Wealthsimple Core vs Premium vs Generation: Which Tier Saves You the Most?

Premium saves ~$550/year at $100K through fee waivers, better rates, and free tax software. Here is the exact math for every tier — plus what changed in 2026.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: Wealthsimple’s three tiers — Core, Premium ($100K+), and Generation ($500K+) — gate management fees, cash interest, and private-market access. Premium saves roughly $550/year through fee waivers alone;1 Generation drops the management fee to a tiered 0.40%-to-0.20% scale and unlocks private equity, private credit, and the Summit Portfolio.

- Core ($0-$99K): 0.50% management fee, 1.25% Cash interest, 2.0% crypto fee, $10/mo USD account

- Premium ($100K+): 0.40% fee, 1.75% Cash, free USD account, $240 Visa Infinite annual fee waived

- Generation ($500K+): 0.40%→0.20% management fee, 2.25% Cash without direct deposit, private equity at $10K minimum

- Tier set by the higher of net deposits OR portfolio value — a market drop alone can’t downgrade you

- Self-directed Wealthsimple Trade is free at every tier regardless of balance

What Are Wealthsimple’s Three Client Tiers in 2026?

Wealthsimple assigns your tier based on the higher of your net deposits or total portfolio value across all accounts — TFSA, RRSP, non-registered, corporate, chequing, and crypto combined.1

| Feature | Core ($0–$99K) | Premium ($100K+) | Generation ($500K+) |

|---|---|---|---|

| Management Fee | 0.50% | 0.40% | 0.40%–0.20% |

| Cash Interest | 1.25% (1.75% with DD) | 1.75% (2.25% with DD) | 2.25% |

| USD Account | $10/mo | Free | Free |

| Crypto Trading Fee | 2.0% | 1.0% | 0.5% |

| Crypto Staking Cut (WS takes) | 30% | 30% | 15% |

| Options Per-Contract | $0 | $0 | $0 |

| Tax Software | Basic (pay what you want) | Plus ($40 value) | Pro ($80 value) |

| Priority Support | Standard | Priority | Highest priority |

| Visa Infinite Fee | $240/yr (waivable with DD) | Waived | Waived |

| Milestone Rewards | None | From $200K | From $200K |

| Private Markets | Not available | Not available | Available |

The net deposits rule provides a critical safety net: if you deposit $100,000 and a market crash drops your portfolio to $85,000, you keep Premium status because your net deposits still meet the threshold. Downgrades only trigger when both net deposits and market value fall below the line — and only when withdrawals (not market drops) push both metrics under the threshold. Our Wealthsimple Generation review walks through the dedicated-advisor onboarding, household expansion exception, and the Big Five wealth-manager fee comparison in full.

For a deep dive on the interest rate column, including how Wealthsimple compares to EQ Bank and Big Five savings accounts, see our Wealthsimple Cash Account review.

What Does Wealthsimple Charge for Managed Investing in 2026?

Wealthsimple’s managed investing fee (the robo-advisor product) is 0.50% for Core, 0.40% for Premium, and a tiered scale at Generation that runs from 0.40% at the $500K threshold down to 0.20% for clients with $10,000,000 or more in managed assets.1 Wealthsimple does not publicly disclose the intermediate breakpoints, so the marketed “as low as 0.20%” floor applies only at the upper end of that scale.

These fees are charged on top of the underlying ETF Management Expense Ratios (MERs), which add roughly 0.12%–0.15% for the Classic portfolio and 0.21%–0.23% for the SRI portfolio.2

| Tier | Management Fee | + ETF MER (Classic) | All-In Cost | Annual Cost |

|---|---|---|---|---|

| Core | 0.50% | ~0.15% | ~0.65% | ~$650 (on $100K) |

| Premium | 0.40% | ~0.15% | ~0.55% | ~$550 (on $100K) |

| Generation | 0.40%–0.20% | ~0.15% | ~0.55%–0.35% | ~$2,750 (on $500K minimum) |

A common misconception: crossing from Premium to Generation does not reduce your managed investing fee at all. Both tiers pay 0.40% at their entry thresholds. The Generation fee only compresses at much higher balances.

How does Wealthsimple compare to other robo-advisors? At the $100,000 Premium threshold:

| Platform | Management Fee | All-In Cost (est.) |

|---|---|---|

| Wealthsimple (Premium) | 0.40% | ~0.55% |

| Questwealth Portfolios | 0.20% | ~0.39% |

| Nest Wealth | $40/mo (0.48% effective) | ~0.63% |

| BMO SmartFolio | 0.70% | ~0.90% |

| RBC InvestEase | 0.50% | ~0.70% |

Questwealth is the cheapest robo-advisor at $100K, undercutting Wealthsimple Premium by roughly 0.16% — about $160 per year. But Questwealth lacks Wealthsimple’s ecosystem: no integrated chequing account, no credit card, no tax software, no crypto, and no private market access.3

Is Wealthsimple Premium Worth It at $100K?

Premium saves approximately $550 per year in hard-dollar value the moment you cross $100,000 — without counting any trading fee improvements.1

| Benefit | Annual Value |

|---|---|

| Management fee reduction (0.50% → 0.40% on $100K) | $100 |

| USD account fee waived ($10/mo) | $120 |

| Visa Infinite annual fee waived ($20/mo) | $240 |

| Tax Plus plan included (retail $40) | $40 |

| Cash interest boost (0.50% on $10K cash) | $50 |

| Recommended pick. Total Verified Annual Value | $550 |

That $550 represents a 0.55% yield overlay on a $100,000 portfolio, generated entirely independent of market returns — just for maintaining status. The benefits activate automatically when you cross the threshold.

Two people at the same address can pool assets to reach the $100K threshold together, with each household member selecting their own Milestone Rewards independently — see the Household feature breakdown below for the mechanics.

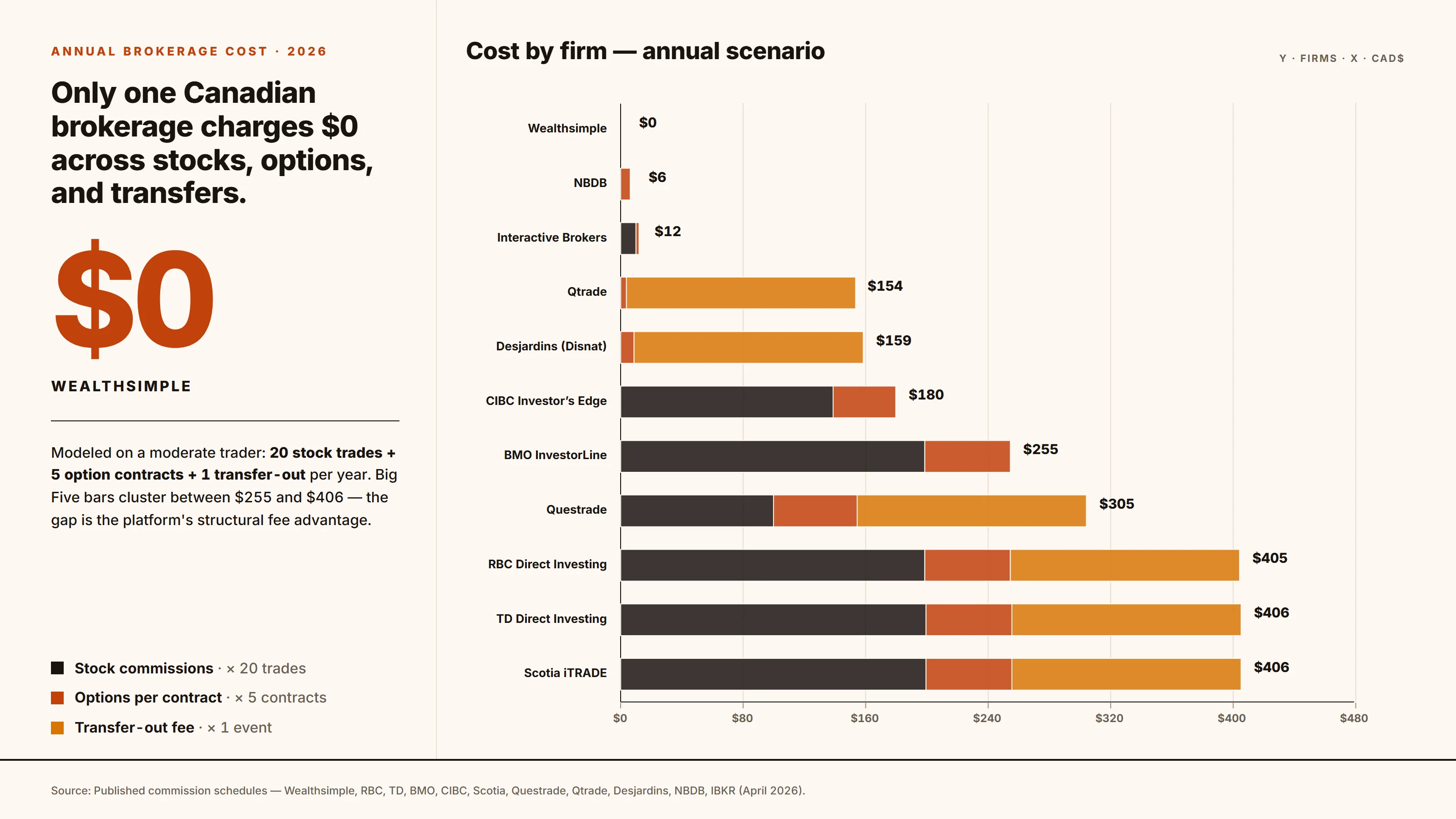

How Do Wealthsimple’s Trading Fees Compare to Other Canadian Brokerages?

Wealthsimple charges $0 commission on stocks, ETFs, and options across all tiers — making it the only Canadian brokerage with truly zero trading fees on every product.1

| Platform | Stock/ETF Commission | Options (Per Contract) | Transfer-Out Fee |

|---|---|---|---|

| Recommended pick. Wealthsimple | $0 | $0 | $0 |

| Questrade | $0 buy ETFs / $4.95–$9.95 sell | $9.95 base + $1.00 | $150 |

| National Bank (NBDB) | $0 | $0 base + $1.25 (min $6.25) | — |

| Qtrade | $0 | $0 base + $0.75 | $150 |

| Desjardins (Disnat) | $0 | $1.25 (min $8.75) | $150 |

| Interactive Brokers | $0.005/share (tiered) | $0.15–$0.65 | $0 |

| RBC Direct Investing | $9.95 | $9.95 + $1.25 | $150 |

| TD Direct Investing | $9.99 | $9.99 + $1.25 | $150 |

| BMO InvestorLine | $9.95 | $9.95 + $1.25 | — |

| CIBC Investor's Edge | $6.95 | $6.95 + $1.25 | — |

| Scotia iTRADE | $9.99 | $9.99 + $1.25 | $150 |

The Big Five banks still charge $6.95–$9.99 per stock trade. For an investor making 20 trades per year, that is $140–$200 in commissions that Wealthsimple eliminates entirely.5

What Changed in Wealthsimple’s Pricing for Self-Directed Traders?

Between late 2025 and April 2026, Wealthsimple made four pricing changes that improve the platform for self-directed traders.

Options went to $0 across all tiers. Previously, Core clients paid $2 USD per contract and Premium/Generation paid $0.75 USD. As of late 2025, the fee is $0 for everyone. This makes Wealthsimple the only Canadian platform with zero options commissions and zero per-contract fees.7

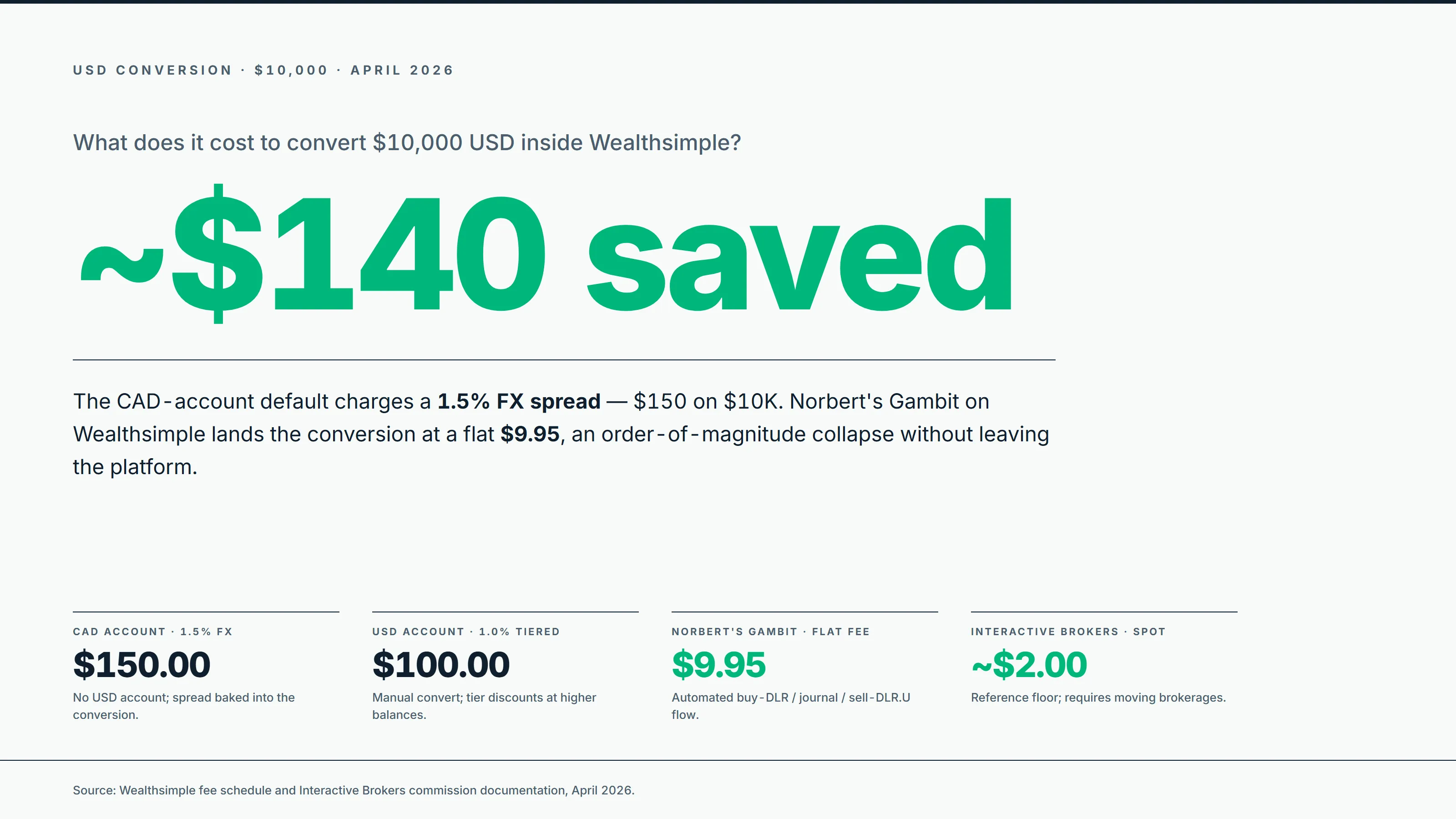

Automated Norbert’s Gambit launched in April 2026. For a flat $9.95 CAD fee, Wealthsimple now handles the purchase, journaling, and settlement of dual-listed ETFs (DLR/DLR.U) automatically in about 2 business days. Previously, investors who wanted to avoid the 1.5% FX fee on US trades had to manually execute this strategy on platforms like Questrade or NBDB.8

On a $10,000 USD conversion, the savings are substantial:

| Method | Cost on $10K |

|---|---|

| Wealthsimple CAD account (no USD) | $150 (1.5% FX) |

| Wealthsimple USD account (manual convert) | $100 (1.0% tiered) |

| Wealthsimple Norbert's Gambit (automated) | $9.95 |

| Interactive Brokers (spot rate) | ~$2 |

For investors converting $25,000 or more at once, Wealthsimple’s tiered FX schedule drops the fee to 0.50% ($25K–$99K) or 0.00% ($100K+). The FX tiers apply to anyone with a USD account, regardless of client tier.

Crypto fee tiers remain unchanged but worth noting: Core clients pay 2.0% per crypto trade, Premium pays 1.0%, and Generation pays 0.5%. Volume-based discounts further compress the Generation fee down to 0.05% at $10M+ in 30-day rolling volume. Wealthsimple takes 30% of staking rewards for Core and Premium clients, but only 15% for Generation — a meaningful difference for large staking positions.9

How Does the Wealthsimple Household Feature Work?

The Wealthsimple Household feature lets two people at the same residential address link their profiles to combine assets for tier qualification — without legally merging accounts.10

What Milestone Rewards and Visa Benefits Come with Each Tier?

Wealthsimple gamifies asset consolidation through Milestone Rewards — partner subscriptions unlocked at $100K increments, starting at $200K.11

Milestone Rewards thresholds and reward slots

- $100,000 0 reward slots — Premium tier financial benefits only

- $200,000 1 reward slot — choose 1 from the Wealthsimple Rewards catalog

- $300,000 2 reward slots — choose 2 (capacity grows, not the catalog)

- $400,000+ 3 reward slots — the cap, even at Generation

The catalog includes Uber One, DragonPass (airport lounges), Strava, Headspace, The Globe and Mail, Maple (virtual healthcare), Willful (online wills), DINR (restaurant access), and Gigs (international eSIMs). Each reward lasts 12 months from activation and must be manually re-selected upon expiry.

Reaching $500,000 (Generation) does not unlock a fourth reward. The cap is strictly 3.

The Visa Infinite Privilege card offers unlimited 2% cashback and 0% foreign transaction fees. The $240/year fee ($20/month) is waived automatically for Premium and Generation clients. Core clients can also get it waived with $4,000+/month in qualifying direct deposits.12

Generation clients who want airport lounge access must now combine two programs: 6 passes through the Visa Airport Companion program (requires the Visa Infinite Privilege card) plus 4 passes by selecting DragonPass as a Milestone Reward13 — for a maximum of 10 visits per year. This replaced the automatic 10-pass benefit that existed before January 2026. Unlike Big Five Visa Infinite Privilege cards, the Wealthsimple version does not support supplementary cardholders — legacy Big Five issuers typically allow them at $99–$149 each.

How Has Wealthsimple’s Tier System Changed in 2025–2026?

Wealthsimple’s trading infrastructure picked up four concrete improvements in 2025–2026, while three lifestyle and advisory benefits were restructured.

What got better:

- Options trading: Went from $2/$0.75 per contract to $0 across all tiers (late 2025)

- Norbert’s Gambit: Fully automated at a flat $9.95 fee (April 2026) — previously required manual execution on competitor platforms

- Direct indexing: Launched in November 2025 with a $1,000 minimum, enabling stock-level tax-loss harvesting that can boost after-tax returns by up to 0.5%14

- Summit Portfolio: Launched with private equity and credit access starting at $10,000 minimum allocation

- À-la-carte Conquest financial plan: Generation clients who want a one-time comprehensive retirement or estate plan without committing to the ongoing 0.90% Wealth Management fee can now pay a flat $2,500 for a Conquest-software-built plan

What was restructured:

- DragonPass lounge access: Changed from 10 automatic passes for Generation clients to a 6+4 split requiring Visa card enrollment plus a Milestone Reward selection (January 2026)

- Financial advisory: Previously included as a core Generation benefit, now the comprehensive planning service sits behind a separate Wealth Management tier at 0.90% of AUM ($1M+ minimum). Standard Generation clients retain access to basic financial planning sessions, but ongoing dedicated advisory requires the paid upgrade.15

According to Wealthsimple’s product team, the advisory shift was driven by demand: high-net-worth clients wanted year-round access to estate planning and complex tax optimization that the 0.40% fee simply could not subsidize. The 0.90% Wealth Management tier — scaling down to 0.50% at $10M+ — now competes directly with the Big Five’s full-service offerings at RBC Dominion Securities, CIBC Wood Gundy, and TD Wealth, which typically charge 1.25%–1.50%.16

The net result is an asymmetric upgrade: the core trading platform is objectively stronger than it was 12 months ago, with $0 options and automated FX as concrete improvements, while a meaningful slice of premium-tier benefits (DragonPass automatic access, year-round dedicated advisory) now sit behind additional spending or a separate paid tier. The trade-off favors active self-directed clients and disadvantages the lifestyle-benefits-first segment that originally chose Generation for the “white-glove” framing.

Is Wealthsimple Generation Worth a Dedicated Look?

Wealthsimple Generation targets the $500K+ investor who might otherwise consolidate with a full-service wealth manager. The tier adds private equity and credit access, 0.5% crypto fees with a 15% staking cut (half what Core and Premium pay), the Tax Pro plan, and what Wealthsimple positions as a dedicated advisory team.

But Generation’s value proposition goes deeper than what a tier comparison can cover. The real questions — how Generation’s 0.40% fee compares to RBC Dominion Securities at 1.25%, what happens to your status during a market crash, whether the advisory team’s planning sessions deliver concrete tax and estate strategy, and how Quebec residents lose access to Tax Pro and French-language advice — require their own analysis.

Our Wealthsimple Generation review covers the Big Five wealth manager fee comparison, downgrade mechanics, the HNW liquidity-event framing for private allocations, and the specific scenarios where $500K at Wealthsimple beats — or falls short of — traditional alternatives. For fund-level redemption math, sleeve-level fees, and the unified Private Market Fund’s 40/35/25 allocation, our Wealthsimple Private Market Fund review is the PRIMARY home.

How Does the Wealthsimple $25 Bonus Stack for First-Time Account Openers?

Everyone starts at Core, and every tier is eligible for the $25 cash bonus on your first $100 deposit. Add the code within 7 days of funding to claim.

Transferring a large portfolio? Wealthsimple’s ongoing transfer promotion adds a 1% cash match paid over 2 years on transfers of $25,000 or more — combined with the referral bonus, the match typically covers transfer-out fees ($150 at most Big Five brokers). The Monthly Millionaire stacks on top: register in the app each contest for 500 free entries, plus any deposits during the contest window add entries ($1 net = 1 entry, capped at 100,000). A Generation-tier reader moving $100,000+ in a single transfer maxes the cap on one move (or $50K with Direct Deposit active). See our current Wealthsimple promotions for the full stack mechanics and current contest window.

Promo code or referral code? They work differently. Our Promo Code vs Referral Code guide explains when each option saves you more.

Frequently Asked Questions

Can I combine assets with my spouse to reach Premium or Generation status?

Yes, through the Wealthsimple Household feature.10 Two people at the same residential address can link profiles to combine assets for tier qualification. If one partner has $60,000 and the other has $40,000, both receive Premium status. Members only see the combined total of accounts the other person explicitly shares — they cannot view individual transactions.

If the market drops my portfolio below $100K, do I lose Premium status?

Usually not. Wealthsimple determines your tier by net deposits OR total portfolio value, whichever is higher. If you deposited $100,000 and a market crash drops your value to $85,000, your net deposits still qualify you. You only risk a downgrade if you withdraw funds that bring both metrics below the threshold. If a downgrade is triggered, Wealthsimple provides a grace period with a specific date to top up your account.

Are Wealthsimple options really $0 per contract in 2026?

Yes. As of late 2025, Wealthsimple charges $0 per contract across Core, Premium, and Generation.7 The only remaining options-related fees are $45 USD for early exercise and $45 USD for a Do Not Exercise instruction. Standard automatic assignment at expiration is free.

How does the direct deposit interest rate boost work?

Core and Premium clients earn an extra 0.50% on their Wealthsimple Chequing balance by routing $2,000+/month in qualifying electronic payroll deposits. This brings Core from 1.25% to 1.75% and Premium from 1.75% to 2.25%. Generation clients already earn the 2.25% cap without any direct deposit requirement.17

Is Summit Portfolio only for Generation clients?

No. Summit Portfolio is available across all tiers with a minimum of $30,000 in total investable assets plus $10,000 to activate the private market allocation. It blends public ETFs with private equity and private credit in a single managed portfolio. For a detailed review of Summit’s 4-layer fee structure and the “47% richer” marketing claim, see our Wealthsimple Summit Portfolio review.

What happens to my Milestone Rewards if I get downgraded?

Wealthsimple reserves the right to claw back the prorated value of active rewards. If you selected a 12-month Uber One subscription and are downgraded in month four, you may be charged for the remaining eight months. The clawback is deducted from your cash balance.11

Does Wealthsimple charge for Norbert’s Gambit?

Yes, a flat $9.95 CAD fee. Wealthsimple launched automated Norbert’s Gambit in April 2026. The platform handles the dual-listed ETF purchase (DLR/DLR.U), journaling, and settlement in about 2 business days. This saves dramatically compared to the 1.5% FX fee on direct US trades from a CAD account.8

Is the Wealthsimple Visa Infinite Privilege card free?

Yes for Premium and Generation; Core clients earn the waiver via $4,000+/month in qualifying direct deposits.12 The card pays a flat 2% cashback with 0% foreign transaction fees but does not support supplementary cardholders — Big Five Visa Infinite Privilege cards typically allow supplementary cards at $99–$149 each.

Do referral bonuses count toward tier qualification?

The referral cash bonus itself is not classified as a “deposit” for net deposit calculations. However, the money you deposit to receive the bonus does count. If you deposit $100K to hit Premium and receive a $25 bonus on top, the $100K qualifies you.

What is Wealthsimple Tax Pro and who gets it free?

Wealthsimple Tax Pro is the premium tier of Wealthsimple Tax ($80 retail value). It includes 9+ returns (up to the CRA NETFILE limit of 20), a 30-minute live consultation with a tax expert, and audit protection. Generation clients receive it free. Premium clients get the mid-tier Tax Plus ($40 value, 8 returns + audit protection). Tax Pro is not available in Quebec or in French.

How long does it take to reach Premium after transferring assets?

Standard institutional transfers via the ATON system take 2–4 weeks.18 Complex accounts (RESPs, LIRAs, corporate) can take 6–8 weeks. The tier upgrade processes within about one business day once the assets settle and cross the $100,000 threshold. Wealthsimple reimburses transfer-out fees when you transfer $25,000 or more in a single transaction.

Sources

Footnotes

Based on published commission schedules from RBC Direct Investing, TD Direct Investing, BMO InvestorLine, CIBC Investor’s Edge, and Scotia iTRADE as of April 2026 ↩

Based on published fee schedules from RBC Dominion Securities Private Investment Management and CIBC Wood Gundy Portfolio Partner programs as of April 2026 ↩

- wealthsimple premium

- wealthsimple generation

- wealthsimple tiers

- wealthsimple fees 2026

- is premium worth it

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.