSA balance, a 25% withholding tax means $15,000 lost immediately upon withdrawal. Under the Canada-US tax treaty, the rate drops to 15% — still $9,000 gone on that same balance. Most other major treaties land in the 15-25% range.

One exception worth flagging: US citizens and dual citizens should consult a cross-border tax specialist before relying on the “keep it open” strategy. Unlike RRSPs, the FHSA is not recognized as tax-sheltered by the IRS — meaning US persons may owe US tax on FHSA investment growth even while it remains tax-free in Canada.

The “Shadow RRSP” strategy

We use the term “Shadow RRSP” because the FHSA functions as a hidden second retirement account for non-residents — one that compounds tax-free and converts to actual RRSP space on demand.

The strategy we recommend for departing Canadians: leave the FHSA untouched. Let the investments compound tax-free for the full remaining life of the account, up to the 15-year expiry. Before the deadline, execute a direct transfer into a Canadian RRSP (which non-residents can also maintain).

This defers all taxation until RRSP decumulation — potentially decades later. By that point, the non-resident may:

- Have returned to Canada and can withdraw at Canadian marginal rates

- Be retired in a lower-tax jurisdiction with a favorable treaty rate

- Be in a lower income bracket, reducing the effective tax on RRSP withdrawals

The FHSA-to-RRSP rollover transforms what appears to be a “locked Canadian housing trap” into a globally portable, long-term tax-deferral vehicle. The strategy provides long-term tax deferral built directly into the standard Canadian tax code — no complex structuring required.

One filing detail to track: when you take a non-qualifying (taxable) withdrawal, Wealthsimple issues a T4FHSA slip reporting the full amount in Box 22. If you hold both a self-directed and a managed Wealthsimple FHSA, the platform generates separate T4FHSA slips for each — they do not consolidate onto a single document. Check both account tabs before filing.

The bottom line: the FHSA is a no-lose account

The Wealthsimple FHSA is structured so that every possible outcome works in your favor:

- You buy a home — withdraw tax-free, no repayment, keep the full amount

- You decide not to buy — roll everything into your RRSP above your normal limit, tax-free

- You leave Canada — keep the account compounding, roll to RRSP before expiry, defer tax indefinitely

- You change your mind years later — the account stays open for 15 years, giving you a decade-plus window to decide

Ben Reeves, Chief Investment Officer at Wealthsimple, told Investment Executive:

“What we’re hearing from investors is that they really value the flexibility that the FHSA provides, where if you don’t end up buying a home, you’re able to [transfer it to your RRSP].”5

The only losing move is not opening the account at all. Every year without an open FHSA is $8,000 of contribution room permanently forfeited — room that would either become a tax-free home purchase or bonus RRSP space.

If you have not opened an FHSA yet, the Wealthsimple FHSA Guide covers the full setup process. For the $100,000 combined strategy with the Home Buyers’ Plan, see the FHSA + HBP down payment guide. And for complex eligibility scenarios, see the FHSA eligibility edge cases. To decide which registered account to prioritize, see TFSA vs RRSP vs FHSA: Which First?.

Frequently asked questions

What happens to FHSA money if you never buy a home?

You can transfer the entire FHSA balance — contributions plus all investment growth — directly into your RRSP or RRIF at any time before the 15-year expiry. This transfer is tax-free and does not consume your RRSP contribution room. The FHSA effectively becomes bonus RRSP space above your normal lifetime limit.

Does transferring an FHSA to an RRSP use contribution room?

No. The FHSA-to-RRSP rollover is explicitly independent of your RRSP deduction room. If you have $0 of available RRSP room and $80,000 in your FHSA, the full $80,000 transfers into your RRSP without penalty or over-contribution.

Does the FHSA automatically close after 15 years?

The FHSA must be closed by December 31 of the 15th anniversary year of its opening (or the year you turn 71, whichever comes first). It does not auto-liquidate. You must initiate the closure — either by making a qualifying withdrawal, transferring to an RRSP/RRIF, or withdrawing as taxable income. Failing to act by the deadline results in the balance being deemed taxable income.

Can you keep an FHSA open after leaving Canada?

Yes. A non-resident can keep the FHSA open, maintain investments, and even continue contributing using accrued room. However, non-residents cannot make a qualifying (tax-free) withdrawal. Cash withdrawals while abroad are subject to 25% non-resident withholding tax (potentially reduced by tax treaty). The optimal strategy is to leave the funds compounding and roll into an RRSP before the 15-year expiry.

Can you transfer your FHSA to an RRSP before the 15-year deadline?

Yes. You can transfer at any time — there is no requirement to wait. If you decide at year 3 or year 8 that you will not buy a home, initiate the rollover immediately. On Wealthsimple, you can initiate this through the app — the platform routes you to the RC721 form via DocuSign for electronic signature.

Is a taxable FHSA withdrawal ever the right choice?

Rarely. A non-qualifying (taxable) withdrawal adds the full amount to your income for the year, potentially pushing you into a higher tax bracket. In almost every scenario, rolling the balance into your RRSP is preferable — you defer the tax until RRSP decumulation at retirement, when your marginal rate is typically lower.

Sources

Footnotes

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.