Wealthsimple TFSA 2026: $0 Fees vs. Big Bank Hidden Costs

A fee-by-fee breakdown of every major Canadian bank — including the 20-year compounding math that shows what 'small' annual fees really cost your TFSA.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

Over 20 years, the gap between $0 and $9.99 per trade compounds into more than $26,000 of lost growth.

The Bottom Line: Wealthsimple charges $0 commissions, $0 account fees, and $0 to transfer out — while the Big Five bank brokerages charge $6.95-$9.99 per trade plus $100-$150/yr in maintenance fees on smaller accounts. The 2026 TFSA limit is $7,000 ($109,000 cumulative since 2009).

- $0 across the board vs. TD, RBC, BMO, CIBC, Scotia — and Disnat’s $120/yr inactivity trap

- Hidden bank fees compound into $26,000+ in lost growth over 20 years

- Transfer fee reimbursement on incoming balances of $25,000+

This guide breaks down exactly what Wealthsimple charges versus six major banks, quantifies the hidden cost of staying at a legacy institution, and walks through the opening and transfer process step by step.

What is the TFSA and how much room do you have in 2026?

The Tax-Free Savings Account contribution limit for 2026 is $7,000 per year, and all investment gains inside — capital gains, dividends, and interest — grow permanently tax-free.1 Unlike a Wealthsimple RRSP where withdrawals are taxed as income, TFSA withdrawals are never taxed regardless of how large the balance has grown. Withdrawn amounts restore as contribution room the following January 1, giving the TFSA a flexibility that no other Canadian registered account offers.

Aaron Hector, Senior Wealth Advisor and Founding Partner at TIER Wealth in Calgary, told Investment Executive:

“If a client is on the fence about the RRSP vs. TFSA decision, I would usually err to using the [TFSA], because it’s just so flexible. It’s really easy to take money out of a TFSA a year or two down the road and move it into the RRSP. Going the other direction just does not work.”2

The federal government sets the annual TFSA limit each year based on inflation indexing. Both 2025 and 2026 hold steady at $7,000. The cumulative room since the TFSA launched in 2009 now totals $109,000 for anyone who has been eligible since the beginning:

| Year Range | Annual Limit | Cumulative Total |

|---|---|---|

| 2009-2012 | $5,000 | $20,000 |

| 2013-2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016-2018 | $5,500 | $57,500 |

| 2019-2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024-2026 | $7,000 | $109,000 |

TFSA contribution room accumulates automatically for every Canadian tax resident aged 18 or older with a valid Social Insurance Number. If you turned 18 in 2020, your cumulative room in 2026 is $45,500 — not the full $109,000. Unused room carries forward indefinitely and never expires. If you arrived in Canada recently, your room calculation starts from your first year of tax residency — see our TFSA newcomers guide for the arrival-year table and common traps.

The TFSA also pairs well with other registered accounts. If you are saving for a first home, the Wealthsimple FHSA offers tax-deductible contributions on top of the TFSA’s tax-free growth — and both can be held on the same Wealthsimple account.

How do Wealthsimple TFSA fees compare to the big banks?

Wealthsimple’s self-directed TFSA charges $0 commissions on every stock and ETF trade, $0 in annual maintenance fees, and $0 in transfer-out fees.3 The Big Five bank brokerages — TD, RBC, BMO, CIBC, and Scotia — charge between $6.95 and $9.99 per trade, plus annual or quarterly fees that hit smaller accounts hardest:4

TD Direct Investing and RBC Direct Investing both waive the $25 quarterly fee only if the client’s aggregate household balance exceeds $15,000 — or with a pre-authorized contribution plan at RBC, or 3+ trades per quarter at TD. BMO InvestorLine sets a higher bar: the $100 annual fee kicks in on any registered portfolio under $25,000. Scotia iTRADE’s Low Activity Account Administration fee ($25/quarter) applies below $10,000 unless the investor makes at least one trade every three months.

Desjardins Disnat deserves a closer look because it appears competitive at $0 commissions. The catch is the $30 quarterly inactivity fee ($120/year) that applies when the aggregate balance is under $15,000 and fewer than six trades are executed per year.4 Holding a CELI or FHSA alone does not waive this fee — only holding an RRSP or RRIF, or being aged 18-30, exempts the account. A passive investor with $10,000 in a Disnat CELI pays $120/year in inactivity fees while executing the exact same strategy that costs $0 on Wealthsimple.

How much are bank TFSA fees really costing you?

Bank TFSA fees cost up to $120 per year in maintenance charges alone — and that is before the $6.95-$9.99 per-trade commissions that compound as lost tax-free growth over decades. Two costs do the most damage to long-term returns: maintenance fees on smaller accounts and commissions on regular contributions.

Cameron Smith, Wealth Advisor at Investment Planning Counsel, told Yahoo Finance Canada:

“The number one determinant of long-term returns really is the amount of fees you charge. So, a mutual fund that is charging 1 or 1.15 per cent per year versus an ETF that’s 0.2 per cent, that’s a big amount of money.”5

The maintenance fee drag:

A new investor contributing $4,000 to a TD Direct Investing TFSA falls below the $15,000 household waiver threshold. That triggers the $25 quarterly maintenance fee — $100 per year, or 2.5% of the entire portfolio. In an environment where broad-market dividend ETFs yield 2-3%, the maintenance fee alone wipes out an entire year of passive income before a single trade is placed.

BMO InvestorLine is steeper: the $100 annual fee applies to any registered account under $25,000. A beginning investor with $7,000 (one year’s maximum TFSA contribution) loses 1.4% of their portfolio annually just for having the account open — on top of the $9.95 commission charged on every purchase.

The commission drag on dollar-cost averaging:

If you contribute $250 bi-weekly and buy a broad-market ETF each time, you pay $9.99 per trade at TD Direct Investing or Scotia iTRADE. That is a 4% immediate loss on every $250 contribution. Over a full year, 26 trades at $9.99 each means $260 in commissions on $6,500 of contributions.

The real damage is not the $260 — it is the compounding those lost contributions would have generated inside the tax-free shelter. Over a 20-year horizon at a 7% average annual return, $260 per year in lost contributions compounds to over $10,600 in forgone tax-free wealth. For a 25-year-old investor with a 40-year time horizon, the figure approaches $52,000.

On Wealthsimple, the identical strategy costs exactly $0 in commissions and $0 in maintenance fees. The only structural cost is the 1.5% currency conversion fee on US-listed securities, which does not apply to Canadian ETFs like XEQT, VGRO, or VEQT — the most popular choices for Canadian TFSA investors.

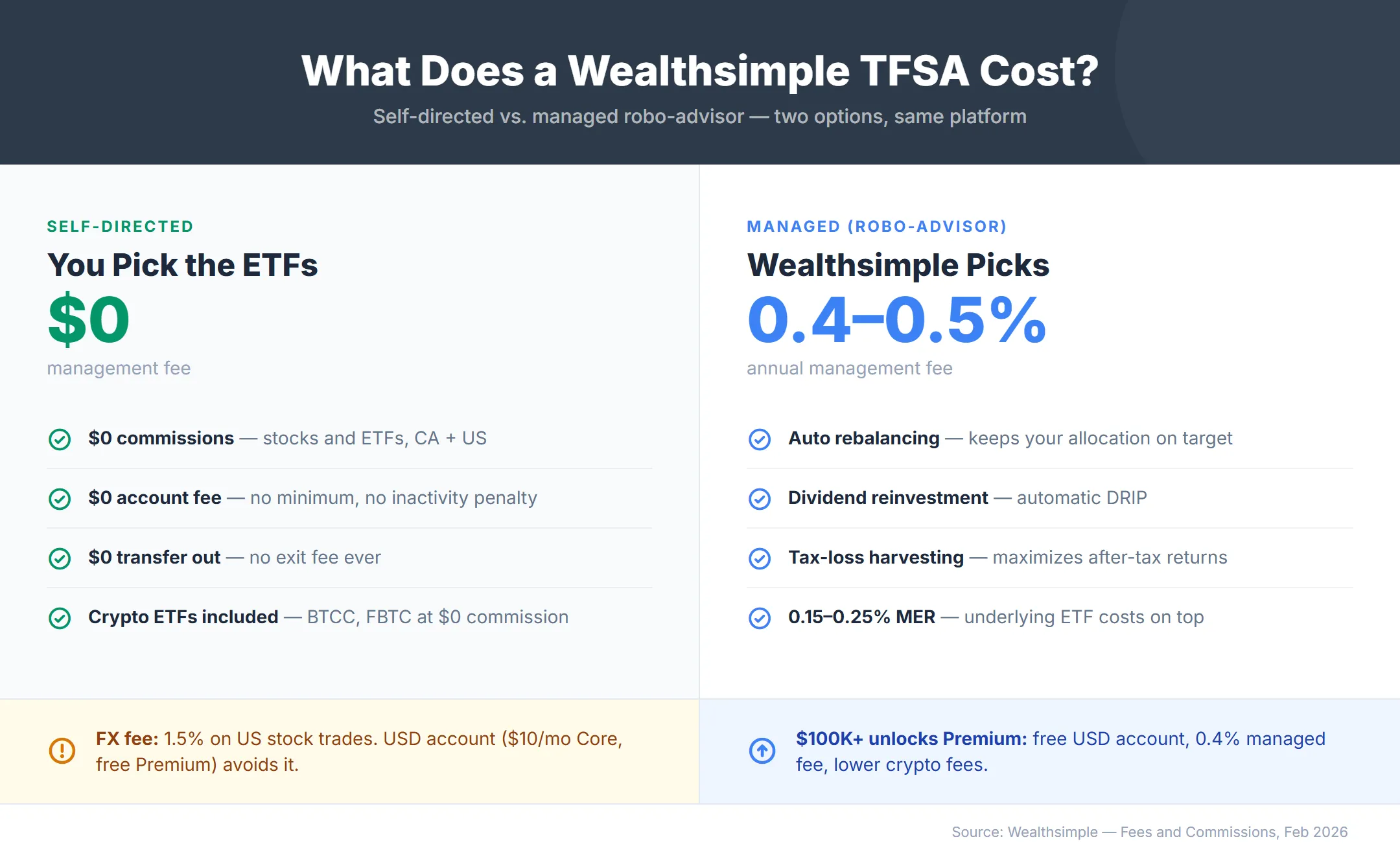

What does Wealthsimple charge for a TFSA?

The self-directed Wealthsimple TFSA charges $0 in management fees, while the managed robo-advisor option charges a 0.4% to 0.5% annual fee depending on your tier.3

Self-directed TFSA:

- $0 commission on all Canadian and US stocks and ETFs

- $0 account maintenance fee — no minimum balance, no inactivity penalty

- $0 transfer-out fee

- 1.5% currency conversion fee on US stock trades (applies across all tiers)

- $10/month USD account to hold US dollars and avoid per-trade FX conversion (free on Premium)

Managed TFSA (robo-advisor):

- 0.5% annual management fee (Core tier, under $100K)

- 0.4% annual management fee (Premium tier, $100K+)

- Automatic rebalancing, dividend reinvestment, and tax-loss harvesting included

- Underlying ETF MERs of approximately 0.15-0.25% apply on top of the management fee

For most TFSA investors buying Canadian-listed ETFs, the total cost on the self-directed Wealthsimple TFSA is effectively $0. This includes crypto ETFs like BTCC and FBTC, which trade on the TSX in Canadian dollars and carry no currency conversion or commission charges. The FX fee only applies when you trade US-listed securities. If you regularly buy US stocks like Apple or the S&P 500 (VOO), the USD account at $10/month eliminates per-trade conversion entirely — and it becomes free once your total Wealthsimple balance across all accounts reaches $100,000 (Premium tier).

How do you open a Wealthsimple TFSA?

Opening a Wealthsimple TFSA takes under 10 minutes with no minimum deposit and no branch visit required. You need a valid Social Insurance Number, a Canadian residential address, and a piece of government-issued photo ID.

Identity verification takes minutes: snap a photo of your ID and a selfie, and Wealthsimple typically approves your TFSA within the same day.

Step-by-step:

- Sign up at Wealthsimple using a referral link to lock in the cash bonus

- Complete identity verification — upload a photo ID and take a selfie, which in our testing was approved within minutes

- Select “TFSA” as your account type, then choose self-directed or managed

- Link your bank account for deposits via Plaid or manual entry

- Fund the account — a deposit of $100 or more qualifies for the referral bonus

Wealthsimple is an IIROC-regulated investment dealer and CIPF member — your TFSA assets are protected up to $1 million per account category if the firm becomes insolvent.

The referral bonus is deposited as cash directly into your account within 14 business days of your first deposit clearing. It does not consume your TFSA contribution room because Wealthsimple classifies it as a promotional credit, not a contribution.

How do you transfer your TFSA to Wealthsimple?

Transferring a TFSA to Wealthsimple takes 2 to 4 weeks via the ATON system and preserves your full contribution room — it does not count as a withdrawal and recontribution.6 You initiate the transfer entirely from the Wealthsimple app; you do not need to call or visit your current bank.

Once initiated from the Wealthsimple app, the ATON transfer from TD typically completes within 2-3 weeks — entirely hands-off.

Key transfer details:

- Transfer-out fee: Every major bank charges $135-$150 to release your TFSA (see the fee battle card above)

- Wealthsimple reimbursement: Automatic on transfers of $25,000 or more (threshold increased from $15,000 on April 10, 2025)6

- Reimbursement timeline: In our testing, deposited automatically within 2 business days of transfer completion

- 90-day retention clause: Transferred funds must remain in Wealthsimple for 90 days or the reimbursement may be clawed back

- Does not affect contribution room: The reimbursement is classified as a fee offset, not a contribution to your TFSA

The reimbursement covers the administrative transfer-out fee only. It does not cover Deferred Sales Charges (DSCs), mutual fund low-load fees, or trading commissions incurred during liquidation at the departing institution.

If your TFSA balance is under $25,000, the transfer fee is not automatically reimbursed — but the $25 referral bonus helps offset it. For transfers of $25,000+, the fee reimbursement stacks with the referral bonus and any active promotions like the transfer match — check the current offers before initiating your transfer.

Processing time varies by institution. Based on our tracking, bank-initiated transfers through the ATON system typically take 2-4 weeks, with Desjardins sometimes stretching to 5 weeks due to paper-based internal processes. The transfer is entirely hands-off once initiated — Wealthsimple handles the communication with the departing institution.

Be prepared for a final settlement delay. Even after you receive the confirmation email that your transfer has landed at Wealthsimple, the funds typically sit as “unavailable” for up to 3 business days before you can actually use them to buy stocks or ETFs.

We cover the full bank-by-bank transfer process — including specific timelines, hold periods, and pain points for TD, RBC, BMO, CIBC, Scotia, and Desjardins — in our dedicated guide to transferring your TFSA to Wealthsimple.

Sources

Footnotes

CRA — Tax-Free Savings Account (TFSA) Guide for Individuals ↩

Investment Executive — No TFSA info in CRA portals? No problem, advisors say ↩

Fee data compiled from published rate schedules at TD Direct Investing, RBC Direct Investing, BMO InvestorLine, CIBC Investor’s Edge, Scotia iTRADE, and Desjardins Disnat as of February 2026. ↩ ↩2

Yahoo Finance Canada — Should you switch from mutual funds to ETFs? Here’s what the experts say ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.