The $100K Down Payment Strategy: Using the FHSA and HBP Combined in 2026

Carry-forward timing, deduction deferral math, and the HBP repayment catch — how to actually execute the FHSA + HBP strategy without leaving money on the table.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: You do not have to choose between the FHSA and the HBP — the CRA lets you use both for the same home purchase. Combined limit: $100,000 solo, $200,000 as a couple. The FHSA withdrawal is permanent and tax-free; the HBP is a 15-year loan from your RRSP.

- FHSA: $40,000 max, no repayment, fully tax-free

- HBP: $60,000 max from your RRSP, must repay over 15 years

- Defer your FHSA deduction to a higher tax bracket for up to $10,000 more in refunds

How Is the FHSA Different From the Home Buyers’ Plan?

The FHSA and the Home Buyers’ Plan are separate programs with different mechanics — the FHSA is a standalone registered account you contribute to directly, while the HBP is a withdrawal provision that lets you borrow from an existing RRSP. The most important difference: FHSA withdrawals are permanently tax-free with no repayment, while HBP withdrawals must be repaid over 15 years or the missed amount becomes taxable income.

| Feature | FHSA | Home Buyers’ Plan (HBP) |

|---|---|---|

| Source of funds | Standalone registered account | Withdrawal from your RRSP |

| Maximum amount | $40,000 lifetime | $60,000 per person |

| Tax on contributions | Deductible (same as RRSP) | Already deducted when contributed to RRSP |

| Tax on withdrawal | $0 — permanently tax-free | $0 upfront, but must repay over 15 years |

| Repayment required | None | 1/15th per year for 15 years |

| Missed repayment | N/A | That year’s amount added to taxable income |

| Investment growth | Withdrawn tax-free | Must repay the full withdrawal, not growth |

The critical insight most guides miss: you do not have to choose one or the other. The CRA allows both for the same home purchase.

Do you have to choose between the FHSA and the Home Buyers’ Plan?

The FHSA and the Home Buyers’ Plan (HBP) can be used together for the same qualifying home purchase — despite being frequently presented as competing programs on personal finance forums and even by some bank advisors. The assumption is that since both target first-time home buyers, using one disqualifies you from the other.

This is wrong. The Income Tax Act contains no provision restricting the combined use of these two programs.1 They operate through entirely separate mechanisms — the FHSA is a standalone registered account,2 while the HBP is a withdrawal provision within an existing RRSP — and neither references the other as a condition of eligibility.

A first-time buyer who has both a funded FHSA and a funded RRSP can make a qualifying FHSA withdrawal and an HBP withdrawal in the same calendar year, directed toward the same property purchase, with no conflict.

What is the maximum combined FHSA and HBP down payment?

The FHSA and HBP together provide a $100,000 tax-sheltered down payment for a solo buyer ($200,000 for a couple).

As Aaron Hector, Private Wealth Advisor at CWB Wealth Management, explained in Yahoo Finance Canada, couples can reach “$100,000 in pre-tax dollars — or $200,000 as a couple,” and unlike the HBP, “any growth on the FHSA can come out tax-free as well.”3

In Toronto, Vancouver, or Montreal, $200,000 is enough for a 20% down payment on a $1,000,000 property — the threshold that eliminates CMHC mortgage insurance premiums entirely. That insurance savings alone can exceed $30,000 on a high-ratio mortgage. For properties above $1M, the insured mortgage cap was expanded from $1 million to $1.5 million in December 2024, meaning the FHSA + HBP combination can significantly reduce premiums on homes up to $1.5M as well.

Hit 20% down and the CMHC insurance premium disappears — that’s over $30,000 back in your pocket on a $1M property.

How does FHSA carry-forward work before a home purchase?

The FHSA contribution room only starts accumulating from the year you open an account. Unlike the TFSA, there is no retroactive room. This makes account opening timing critical — especially when coordinating with an HBP withdrawal that requires years of Wealthsimple RRSP contributions.

The optimal approach for someone 3-5 years away from a purchase:

Year 1 — Open the FHSA immediately, even with $0. The moment the account is registered, the CRA grants $8,000 of room for that calendar year. If you cannot contribute, the unused $8,000 carries forward.

Years 2-5 — Contribute the maximum each year. With the carry-forward from Year 1, your Year 2 maximum is $16,000 ($8,000 new + $8,000 carried). From Year 3 onward, contribute $8,000 per year until you hit the $40,000 lifetime cap.

Simultaneously — Build the RRSP for HBP. While funding the FHSA, also contribute to your RRSP to build the $60,000 you will withdraw through the HBP. These contributions generate their own separate tax deductions — and if you are on Wealthsimple, their RRSP match program can stretch those contributions further. One CRA rule to plan around: RRSP contributions must sit in the account for at least 90 days before an HBP withdrawal, or you lose the tax deduction on that specific amount. If you are making last-minute contributions to top up your RRSP for the HBP, ensure the 90-day window closes before your planned withdrawal date.

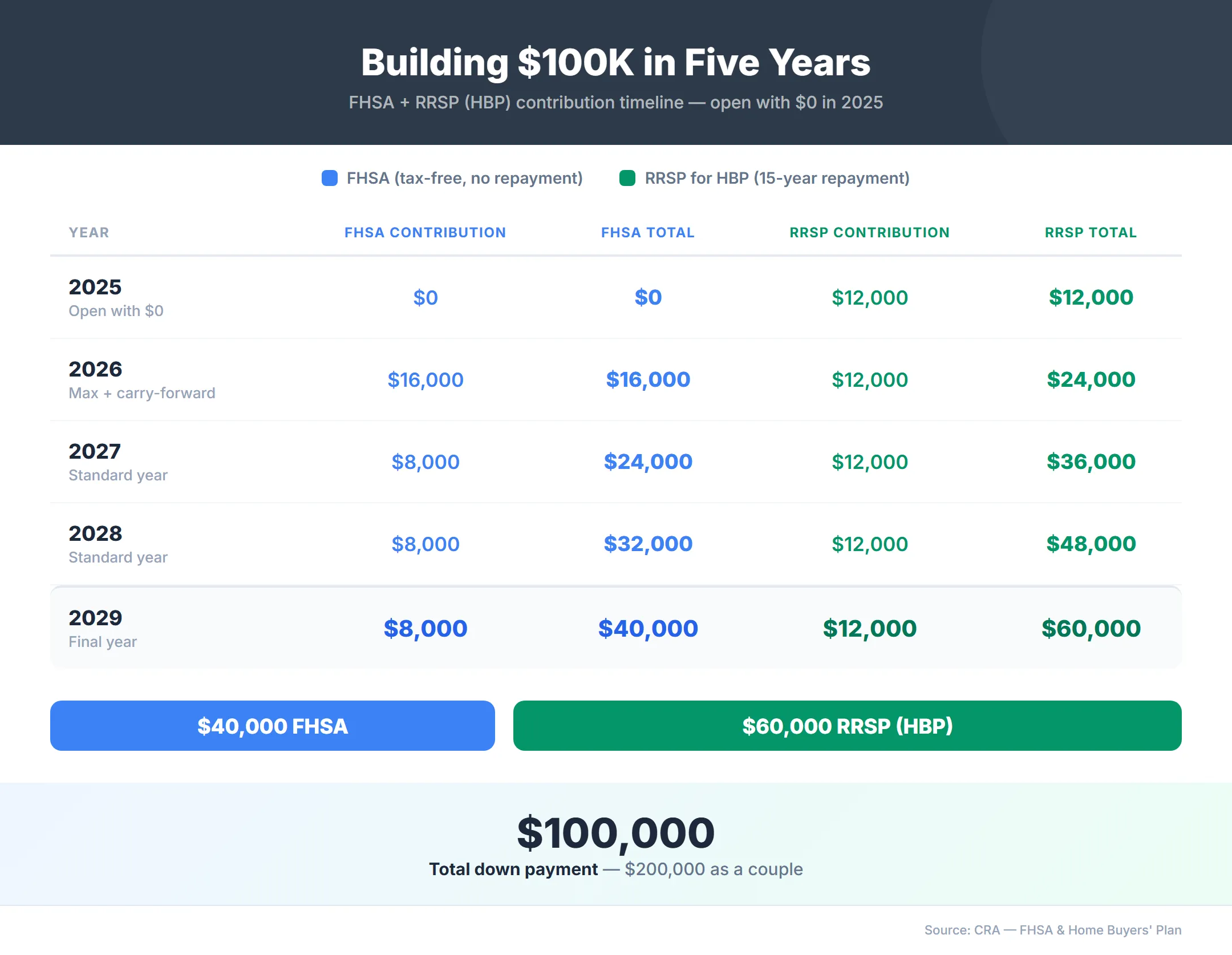

Here is the contribution room math for someone who opens with $0 in 2025:

By 2029, this buyer has $40,000 in the FHSA and $60,000 earmarked in the RRSP — the full $100,000, built over five years with annual contributions ranging from $12,000 to $28,000.

How does FHSA deduction deferral work?

Both FHSA and RRSP contributions generate tax deductions, but you are not required to claim them in the same year you contribute. This creates a deferral strategy for anyone currently in a low tax bracket who expects their income to rise significantly.

The mechanics: Make your FHSA contribution to get the money into the tax-free compounding environment immediately. Report it on Schedule 15 of your tax return. On Line 20805, claim $0 as your deduction. The unclaimed deduction carries forward indefinitely until you choose to use it.

The math at different brackets:

| Marginal Tax Rate | Tax Savings on $8,000 FHSA Deduction | Tax Savings on $60,000 HBP (RRSP) Deduction |

|---|---|---|

| 20% (entry level) | $1,600 | $12,000 |

| 33% (mid-career) | $2,640 | $19,800 |

| 45% (high earner) | $3,600 | $27,000 |

A medical resident contributing $8,000 to the FHSA at a 20% bracket who defers the deduction until their staff physician years at 45% gains an extra $2,000 from that single year’s contribution. Applied across the full $40,000 FHSA lifetime limit, the deferral strategy recovers an additional $10,000 in tax refunds compared to claiming immediately.

The same logic applies to RRSP contributions earmarked for the HBP. The RRSP deduction can also be carried forward, meaning both sides of the $100,000 strategy benefit from deferral.

How do you open both an FHSA and RRSP for the HBP on Wealthsimple?

Wealthsimple lets you open both an FHSA and an RRSP within the same app, fund them simultaneously, and eventually execute both withdrawals through a single interface — all with $0 commissions and $0 transfer-out fees.

Setting up the FHSA

- Log into Wealthsimple (or sign up with a referral code 9C6DMQ for a $25 cash bonus)

- Select Add Account and choose FHSA

- Pick self-directed ($0 fees) or managed (0.4-0.5% fee)

- Confirm your first-time buyer declaration

- Fund via bank transfer or set up automatic deposits

Check the Wealthsimple promotions page for additional bonuses you can stack with the referral code.

Setting up the RRSP for HBP

- From the same Wealthsimple account, select Add Account and choose RRSP

- Pick self-directed or managed

- Fund alongside your FHSA — both generate separate tax deductions

When you are ready to purchase, both the FHSA qualifying withdrawal and the HBP RRSP withdrawal are initiated through the Wealthsimple app. The FHSA withdrawal is straightforward — request the funds, they arrive tax-free. The HBP withdrawal requires a T1036 form (Home Buyers’ Plan Request to Withdraw Funds from an RRSP), which Wealthsimple processes digitally.1

One timing detail that catches first-time buyers off guard: real estate deposits are typically due within 24 hours of an accepted offer, but FHSA and HBP withdrawals take 3-5 business days to reach your chequing account. Managed accounts may take 10-15 business days because the robo-advisor must liquidate positions first. After the withdrawal settles, transferring funds to your bank for the closing bank draft adds another 3-7 business days. Plan to front the deposit from savings or a line of credit, then reimburse yourself when the withdrawal settles.

For a full walkthrough of account setup, managed vs. self-directed options, and Wealthsimple’s fee structure, see our Wealthsimple FHSA Guide.

Do you have to repay the FHSA or the HBP?

FHSA qualifying withdrawals require zero repayment, while HBP withdrawals must be repaid to your RRSP over 15 years — the critical difference that most comparisons gloss over. The money from the FHSA leaves the account and belongs to you permanently. No forms, no annual minimums, no 15-year schedule.

HBP withdrawals are a loan from your own RRSP. You must repay the full amount back into your RRSP over 15 years, starting in the second calendar year after the withdrawal.1 The minimum annual repayment is 1/15th of the total withdrawn.

As Jamie Golombek, Managing Director of Tax and Estate Planning at CIBC Private Wealth, warned in the same Yahoo Finance Canada interview, “If you forget that, then you’re going to be short $4,000 a year potentially and your retirement will suffer.”4

The HBP repayment math

On a maximum $60,000 HBP withdrawal:

| Detail | Amount |

|---|---|

| Total HBP withdrawal | $60,000 |

| Annual minimum repayment | $4,000/year |

| Repayment period | 15 years |

| What happens if you miss a year | $4,000 added to taxable income |

Missing a $4,000 repayment at a 33% marginal rate costs you $1,320 in extra tax that year. Miss three years and you have effectively paid $3,960 in penalties — exceeding one full year of FHSA tax savings at a 33% rate.

The strategic priority

Because the FHSA has no repayment obligation, the optimal deployment order for a home purchase is:

- Withdraw FHSA first — the full $40,000, tax-free, permanently yours

- Withdraw HBP second — only the amount you actually need beyond the FHSA, understanding the 15-year repayment commitment

- Minimize HBP if possible — if your FHSA plus personal savings cover the down payment, consider withdrawing less than the $60,000 HBP maximum to reduce the repayment burden

A buyer who needs $70,000 for a down payment is better served withdrawing $40,000 from the FHSA (no repayment) and $30,000 from the HBP ($2,000/year repayment for 15 years) than splitting it evenly. The FHSA should always be depleted first.

The opportunity cost of HBP repayment is real: the $4,000 you repay to your RRSP each year is money you cannot direct toward your TFSA, emergency fund, or mortgage prepayments. If you invested that $4,000 annually in a TFSA at a 7% average return, you would accumulate roughly $100,000 over 15 years. The HBP withdrawal is not free — it carries a significant long-term opportunity cost.

The bottom line

The FHSA and the Home Buyers’ Plan are not competitors — they are complements. Used together, they create a $100,000 solo ($200,000 couple) tax-sheltered homebuying fund that no other combination of Canadian accounts can match.

The action items are straightforward:

- Open the FHSA now (even with $0) to start the contribution room clock — every year without an open account is $8,000 of room permanently lost

- Fund both the FHSA and RRSP in parallel to build toward the combined $100,000

- Defer deductions if you are in a low tax bracket today

- Withdraw FHSA first at purchase time to minimize HBP repayment obligations

For eligibility details and complex scenarios (spouse owns a home, divorce, inherited property, newcomers), see our FHSA eligibility edge cases guide. For what happens if your plans change and you never buy, see the FHSA exit strategy guide.

Frequently asked questions

Can you use the FHSA and Home Buyers’ Plan together?

Yes. The CRA explicitly permits the simultaneous use of both the FHSA and the Home Buyers’ Plan for the same qualifying home purchase. There is no rule requiring you to choose one or the other. A solo buyer can deploy up to $100,000 in tax-sheltered capital ($40,000 from the FHSA plus $60,000 from the HBP).

What is the maximum tax-free down payment for a first-time buyer in Canada?

A solo first-time buyer can access up to $100,000 tax-free by combining the FHSA ($40,000 lifetime limit) and the Home Buyers’ Plan ($60,000 from an RRSP). A couple where both partners qualify can reach $200,000 combined.

Do you have to repay the FHSA like the Home Buyers’ Plan?

No. FHSA qualifying withdrawals are permanent and tax-free with no repayment obligation. The HBP withdrawal is structured as a loan from your RRSP that must be repaid over 15 years. If you miss a minimum annual repayment, that amount is added to your taxable income for the year.

What is the HBP minimum annual repayment?

The HBP repayment is calculated as 1/15th of the total amount withdrawn per year, starting in the second year after the withdrawal. To be concrete: if you withdraw in 2026, your first repayment of $4,000 is due with your 2028 tax return. On a $60,000 HBP withdrawal, the minimum annual repayment is $4,000 per year for 15 years back into your RRSP.

Can you open an FHSA with $0 to lock in contribution room?

Yes. FHSA contribution room only starts accumulating from the year you open an account. Opening with a $0 deposit locks in $8,000 of room for that calendar year. If you do not contribute, the $8,000 carries forward (up to $8,000 max carry-forward), giving you $16,000 of available room the following year.

Should you claim the FHSA deduction immediately or defer it?

It depends on your current tax bracket. If you are in a low bracket now but expect higher income soon (medical residents, law students, junior professionals), contribute now to capture tax-free growth but carry the deduction forward. An $8,000 deduction at 45% returns $3,600 versus $1,600 at 20% — a $2,000 difference from timing alone.

Sources

Footnotes

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.