FHSA Eligibility: The 4 Edge Cases Most Guides Get Wrong

The CRA's 'first-time buyer' rule is about where you lived, not what you owned. Four scenarios — from common-law to inherited cottages — where the answer surprises most Canadians.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

TL;DR: The CRA’s “first-time buyer” test hinges on principal residency, not property title. Your spouse can own a home and you still qualify. Inherited property does not disqualify you. Divorce resets your eligibility after 4 years. Work permit holders are eligible.

- Spouse owns a home you never lived in as your primary residence — you qualify

- Inherited a cottage or fractional share — you qualify if you never lived there

- Divorce transfers via CRA Form RC723 are tax-free and preserve contribution room

This guide covers all four edge cases with CRA sources, the specific mistakes to avoid, and how each situation plays out on the Wealthsimple platform. For the basic FHSA overview — contribution limits, fees, how to open — see our Wealthsimple FHSA Guide.

What are the basic FHSA eligibility rules?

The CRA requires three things to open an FHSA: you must be a Canadian resident for tax purposes, between 18 and 71 years old, and a first-time home buyer.1

The first-time buyer test is strictly time-based. You qualify if you have not lived in a qualifying home that you or your spouse/common-law partner owned as your principal place of residence in the current calendar year or the four preceding calendar years.

Denise Laframboise, a mortgage broker in Brooklin, Ontario, explained in MoneySense:

“It truly depends on the program. Each program has its own criteria for [qualifying as a] first-time home buyer. It isn’t a one-size-fits-all across every program and every provincial or municipal incentive.”2

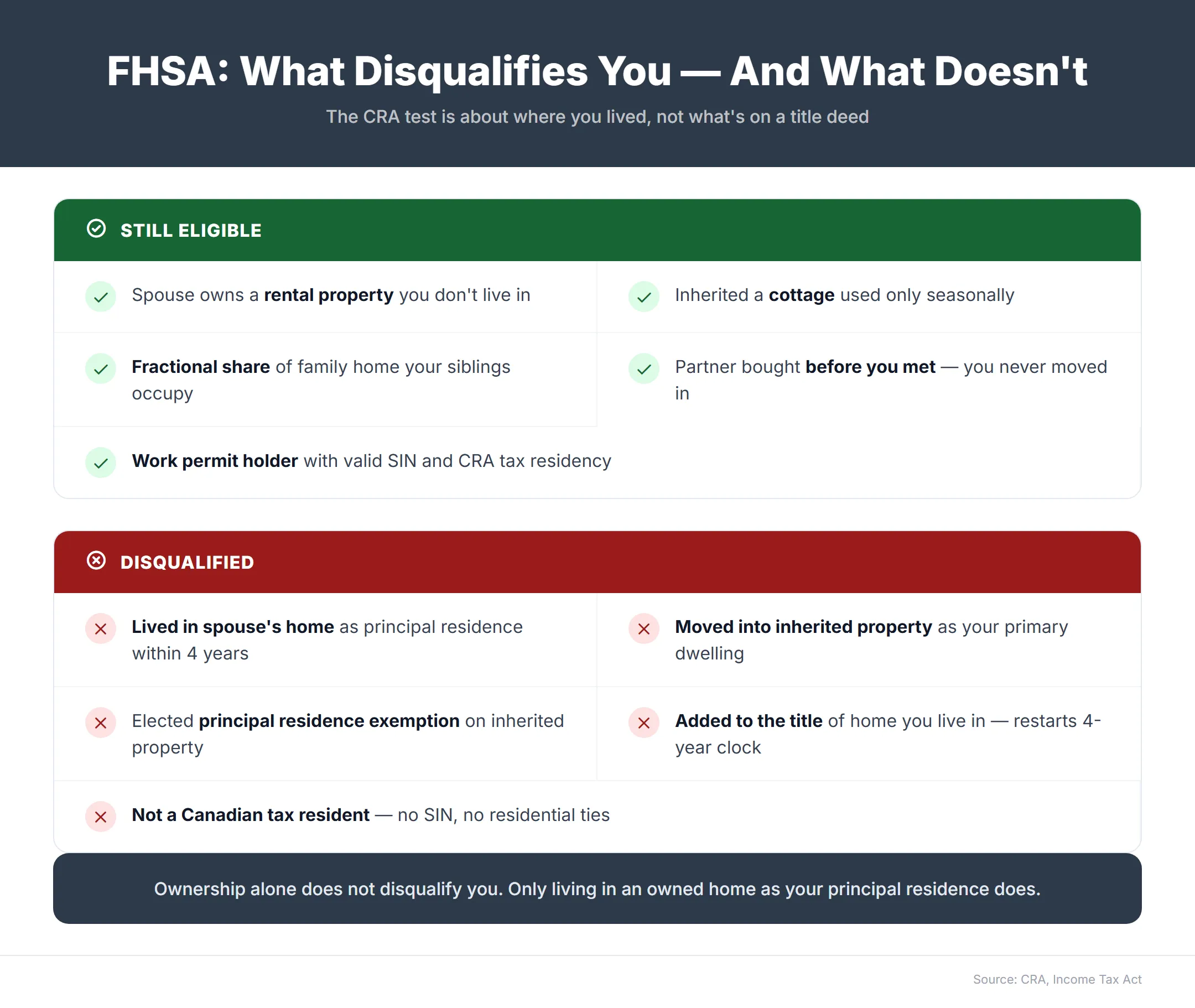

Two terms carry all the weight: “lived in” and “principal.” Ownership alone does not disqualify you. Occupancy of property that is not your principal residence does not disqualify you. Only living in an owned home as your primary dwelling triggers the restriction.

One timing nuance the CRA buries in the withdrawal rules: the first-time buyer test ignores the 30 days immediately preceding a qualifying withdrawal. If you take possession of your new home and request the FHSA withdrawal within that 30-day window, you still qualify — even though you are technically living in a home you own.

Every edge case below turns on this distinction.

Can I open an FHSA if my spouse owns a home?

Yes, you are eligible to open a Wealthsimple FHSA provided you have not lived in your spouse’s property as your principal residence.1

The common assumption is that marriage or common-law status automatically consolidates your financial eligibility with your partner’s — if they own a home, you own a home. This is incorrect for the FHSA. The CRA evaluates your principal residence history, not your partner’s property portfolio.

When spousal ownership does not block you

- Your partner owns a rental property or investment property that neither of you lives in

- Your partner bought a home before you became a couple and you have never moved in

- You maintain separate principal residences due to work (long-distance employment, military posting, etc.)

- Your partner owns a cottage used only seasonally while you rent an apartment as your primary dwelling

In all of these situations, you are a first-time home buyer because you have not lived in a home you or your spouse owned as your principal residence.

The critical timing distinction

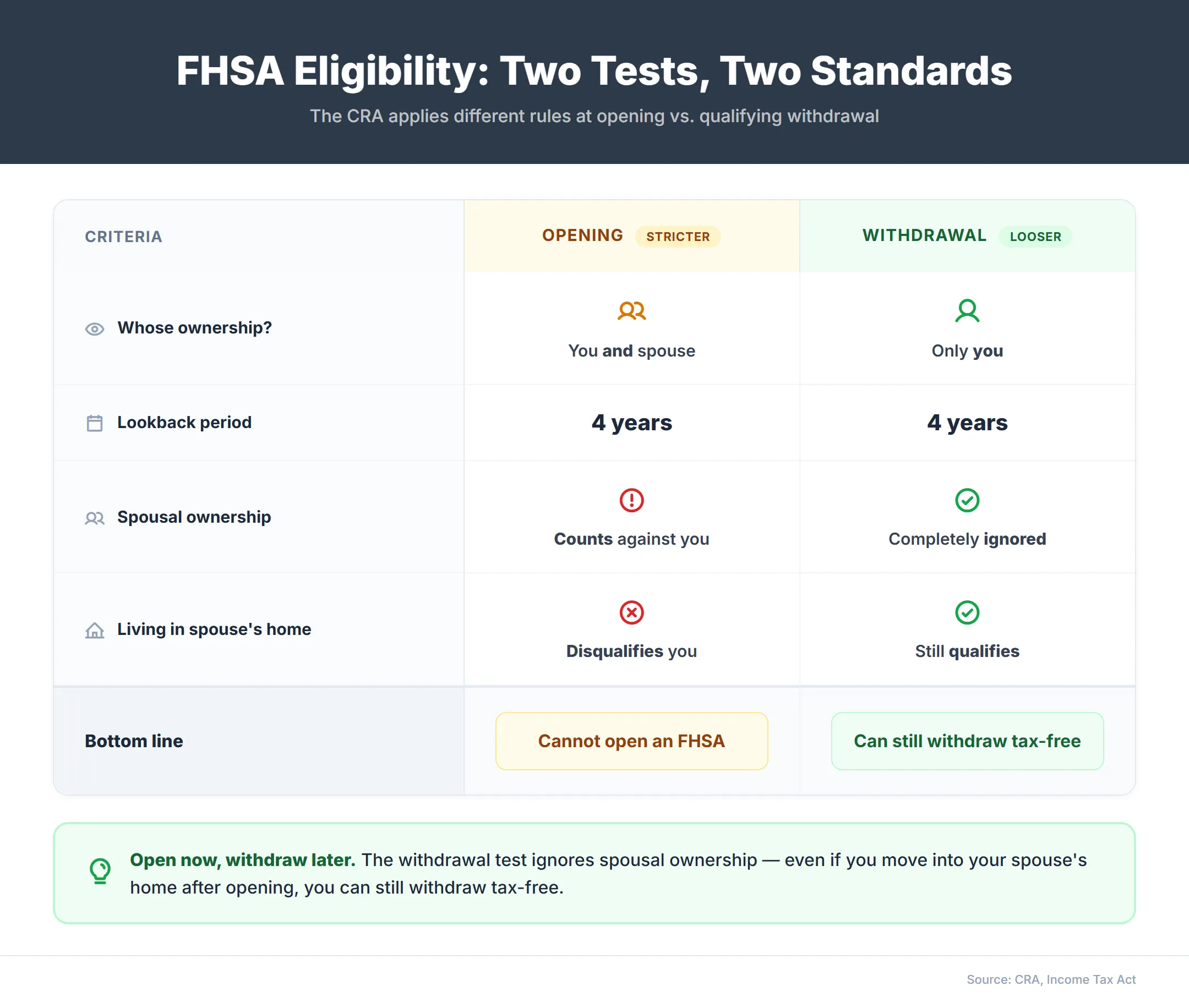

The FHSA has two separate eligibility tests, and they apply at different moments:

At opening: You must be a first-time buyer at the time the account is opened. The CRA checks whether you or your spouse owned a home you lived in as your principal residence. Once the account is open and registered, your $8,000 of annual room is locked in.

At withdrawal: You must be a first-time buyer again at the time of the tax-free withdrawal — but the definition is looser. The withdrawal test only checks whether you owned your principal residence. Spousal ownership is ignored entirely.1

What happens to FHSA assets during a divorce?

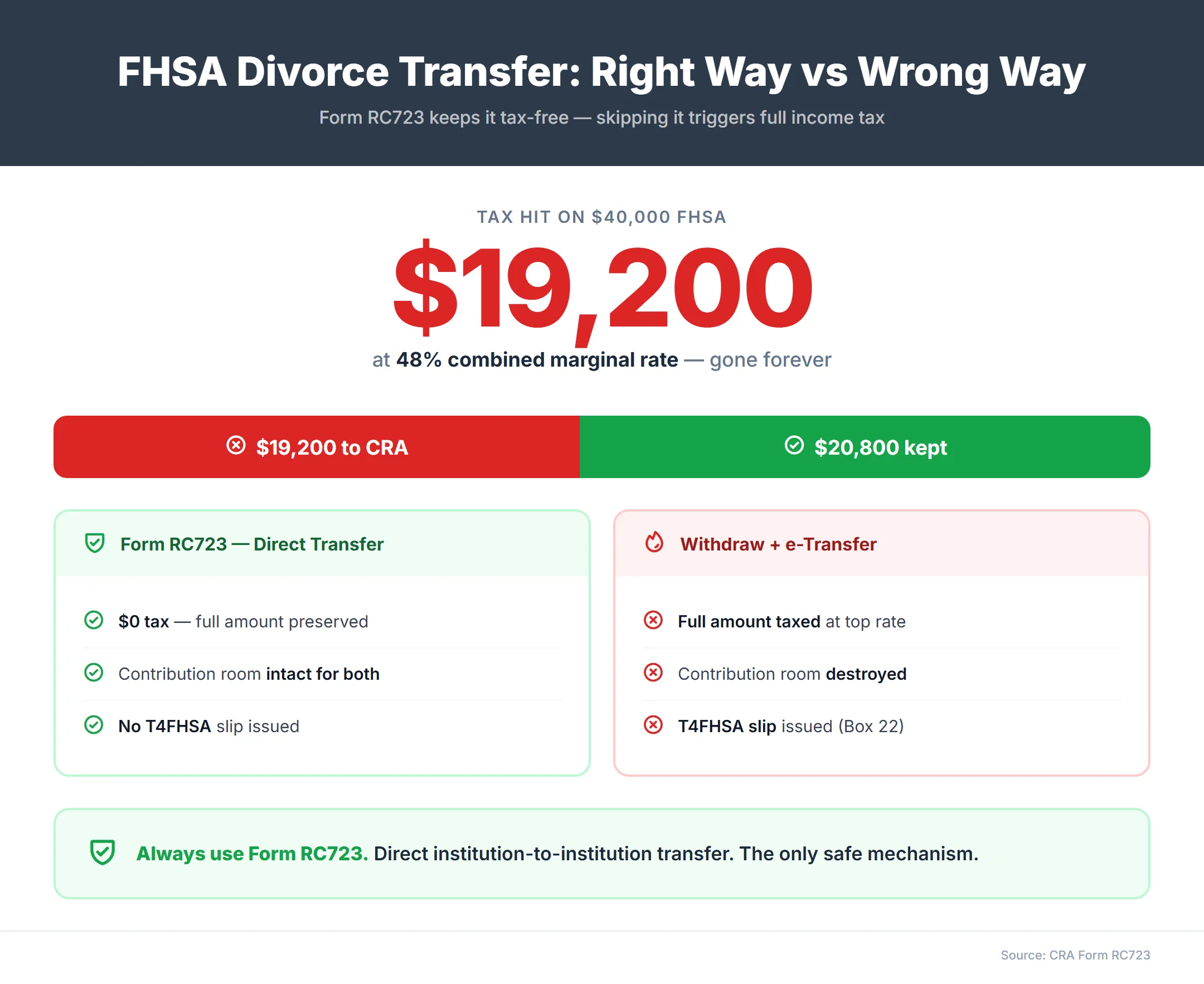

FHSA assets can be transferred directly to a former spouse’s FHSA, Wealthsimple RRSP, or RRIF completely tax-free using Form RC723.3

This transfer does not consume the recipient’s contribution room, provided they are legally entitled to the amount under a court decree or separation agreement. Two absolute conditions must be met:

- The recipient must be legally entitled to the amount under a court decree, order, or written separation agreement

- The transfer amount cannot exceed the total fair market value of all assets in the transferor’s FHSA minus any excess (over-contribution) amount

The RC723 Shield

CRA Form RC723 — Transfer from an FHSA to another FHSA, RRSP or RRIF on Breakdown of Marriage or Common-law Partnership — is the only safe mechanism for this transfer.3 The form instructs the financial institution to execute a direct, institution-to-institution transfer that preserves the tax-sheltered status of every dollar.

On Wealthsimple, submitting RC723 to the back office initiates the transfer through internal systems. Both parties maintain their registered accounts intact, and the CRA records the movement as a qualifying transfer rather than a taxable event.

What if the transfer exceeds the FMV limit?

If the court-ordered amount exceeds the fair market value of the FHSA minus any over-contributions, the excess is treated as a new contribution to the recipient’s account. This can push the recipient into an over-contribution state, triggering a 1% monthly penalty. Before executing a large divorce-related transfer, both parties should verify the FHSA balance and any excess amounts with their accountant. If the recipient does not yet have an FHSA, opening one on Wealthsimple takes minutes — see the Wealthsimple promotions page for current signup bonuses.

Does inheriting property disqualify me from the FHSA?

Inheriting a family cottage does not disqualify you from opening an FHSA — as long as you never used it as your principal residence.

No, inheriting legal title or a fractional share of a property does not automatically disqualify you unless you occupy it as your principal residence.1

The eligibility test is based on residency, not title registration — so you can hold a cottage, a portion of a family home, or a share of a rental building and still qualify for a Wealthsimple FHSA.

When inherited property does not block you

- A vacation cottage used only seasonally while you rent year-round elsewhere

- A fractional share of a family home that your siblings occupy as their primary dwelling

- A rental property generating income but never occupied by you

- An inherited unit in a different city or province that you have never lived in

In each case, the inherited property is not your principal place of residence. You remain a first-time home buyer under the CRA definition, and you can open and fund a Wealthsimple FHSA without restriction.

Be aware that some real estate lawyers incorrectly tell beneficiaries they are immediately disqualified the moment they inherit a title. This is wrong. Holding title to property you do not occupy as your principal residence has no impact on your FHSA eligibility — the CRA test is residency-based, not title-based.

When inherited property does block you

If you move into the inherited property full-time — perhaps to save on rent or because it suits your lifestyle — it becomes your principal residence. At that moment, you lose your first-time buyer status, and any future qualifying withdrawal from the FHSA is blocked until four full years after you stop living there.

The principal residence election conflict

This is the advanced trap. If you elect an inherited property as your principal residence to shelter it from capital gains tax when you eventually sell it, that election inherently confirms that you occupied it as your principal dwelling. This destroys your FHSA qualifying withdrawal eligibility for the four-year lookback period.

You may face a strategic choice: use the principal residence exemption to shelter the cottage from capital gains tax, or preserve your FHSA withdrawal eligibility to buy your own home tax-free.4 Both are powerful tax-sheltering mechanisms, but they cannot apply simultaneously. Consult a tax professional before making this election if you hold both an FHSA and inherited property.

Can temporary residents open an FHSA in Canada?

Yes, temporary residents are eligible to open an FHSA provided the CRA considers them a resident of Canada for tax purposes.1

Immigration status — permanent resident, work permit, study permit — is irrelevant. Having a valid Social Insurance Number and meeting tax residency requirements is the only test.

How the CRA determines tax residency

The CRA does not use your IRCC visa category. Instead, they assess:

- Significant residential ties — a home in Canada, a Canadian spouse or dependents, personal property, social ties

- The 183-day rule — physical presence in Canada for 183 days or more in a calendar year generally establishes tax residency

Most full-time workers in Canada with a SIN, a Canadian address, and a Canadian employer meet these criteria, regardless of their visa type.

Opening on Wealthsimple with a SIN starting with 9

Wealthsimple’s automated onboarding process accommodates temporary residents with SINs beginning with 9. The account opening flow is identical to any other user — you provide identification, confirm your eligibility declaration, and the FHSA is registered with the CRA. New users can apply a Wealthsimple referral code during signup for a $25 cash bonus.

One operational detail to watch: Wealthsimple’s systems are tied to your SIN expiry date. If your work permit expires and you have not uploaded the renewal documents, your account may be frozen until the updated SIN is on file. Always upload renewed documents before the old ones expire to avoid being locked out of trades.

The $8,000 annual deduction begins reducing your Canadian taxable income immediately. For a newcomer in a 33% combined marginal bracket, that is approximately $2,640 in tax savings per year — money that would otherwise go to the CRA. For a broader guide to navigating registered accounts as a newcomer — including TFSA contribution room rules and the residency trap — see our TFSA newcomers guide.

The exit strategy for temporary residents

The real anxiety for newcomers is not opening the account — it is what happens if they leave. The answer is more favorable than most expect:

- Keep the FHSA open after departure. Non-residents can maintain the account and continue investing tax-free.

- Continue contributing using any accrued participation room, deducting against Canadian-source income.

- Cannot make a qualifying withdrawal. The tax-free home purchase provision requires Canadian tax residency at the time of withdrawal.

- Cash withdrawal abroad triggers 25% non-resident withholding tax (reduced by treaty).

- The optimal move is the RRSP rollover — leave funds compounding, transfer to RRSP before the 15-year expiry, defer taxation indefinitely.

If you leave Canada and later return to buy a home, the CRA requires you to be a tax resident continuously from the date of your first qualifying withdrawal through to the date you acquire the property.1 Re-establishing residency the week before closing is not enough — plan the timeline accordingly.

For a detailed breakdown of the non-resident strategy, see the FHSA exit strategy guide.

The bottom line

FHSA eligibility is more permissive than most Canadians realize. The CRA’s first-time buyer definition tests principal residency, not property ownership, marital status, or immigration category. Understanding this distinction unlocks the account for people who incorrectly assumed they were disqualified.

The four verdicts:

- Spouse owns a home — you are eligible to open if you have never lived in it as your principal residence. At withdrawal, spousal ownership is ignored entirely — only your own ownership matters.

- Divorce asset division — use Form RC723 for a tax-free direct transfer. Never withdraw manually.

- Inherited property — eligible if you have never lived in the inherited property as your principal residence. Watch the principal residence election conflict.

- Newcomers and temporary residents — eligible if CRA considers you a tax resident. The FHSA doubles as a tax reduction tool with a built-in RRSP safety net.

For the full FHSA overview, contribution limits, and Wealthsimple setup instructions, see the Wealthsimple FHSA Guide. For the $100K combined strategy with the HBP, see the FHSA + HBP down payment guide. To decide which account to open next, see TFSA vs RRSP vs FHSA: Which First?.

Frequently asked questions

Can I open an FHSA if my spouse owns a home?

Yes, if you have not lived in a qualifying home owned by you or your spouse as your principal residence in the current year or the preceding four calendar years. If your spouse owns a rental property or a home you have never lived in, you are eligible to open an FHSA. The test is principal residency, not title ownership.

Does inheriting property disqualify me from the FHSA?

Not automatically. Inheriting a fractional share of a cottage, family home, or rental property does not disqualify you if you have never lived in that property as your principal residence. You can hold title to inherited real estate and still be a first-time home buyer under the CRA definition.

What happens to the FHSA in a divorce?

FHSA assets can be transferred directly to a former spouse’s FHSA, RRSP, or RRIF completely tax-free using CRA Form RC723. The transfer does not consume the recipient’s contribution room. Never withdraw and manually send the funds — that triggers a taxable withdrawal and destroys the contribution room for both parties.

Can temporary residents open an FHSA in Canada?

Yes. FHSA eligibility requires Canadian tax residency, not permanent residency or citizenship. Work permit holders with a valid SIN — including SINs starting with 9 — who are considered tax residents by the CRA can open and fund an FHSA on Wealthsimple.

Does the FHSA eligibility test apply at opening or at withdrawal?

Both, but the definitions differ. At opening, you must not have lived in a home owned by you or your spouse as your principal residence. At withdrawal, the test is looser — it only checks whether you owned your principal residence. Spousal ownership is ignored. Living in a home your spouse owns does not block a qualifying withdrawal.

Can I open an FHSA if my common-law partner owns a home?

The same rule applies as for married spouses. If you have not lived in your common-law partner’s home as your principal residence in the current year or the preceding four years, you are eligible. The CRA treats common-law partners (living together for 12+ continuous months) identically to married spouses for FHSA purposes.

Sources

Footnotes

Quote from Denise Laframboise, Mortgage Broker, LaframboiseMortgage.ca, given in a MoneySense interview on first-time home buyer eligibility. ↩

CRA — Form RC723: Transfer from an FHSA on Breakdown of Marriage ↩ ↩2

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.