Transfer Your TFSA to Wealthsimple (2026): Bank Fees, Timelines & How to Get Reimbursed

The entire transfer starts from the Wealthsimple app — no branch visits required. Bank-by-bank processing times, fee amounts, and the quirks that cause delays.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: Banks charge $135-$150 to transfer your TFSA out, and the process takes 2-5 weeks. Wealthsimple reimburses that fee on incoming transfers of $25,000+. The entire transfer is initiated from the Wealthsimple app — no branch visits required.

- TD, RBC, BMO, and Disnat charge $150; CIBC charges $135

- Desjardins is the slowest at 4-5 weeks due to paper-based processing

- Reimbursement deposits within 2 business days of transfer completion

- New to Wealthsimple? $25 bonus on top of the fee reimbursement — Sign Up with Code 9C6DMQ

This guide maps the exact transfer-out fee, processing timeline, and operational pain points at TD, RBC, BMO, CIBC, Scotia, and Desjardins Disnat — then walks through the step-by-step process for initiating the move entirely from the Wealthsimple app.

Desjardins takes 4-5 weeks to process a transfer — the slowest of any major institution, due to paper-based processing.

How much does your bank charge to transfer a TFSA?

Canadian banks charge a flat administrative fee of $135 to $150 every time you transfer a registered account to another institution — regardless of your account balance, how long you have been a client, or whether you have ever paid a cent in commissions.1 Your departing bank deducts the fee from your balance before releasing the funds, meaning the amount that arrives at Wealthsimple is reduced by the penalty.

In 2025, Wealthsimple estimated that Canadian investors collectively paid over $30 million in transfer-out charges and filed a formal request with the federal government to review rising transfer fees. As Jessica Oliver, Head of Government and Regulatory Relations at Wealthsimple, told Reuters, “If the government were to take action, it would make it easier for clients to overcome that friction.”2

| Bank | Transfer-Out Fee | Low-Balance Annual Fees You Stop Paying |

|---|---|---|

| TD Direct Investing | $150 | $100/yr if under $15,000 |

| RBC Direct Investing | $150 | $100/yr if under $15,000 |

| BMO InvestorLine | $150 | $100/yr if under $25,000 |

| CIBC Investor’s Edge | $135 | $0 (annual fee waived for TFSAs) |

| Scotia iTRADE | $150 | $0 (LAAA fee waived for registered accounts) |

| Desjardins Disnat | $150 | $120/yr if under $15,000 and fewer than 6 trades |

The transfer-out fee is identical whether you are moving $5,000 or $500,000. It is a flat exit penalty designed to exploit the sunk-cost fallacy — and it works. Many investors pay $100 to $150 in annual maintenance fees year after year rather than absorb a one-time $135-$150 transfer fee that would eliminate those recurring costs permanently.

Beyond the transfer fee itself, three additional costs can surface at the departing institution:

- Deferred Sales Charges (DSCs): If your TFSA holds mutual funds with a back-end load schedule, selling early triggers penalties — typically 5-6% in year one, declining annually

- Trading commissions on liquidation: If your bank must sell holdings before transferring cash, you pay $6.95-$9.99 per position at the standard commission rate

- Low-load mutual fund fees: Some funds carry early redemption charges separate from DSCs, usually 2-3% within the first three years

Wealthsimple explicitly excludes these extra costs from its reimbursement policy — only the administrative transfer-out fee is reimbursed.

Does Wealthsimple reimburse TFSA transfer fees?

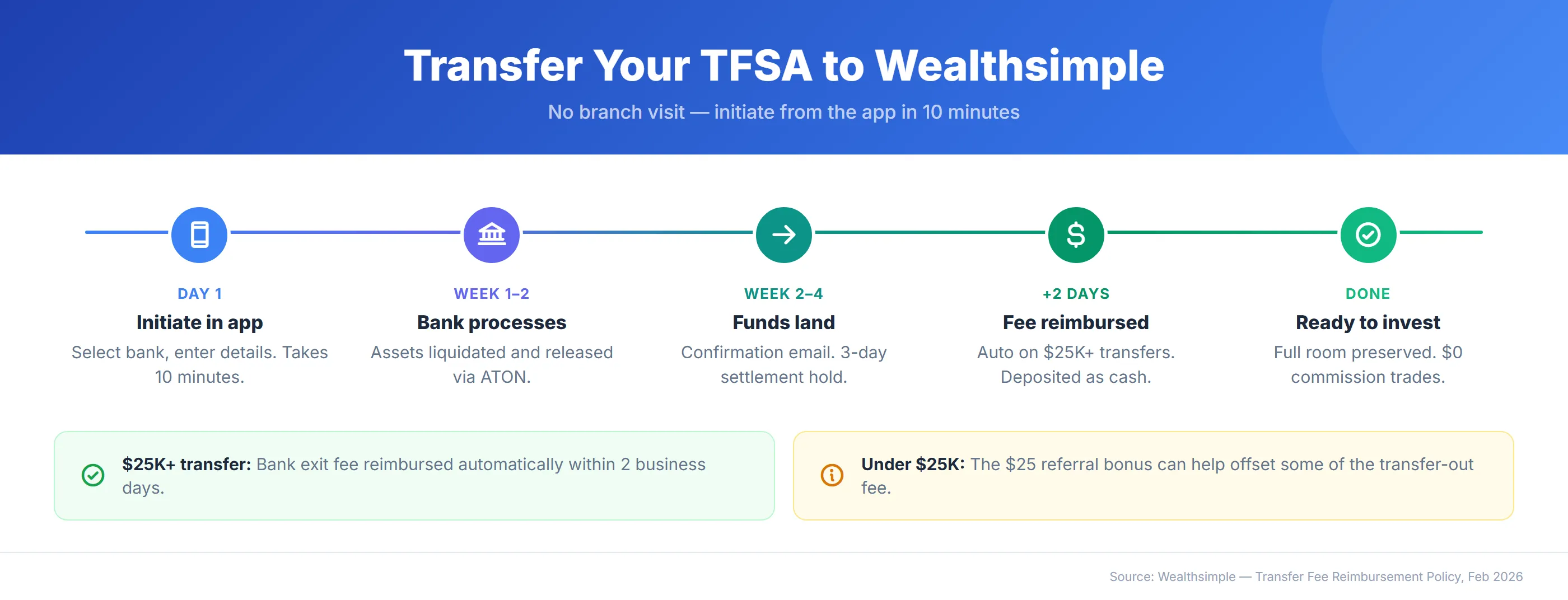

Wealthsimple automatically reimburses the transfer-out fee charged by your previous institution when the total transfer amount is $25,000 or more.3 No receipt submission, no support ticket, no paperwork — the system detects the incoming institutional transfer amount and processes the reimbursement without manual intervention.

As Jessica Oliver, Wealthsimple’s Head of Government and Regulatory Relations, told BNN Bloomberg, “Canadians should be in control of their money. They should have the autonomy to move their money where they want.”4

Current policy details (February 2026):

- Minimum transfer amount: $25,000 (increased from $15,000 on April 10, 2025)

- Reimbursement timeline: Deposited into your Wealthsimple cash balance within 2 business days of the transfer completing

- 90-day retention clause: Transferred funds must remain in Wealthsimple for at least 90 days, or the reimbursement may be clawed back

- TFSA contribution room: The reimbursement does not count against your contribution room — it is classified as an administrative fee offset, not a deposit

- What is covered: The administrative transfer-out fee only — DSCs, low-load mutual fund fees, and trading commissions during liquidation are excluded

The reimbursement policy applies to TFSA, Wealthsimple RRSP, Wealthsimple FHSA, and other registered account transfers. If you are transferring multiple registered accounts simultaneously — for example, a TFSA and an RRSP — each account must independently meet the $25,000 minimum to qualify for its own reimbursement.

What is the transfer timeline at each major bank?

The standard timeline to transfer a TFSA from a major Canadian bank is 2 to 4 weeks through the ATON (Automated Transfer Online Notification) system, though specific institutions vary. You initiate the transfer from the Wealthsimple side; the departing bank receives the ATON request and processes the release. You do not need to call your bank, visit a branch, or sign paperwork at the departing institution.

Most institutional TFSA transfers complete within 2-4 weeks. Desjardins is the consistent outlier at 4-5 weeks due to paper-based internal processes.

TD Direct Investing

Transfer-out fee: $150 | Typical timeline: 2-3 weeks

TD processes ATON transfers relatively smoothly, but one friction point catches account holders off guard: you cannot walk into a TD branch and request a TFSA transfer. The ATON process must be initiated by the receiving institution (Wealthsimple). Attempting to withdraw the TFSA manually at a branch is treated as a regular withdrawal — which costs you contribution room until the following January 1 and may trigger the 1% monthly overcontribution penalty if you redeposit in the same calendar year without available room.

If your TD TFSA holds proprietary TD e-Series mutual funds, those positions will be liquidated to cash before the transfer processes (TD does not charge a commission to sell mutual funds). Standard ETFs and individual stocks can transfer in-kind if available on the Wealthsimple platform.

TD also charges a $25 quarterly admin fee ($100/year) on accounts with a household balance under $15,000. Transferring out eliminates this recurring drag immediately.

RBC Direct Investing

Transfer-out fee: $150 | Typical timeline: 2-4 weeks

RBC follows the standard ATON process, but the main delay is internal: RBC’s back-office team appears to review each outbound registered transfer before releasing funds — account holders report this step can add 3-5 business days to the standard processing window, with little communication during the wait — the transfer appears stalled on the Wealthsimple tracker until RBC completes its internal review.

RBC Series A and Series D mutual funds are proprietary and unavailable outside the RBC ecosystem. These positions will be liquidated before the cash transfers (RBC does not charge a commission for mutual fund sell orders). If your RBC TFSA holds broadly available ETFs (iShares, Vanguard, BMO ETFs), those can transfer in-kind without liquidation.

The $25 quarterly admin fee ($100/year) applies to RBC accounts with an aggregate balance under $15,000. Transferring eliminates the fee and the $9.95 commission on every future trade.

BMO InvestorLine

Transfer-out fee: $150 | Typical timeline: 2-4 weeks

BMO InvestorLine is the most punitive institution for small TFSA accounts. The $100 annual admin fee applies to any registered account holding less than $25,000 — a threshold significantly higher than the $10,000-$15,000 range at other banks. An investor with a $10,000 TFSA at BMO is losing 1% per year in administrative fees alone before placing a single trade. Combined with the $9.95 per-trade commission, BMO’s cost structure is the most expensive in this comparison for passive investors building wealth from a small starting balance.

BMO transfers process through ATON without unusual complications. The most common complaint is delayed confirmation emails — the transfer may have fully settled on Wealthsimple’s end before BMO sends its notification that the account has been closed.

CIBC Investor’s Edge

Transfer-out fee: $135 | Typical timeline: 2-3 weeks

CIBC Investor’s Edge charges a $135 transfer-out fee — slightly lower than the $150 charged by TD, RBC, BMO, Scotia, and Disnat. However, CIBC does not charge an annual administration fee on TFSA accounts regardless of balance, making it friendlier to small accounts than TD, RBC, or BMO.

CIBC’s ATON processing is among the fastest, typically completing within 2-3 weeks. One quirk to watch: CIBC Investor’s Edge accounts holding GICs cannot transfer those positions until the GIC matures. The GIC must either be broken with applicable penalties or left behind until maturity, at which point you can initiate a second transfer for the remaining balance.

CIBC charges $6.95 per trade — the lowest commission among the big banks, but still $6.95 more than the $0 you pay on every Wealthsimple TFSA trade.

Scotia iTRADE

Transfer-out fee: $150 | Typical timeline: 2-4 weeks

Scotia iTRADE charges the standard $150 transfer-out fee. A separate $125 deregistration fee also exists, but it applies only if you are collapsing the registered account entirely without transferring to another registered account. For a standard ATON transfer to Wealthsimple, you pay the $150 transfer fee — not the deregistration fee.

Scotia’s Low Activity Account Administration (LAAA) fee — $25 per quarter on small non-registered accounts — does not apply to TFSAs. Scotia explicitly waives the LAAA fee for all registered plan accounts (RRSP, TFSA, RESP, LIRA, LIF, RIF).5 The main ongoing cost for passive TFSA investors at Scotia is the $9.99 per trade commission whenever they do invest.

Scotia iTRADE also offers “Active Trader” pricing at $4.99 per trade, but it requires 150+ trades per quarter to qualify. That trading velocity is antithetical to the long-term, low-frequency strategy that makes a TFSA most powerful.

Desjardins Disnat

Transfer-out fee: $150 | Typical timeline: 4-5 weeks

Desjardins Disnat is the slowest institution for TFSA transfers in Canada. While every other major bank processes through ATON within 2-4 weeks, Disnat consistently takes 4 to 5 weeks — and sometimes longer. The delays stem from paper-based internal processes: Disnat may request physical signatures and mailed account statements before releasing funds, adding 1-2 weeks on top of the standard ATON timeline.

Disnat’s fee structure presents a unique paradox. The platform charges $0 commissions on online equity and ETF trades — matching Wealthsimple on that front. But Disnat claws back the savings through a $30 quarterly inactivity fee ($120/year) on accounts with an aggregate balance under $15,000 and fewer than 6 trades per year. Holding a CELI or FHSA does not exempt you from this penalty — only holding an RRSP or RRIF, or being between 18 and 30 years old, qualifies for a waiver.

A 35-year-old passive investor with $10,000 in a Disnat CELI pays $120 per year in inactivity fees despite $0 commissions. The same investor at Wealthsimple pays $0 in commissions and $0 in account fees — with no inactivity penalty regardless of trading frequency or balance.

What if your TFSA balance is under $25,000?

If your TFSA falls below the $25,000 reimbursement threshold, Wealthsimple does not automatically cover your bank’s transfer-out fee. Signing up through a Wealthsimple referral link earns you a $25 cash bonus on your first deposit — a small offset, but the real savings come from what you stop paying at your old bank.

The math for a $15,000 TFSA transfer:

Your bank charges $150 to transfer out. The $25 referral bonus reduces the net cost to $125. But at TD, RBC, or BMO, you are paying $100 per year in low-balance admin fees on that same account. The transfer pays for itself within 15 months — and you save $100 every year after that, permanently.

The math for a $5,000 TFSA transfer:

Your bank charges $150 to transfer out. The $25 referral bonus brings the net cost to $125. At Desjardins Disnat, a passive investor with that balance pays $120 per year in inactivity fees. You break even within 13 months and eliminate the recurring drain permanently. If you are weighing whether to transfer to Wealthsimple or another discount brokerage like Questrade, see our Wealthsimple vs Questrade comparison for the full fee breakdown.

How do you start a TFSA transfer to Wealthsimple?

The entire TFSA transfer is initiated from the Wealthsimple app or website — you do not need to contact your current bank, visit a branch, or sign paperwork at the departing institution.

The entire transfer initiates from the Wealthsimple app — no branch visit, no phone call to your old bank required.

Step 1: Open the Wealthsimple app and tap Move (or navigate to Transfers on the desktop site)

Step 2: Select Transfer from another institution and choose TFSA as the account type

Step 3: Search for your current bank from the list — TD, RBC, BMO, CIBC, Scotia, Desjardins, and dozens of smaller institutions are all available

Step 4: Enter your brokerage account number at the departing institution (this is your investment account number, not your day-to-day banking number)

Step 5: Choose between a full transfer (move everything) or partial transfer (move a specific dollar amount or specific holdings only)

Step 6: Select whether to transfer in-kind (keep your existing stocks and ETFs) or in-cash (your departing bank liquidates everything to cash before sending). In-kind transfers keep your positions intact — you avoid selling at a bad price and skip the $6.95-$9.99 per-trade liquidation commissions at your old bank. Your departing bank will automatically liquidate proprietary mutual funds to cash regardless, since Wealthsimple’s platform cannot hold them. Fractional shares cannot transfer in-kind — brokerages hold them in trust, not as actual share ownership — so sell any fractions before initiating the transfer to avoid a rejection. If any of your holdings are incompatible with Wealthsimple’s platform, an in-kind transfer can stall for 30 days or more while the institutions fail to communicate about the mismatch — choosing in-cash avoids this risk entirely

Step 7: Review the details and submit — Wealthsimple sends the ATON request to the departing institution automatically from this point

You can track the transfer status in your Wealthsimple app under Activity — it updates as the ATON request progresses through each stage.

Three things to watch during the transfer window:

- Do not close your old account before the transfer completes — the ATON system needs the account open to pull the funds. Your bank will close the account automatically once the balance hits zero. If a scheduled dividend pays into your old account after the transfer completes, the departing institution typically sweeps those residual funds to Wealthsimple within 10-15 business days.

- Do not contribute to your old TFSA during the transfer period — overlapping contributions reported by two institutions can create the appearance of an overcontribution to the CRA.

- Verify your exact contribution room on CRA My Account before initiating — especially if you made withdrawals in previous years, since withdrawn amounts only restore as room the following January 1.

For a full breakdown of Wealthsimple TFSA fees, contribution limits, and the 7-bank fee battle card, see the Wealthsimple TFSA Guide 2026. If you are reorganizing finances across multiple account types, see TFSA vs RRSP vs FHSA: Which First? for the account prioritization framework.

Sources

Footnotes

Transfer-out fees based on published fee schedules from TD Direct Investing, RBC Direct Investing, BMO InvestorLine, CIBC Investor’s Edge, Scotia iTRADE, and Desjardins Disnat as of February 2026. ↩

Reuters — Wealthsimple asks Canada to review rising bank transfer fees ↩

BNN Bloomberg — Wealthsimple pushes feds to regulate transfer fees for Canadian investors ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.