TFSA for Newcomers to Canada: How Much Contribution Room Do You Actually Have?

Most newcomers assume they get the full $109,000. Your arrival year, visa type, and SIN each change the number — and overcontributing triggers an immediate 1% monthly penalty.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

Land on December 31 and you still get a full year of TFSA room — the CRA counts any arrival within the calendar year.

The Bottom Line: Your TFSA room starts from the year you became a Canadian tax resident — not the full $109,000 lifetime limit. A 2024 arrival means $21,000 of cumulative room in 2026. Overcontributing triggers a 1% monthly CRA penalty with no grace period.

- Room accumulates by tax residency year, not citizenship or visa type

- SIN starting with 9 (temporary residents) qualifies once you file a tax return

- December arrivals get a full year of room — even if you land on December 31

This guide covers exactly how much room you have based on your arrival year, the most common mistakes newcomers make, SIN eligibility rules for temporary residents, and how to open your first TFSA on Wealthsimple.

What TFSA Contribution Room Do Newcomers Actually Get?

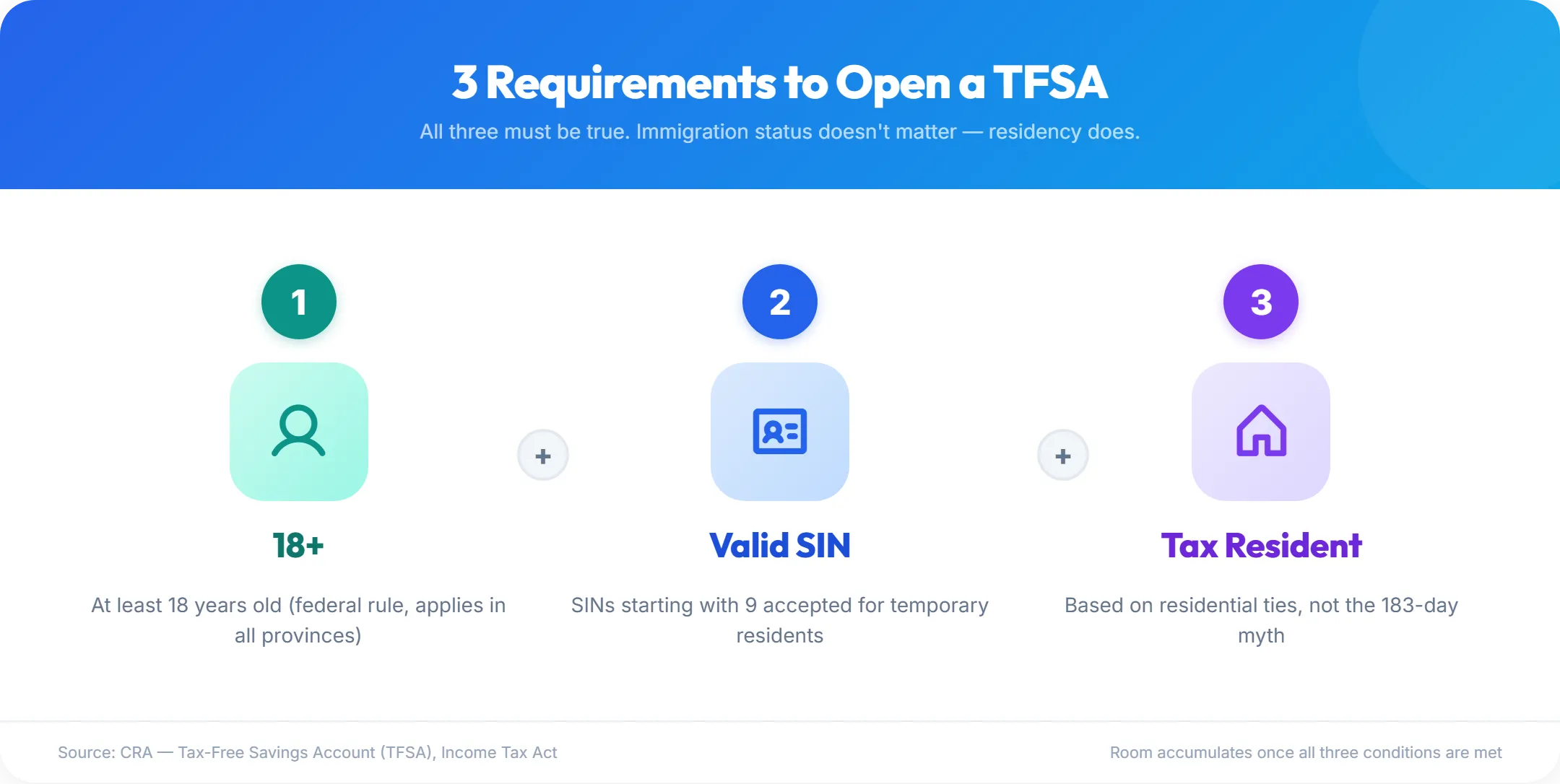

The CRA grants TFSA contribution room based on tax residency and age, not citizenship or immigration status.1 Three requirements must be met: you must be a tax resident of Canada, at least 18 years old, and hold a valid Social Insurance Number (SIN). Room accumulates for each calendar year all three conditions are true. The CRA does not backdate room for years you lived outside Canada.

Wilmot George, Managing Director of Tax and Estate Planning at Canada Life in Toronto, told Investment Executive:

“Many [Canadians] are still learning about the TFSA and how it works, and most are not trained in calculating TFSA contribution room, especially when withdrawals have occurred.”2

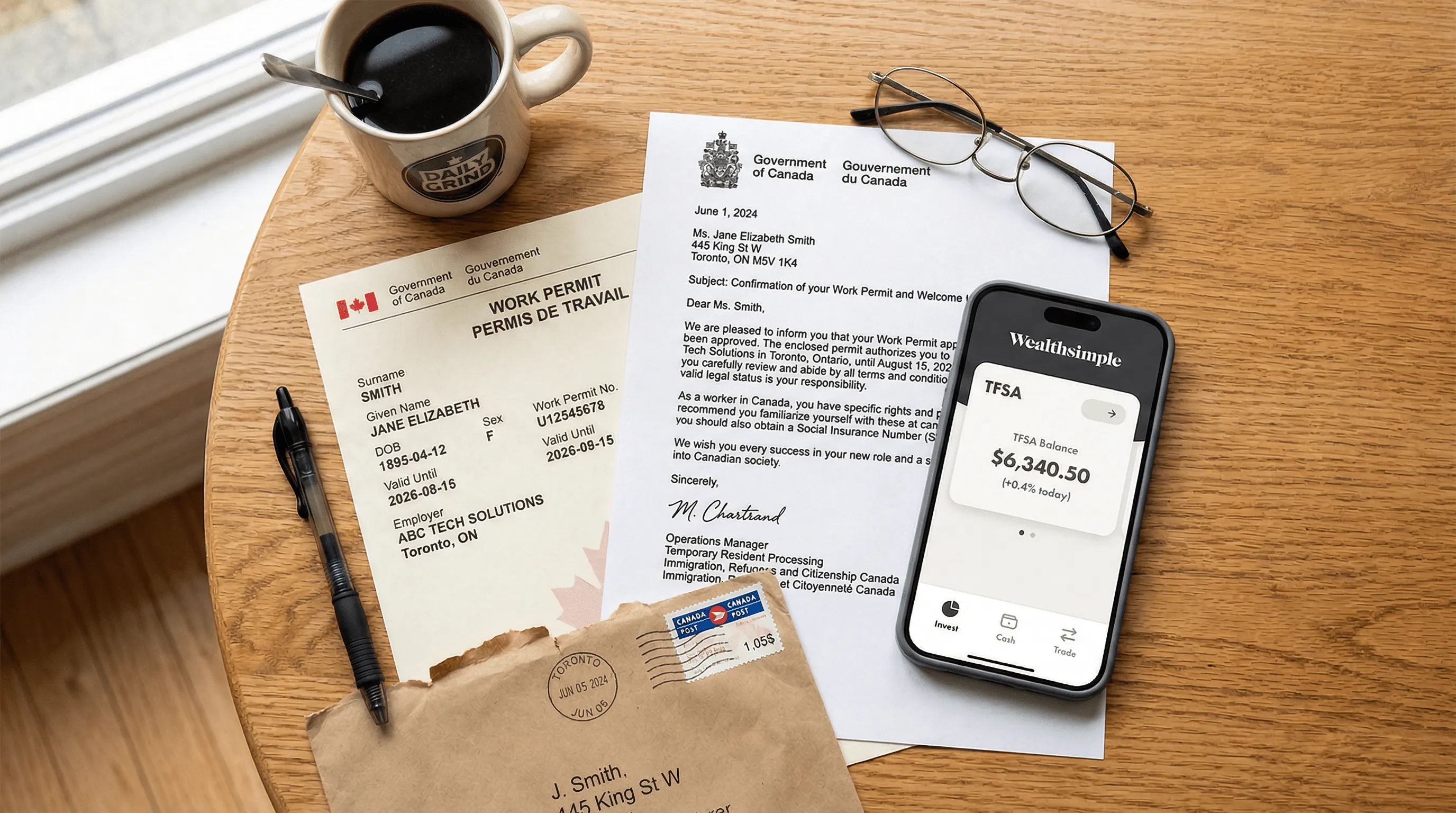

The most dangerous misconception among newcomers is believing they have access to the full $109,000 lifetime TFSA limit that appears in headlines and bank marketing. That number applies exclusively to individuals who have been eligible since the TFSA program started in 2009 — seventeen years of annual limits added together. A newcomer who became a tax resident in 2024 has $21,000 of cumulative room, not $109,000. Overcontributing based on the wrong figure triggers CRA penalties immediately.

The CRA determines tax residency based on significant residential ties — a home in Canada, a Canadian spouse or dependants, and economic connections — not your immigration visa category.3 A common misconception is the “183-day rule” — many newcomers assume they must be in Canada for 183 days before becoming a tax resident. In reality, you can establish tax residency on day one if you arrive with a work permit, sign a lease, and open a Canadian bank account. Permanent residents, work permit holders, and international students with strong residential ties can all qualify as tax residents and begin accumulating TFSA room.

How Much Room Do You Have by Arrival Year?

According to CRA guidelines, a newcomer who established Canadian tax residency in 2024 has $21,000 of cumulative TFSA contribution room available in 2026, calculated by adding the annual limit for each year from residency onward.

| Year Tax Residency Established | Limit That Year | Cumulative Room in 2026 |

|---|---|---|

| Pre-2009 (eligible since launch) | $5,000 | $109,000 |

| 2020 | $6,000 | $45,500 |

| 2021 | $6,000 | $39,500 |

| 2022 | $6,000 | $33,500 |

| 2023 | $6,500 | $27,500 |

| 2024 | $7,000 | $21,000 |

| 2025 | $7,000 | $14,000 |

| 2026 | $7,000 | $7,000 |

The annual TFSA limit has changed multiple times since 2009. It started at $5,000, jumped to a one-time $10,000 in 2015, and has been $7,000 since 2024.1 The federal government sets each year’s limit and indexes it to inflation in $500 increments.

Bookmark this table or screenshot it before your first contribution — most guides only list annual limits and leave newcomers to calculate cumulative room on their own.

If you are deciding between a Wealthsimple TFSA, an RRSP, and an FHSA as a new resident, your available room in each account changes the math. See our comparison of all three accounts for a decision framework based on income and homebuying plans.

Does the Calendar Year Rule Affect Newcomers?

The CRA does not prorate TFSA contribution room by month of arrival — if you become a tax resident at any point during a calendar year, you receive the full annual limit for that entire year.1

A newcomer who lands in Canada and establishes tax residency on December 15, 2025 receives the full $7,000 for 2025. On January 1, 2026, another $7,000 is added automatically, giving them $14,000 of total room — identical to someone who arrived on January 2, 2025. The month of arrival is irrelevant.

This rule works in your favour, but it also creates a planning gap. Newcomers who arrive late in the year sometimes assume they receive a partial year’s room and delay opening an account until January. That delay costs nothing in contribution room (the full year’s room is already locked in), but it does cost time in the market. Opening a Wealthsimple TFSA early — even with a small deposit — lets your money start compounding tax-free immediately.

What Happens If You Over-Contribute?

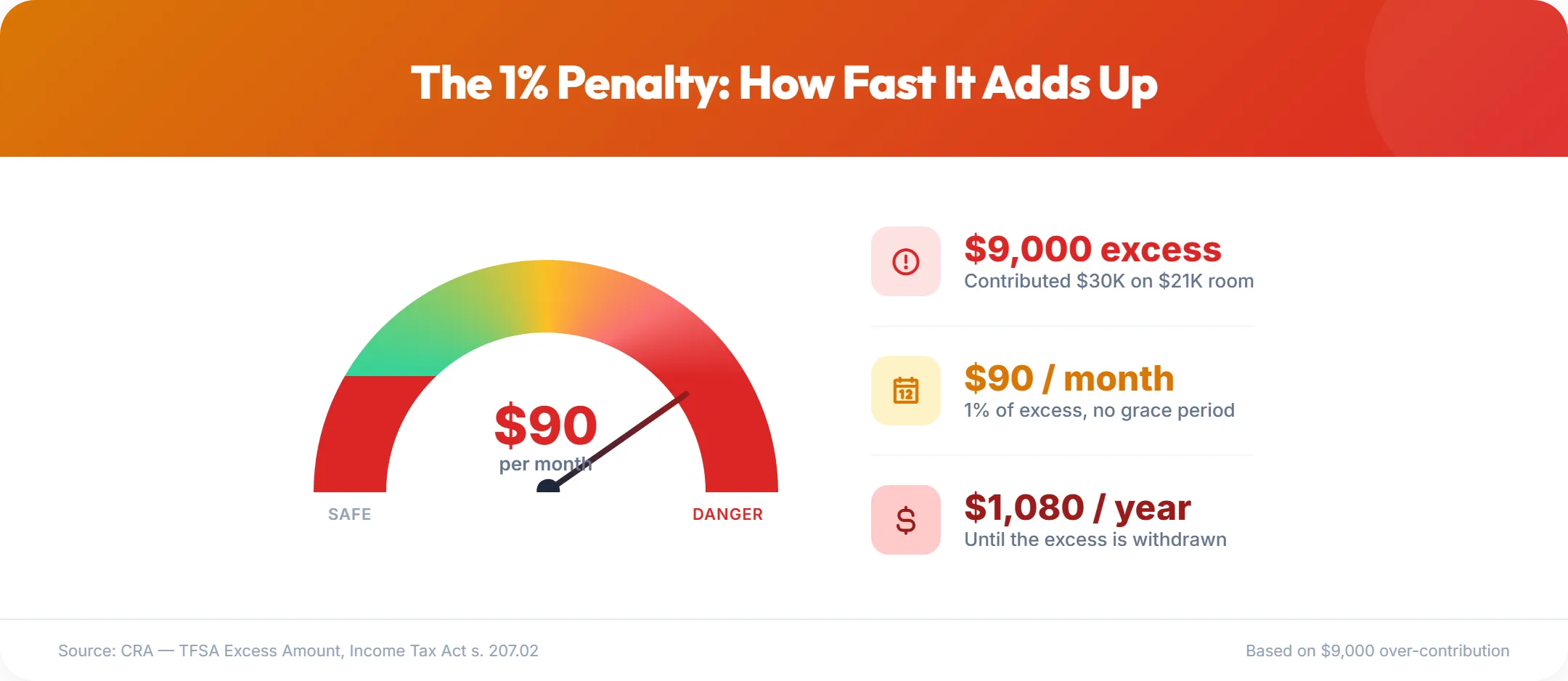

The CRA charges a 1% monthly penalty on the highest excess TFSA amount in each month, with no grace period and no advance warning before the penalty starts accruing.4

Over-contribution is the single most expensive TFSA mistake newcomers make.

Markus Muhs, Senior Portfolio Manager at CG Wealth Management in Edmonton, told Investment Executive:

“I bet there’s a lot of people with self-directed TFSAs [and] no adviser to stop them from overcontributing. If they didn’t look a little bit deeper [to track their TFSA contribution room], they probably put themselves in a bad position.”5

The typical scenario: a newcomer arrives in 2024, reads a “$109,000 TFSA limit” headline, and contributes $30,000 to their account. Their actual room is $21,000. The $9,000 excess generates $90 per month in penalties — $1,080 per year — until the excess amount is withdrawn.

The CRA does not flag over-contributions in real time. The CRA assesses penalties on your annual tax return or through a subsequent notice of assessment, sometimes months after the deposit. By the time you receive the notice, penalties may have compounded across several months.

How to check your actual room

Log into My Account on the CRA website to see your official TFSA contribution room. The number updates after your tax return is processed for each year.

One catch for recent newcomers: the CRA portal sometimes displays incorrect TFSA room. The system may show $0 before your first return is processed, or worse, it may default to the full $109,000 lifetime limit — as if you had been a resident since 2009. Do not trust the CRA My Account number in your first few years. Calculate your actual room manually using the arrival-year table above and contribute based on that figure, not the portal display.

If you discover an over-contribution, withdraw the excess as quickly as possible. Each month it remains in the account adds another 1% charge. The penalty stops accruing once the excess is fully removed. You recover that contribution room on January 1 of the following year.

If the over-contribution was an honest mistake — common for newcomers who misunderstood the residency-based room rules — you can file Form RC4288 (Request for Taxpayer Relief) asking the CRA to waive the penalty under section 207.06 of the Income Tax Act. Explain that the excess arose from a reasonable error and show that you have already withdrawn it. Processing currently takes 6 to 12 months, so pay the penalty upfront to stop interest from compounding while your request sits in the queue — the CRA will refund the amount if the waiver is approved.

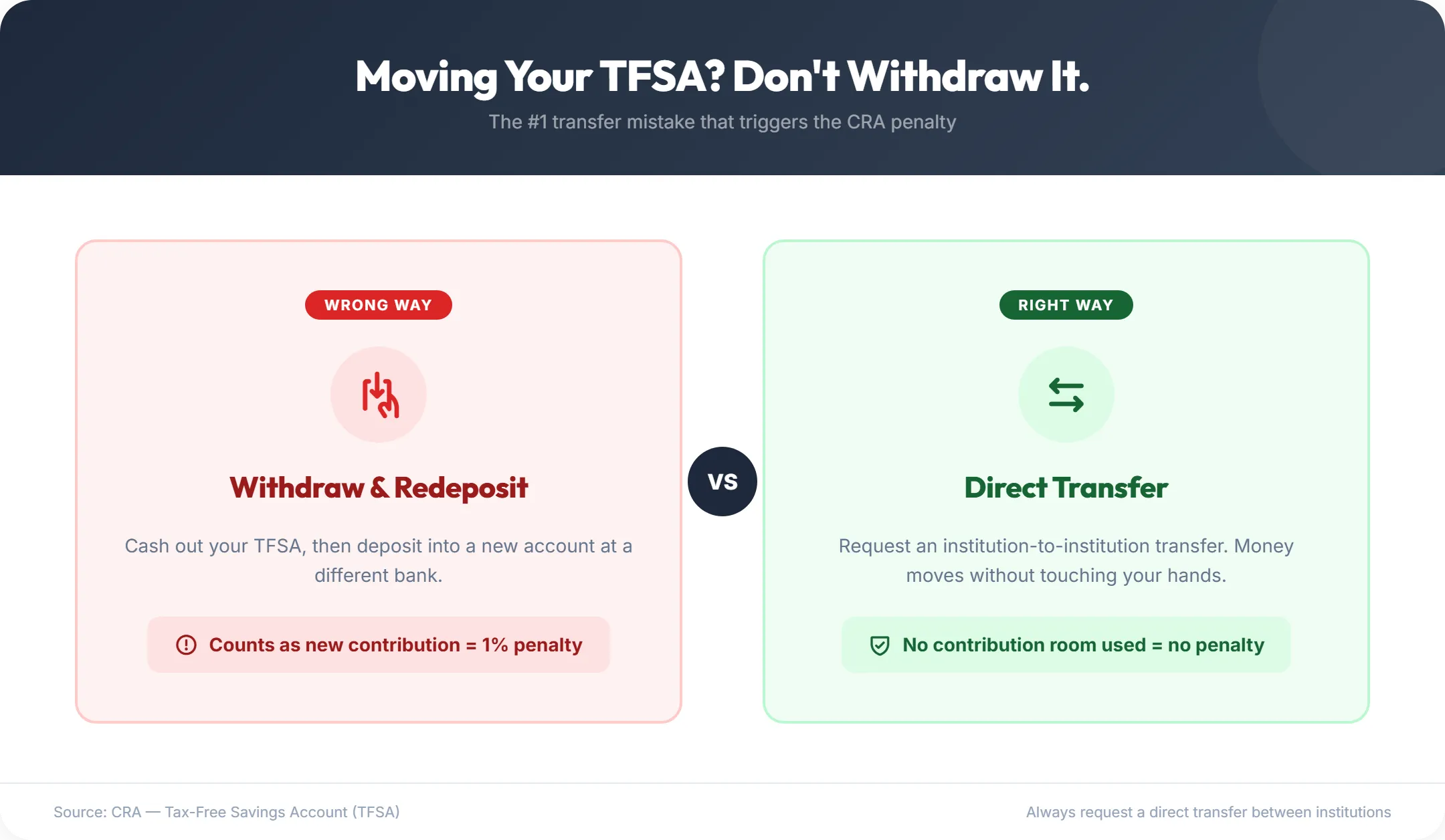

One more trap to avoid: if you want to move your TFSA from one institution to another, do not withdraw the cash and redeposit it yourself. That counts as a new contribution and will trigger the 1% penalty if you have no remaining room. Always request a direct institution-to-institution transfer instead.

Can You Open a TFSA with a SIN Starting with 9?

Yes, temporary residents with a Social Insurance Number starting with 9 can open and fund a Wealthsimple TFSA, provided the CRA considers them a Canadian tax resident.3

Service Canada issues a SIN starting with 9 to temporary residents — work permit holders, study permit holders, and refugee claimants. The SIN itself is not the eligibility test for a TFSA. What matters is whether the CRA classifies you as a tax resident based on your residential ties and physical presence in Canada.

Common scenarios where a temporary SIN holder qualifies:

- Work permit holders with a Canadian address and full-time employment — typically considered tax residents from the date of arrival

- International students who spend the majority of the year in Canada with strong residential ties (lease, bank account, provincial health coverage)

- Spouses of work permit holders who have established their own residential ties in Canada

Wealthsimple’s account opening process accepts SINs starting with 9. You do not need permanent residency or citizenship to open an account. The platform verifies your identity through your SIN and a government-issued photo ID — the same process as any other Canadian applicant. Because newcomers typically have thin Canadian credit files, the automated identity check occasionally flags the application. If this happens, the onboarding team will email you requesting a utility bill or signed lease to manually verify your address.

One important distinction: if your temporary status expires and you leave Canada permanently, you become a non-resident for tax purposes. Non-residents can keep their Wealthsimple TFSA open and investments continue to grow tax-free from Canada’s perspective, but your new country of residence may not recognize the TFSA’s tax-sheltered status and could tax your dividends and capital gains. Any new contributions made while you are a non-resident will trigger the 1% monthly penalty.1 Stop contributing before you sever your residential ties.

If you stay in Canada but your work permit expires before renewal, your temporary SIN also expires. Federal regulations require brokerages to restrict your account on the expiry date — Wealthsimple will not force you to liquidate your investments, but you cannot make new deposits or trades until you provide your renewed permit and updated SIN to their support team. Renew your permit before the expiry date to avoid any interruption.

How Do You Open Your First TFSA on Wealthsimple?

Opening a Wealthsimple TFSA takes under 5 minutes and requires no minimum deposit and no branch visit — two barriers that commonly block newcomers at traditional banks.

Wealthsimple is one of the most accessible platforms for new residents because the account has zero minimum balance requirements, zero administration fees, and $0 trading commissions on Canadian and US stocks and ETFs — including crypto ETFs like BTCC and FBTC. The Wealthsimple platform supports both self-directed investing (you pick the stocks and ETFs) and managed portfolios (Wealthsimple invests for you based on your risk tolerance).

Steps to open

- Download the Wealthsimple app or go to wealthsimple.com

- Enter your personal information, SIN, and upload a government-issued photo ID

- Select “TFSA” as your account type

- Fund the account through Interac e-Transfer, bill payment, or by linking your Canadian bank account

- Start investing — or hold cash in the account while you research your options

If you are choosing between Wealthsimple’s Core (free), Premium (for accounts over $100K), and Generation ($500K+) tiers, the Core plan covers everything a newcomer needs with zero fees on stock and ETF trades. Our tier comparison breaks down where Premium adds value — primarily the 0% foreign exchange fee on US stocks.

Wealthsimple is registered with the OSC and member of CIPF, which protects your account up to $1 million if the firm becomes insolvent — the same coverage as any Big Five bank brokerage.

New accounts opened through a Wealthsimple referral code qualify for a cash bonus on your first deposit. The current Wealthsimple promotions include a $25 bonus on a $100 minimum deposit, which is a useful head start for newcomers funding their first TFSA. One caveat: if you contribute your exact annual limit and then receive a promotional bonus deposited into your TFSA, the bonus pushes you into an over-contribution. Leave a small buffer in your room if you are expecting a promotional payout.

For newcomers also considering homeownership, the FHSA (First Home Savings Account) may deserve priority. The FHSA offers tax-deductible contributions plus tax-free withdrawals for a qualifying home purchase — a double tax advantage the TFSA cannot match. Newcomers with temporary residency, a spouse who owns property, or other complex situations should check the FHSA eligibility edge cases — the CRA’s definition of “first-time buyer” is more forgiving than most expect. Our TFSA vs RRSP vs FHSA comparison walks through exactly which account to open first based on your income, tax bracket, and homebuying timeline.

Sources

Footnotes

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.