Wealthsimple Private Market Fund 2026: PE + Credit, No Accreditation Required

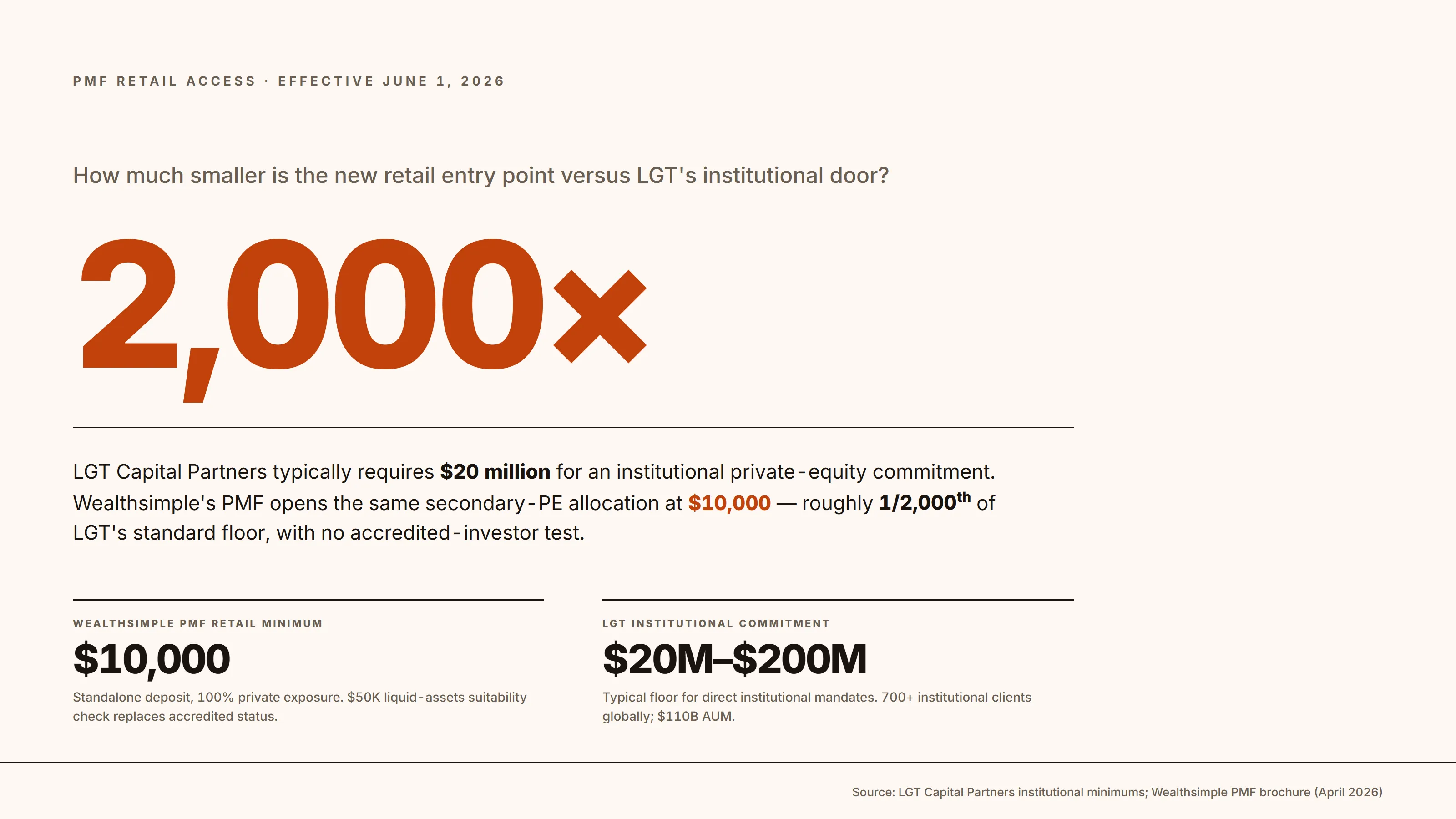

LGT Capital Partners ($110 billion AUM) and Sagard Holdings ($27 billion, CPPIB-anchored) typically gate institutional clients at $20 million-plus minimum commitments. The unified PMF opens both at a $10,000 retail threshold with a $50,000 liquid-assets suitability check replacing accredited status.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: On June 1, 2026, Wealthsimple’s standalone Private Equity and Private Credit funds collapse into a single Wealthsimple Private Market Fund (PMF) at a $10,000 retail minimum under the OM exemption — no accredited-investor status required.12 Both legacy products go dark to new capital that day; existing PE and PC holders auto-migrate at unit-for-unit exchange.

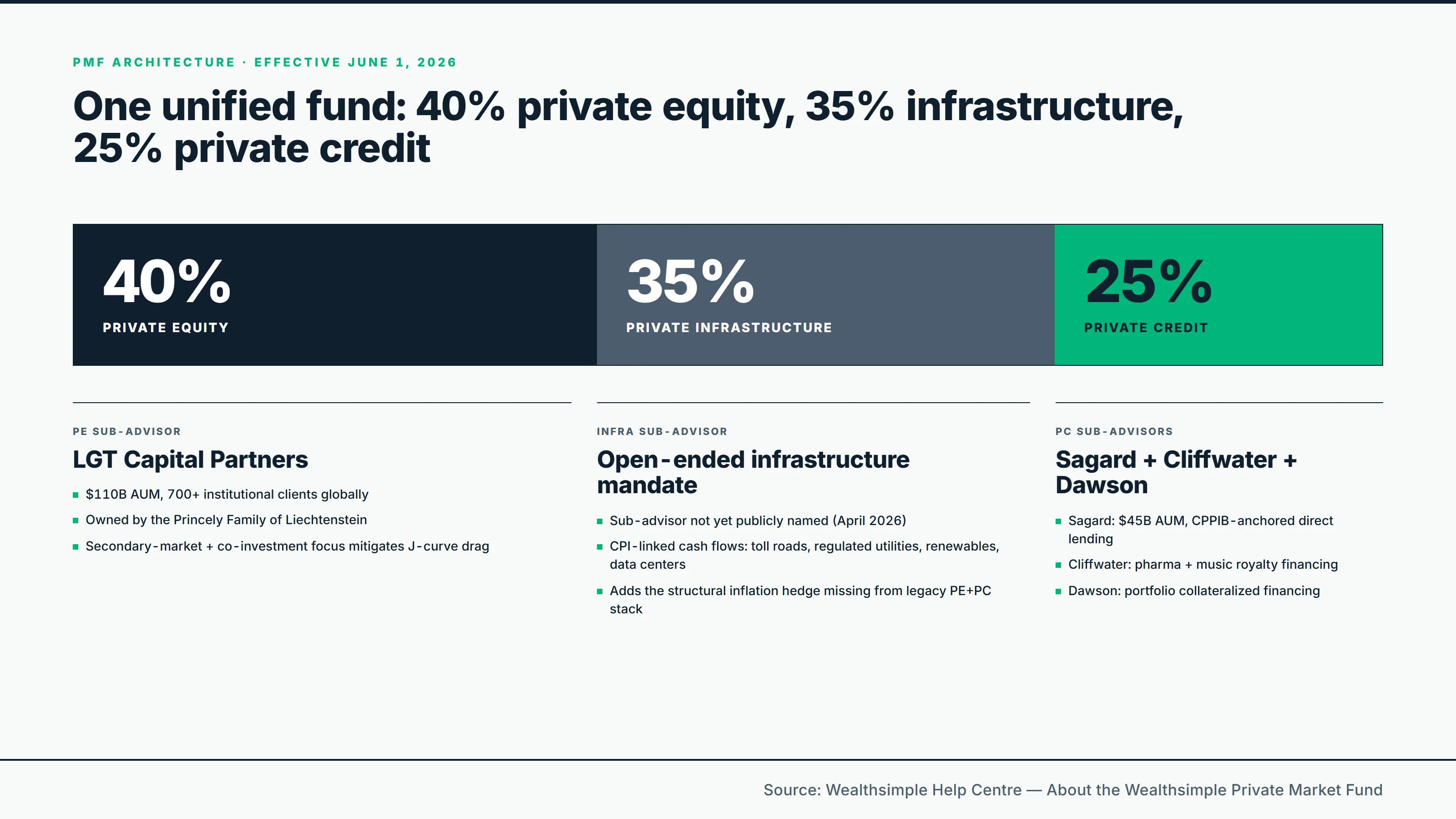

- 40% private equity / 35% private infrastructure / 25% private credit target allocation

- Standalone PE: 52.7% cumulative / 21.6% annualized since January 2024 ($434M AUM)3

- Standalone PC: 9.6% annualized distribution yield since June 2023 ($387M AUM)4

- National Instrument 45-106 OM exemption replaces the accredited-investor test

- $50,000 liquid-asset suitability check still applies (held internally or across other institutions)

How Reliable Is Wealthsimple’s 21.6% Private Equity Return?

The Wealthsimple Private Equity Fund has reported a 52.7% cumulative return and 21.6% annualized since launching in January 2024, with $434 million in AUM as of March 2026.3 The strategy invests through LGT Capital Partners’ secondary-market and direct co-investment programs rather than primary fund commitments, which is the structural reason the early returns clear public-market benchmarks so cleanly.

Primary private equity funds suffer a pronounced J-curve in years one through three, where management fees and acquisition costs depress returns into negative territory before value creation eventually accrues. Secondary-market purchases of mature, cash-flowing fund stakes — often acquired at a discount to NAV — and direct co-investments alongside established general partners without a second carry layer reverse that mechanic. Capital begins compounding from day one rather than enduring a multi-year drawdown.

The mark-to-model caveat is the load-bearing disclosure. The fund’s track record currently spans less than three years of a typical 7-to-10-year private equity investment lifecycle, and the reported returns are unrealized appraisal-driven valuations from third-party sources rather than finalized cash-on-cash exit realizations. Hayley and Sefiloglu (Bayes Business School, City University of London) found that non-parametric estimation reveals structural reporting biases that artificially boost private equity fund IRRs by an average of 3 percentage points per annum across commercial private market databases.5 Their finding applies industry-wide to Preqin-style indices and is the empirical reason Wealthsimple’s headline 21.6% number must be treated as encouraging early data rather than a guide to terminal-wealth outcomes. Brav, Lakan, and Yafeh’s broader analysis confirms that small funds and poor performers systematically drop out of commercial databases before publication, biasing reported aggregate returns upward.6

Sign-up bonus applied with our link.

How Does Wealthsimple Private Credit’s 9.6% Distribution Yield Actually Work?

The Wealthsimple Private Credit Fund has delivered a 7.7% annualized total return and a 9.6% annualized distribution yield since June 2023, with $387 million in AUM.4 The yield is engineered through Sagard’s direct lending program — bilateral, floating-rate senior-secured loans extended to middle-market Canadian and U.S. companies with $50 million to $1 billion in enterprise value.7

Sagard sits at the senior end of the corporate capital stack. In a default scenario, Sagard’s loans are repaid before subordinated debt, mezzanine, or equity, which is the structural reason private credit’s loss-given-default profile sits closer to investment-grade public bonds than to high-yield. Floating-rate exposure adjusts coupon income upward when central banks hike, hedging the duration risk that destroyed traditional bond portfolios through 2022.

Two specialty sub-advisors widen the portfolio beyond Sagard’s direct lending. Cliffwater handles pharmaceutical and music royalty financing extended to companies backed by major private equity sponsors such as Blackstone Inc. and KKR. Dawson Partners runs portfolio collateralized financing — providing liquidity to investors who pledge diversified portfolios as collateral. The cross-sector mix across banking, healthcare, leisure, telecommunications, and high-tech limits sector-specific default correlation.

The 9.6% headline is calculated net of Sagard’s 1.25% management fee and 15% performance fee above the 5% hurdle, but it does not include Wealthsimple’s platform advisory layer. The standalone PMF route’s 1.00% Wealthsimple management fee reduces the realistic delivered yield to approximately 8.0% net to the investor.8 The Summit Portfolio route lands at approximately the same 8.0% on the private allocation once the blended advisory rate is applied to the 30% private sleeve. The convergence is mathematical — both routes pay the same Sagard stack, and the platform advisory differential roughly washes out at the private-sleeve level. The 1.6 percentage points between the headline 9.6% and the delivered 8.0% is the cost of platform access, distribution, and suitability supervision.

What Is the Wealthsimple Private Market Fund (and Why Did It Replace PE/PC)?

The Wealthsimple Private Market Fund (PMF) is the unified successor vehicle launching June 1, 2026, blending 40% private equity, 35% private infrastructure, and 25% private credit through a single OM-exempt structure with monthly redemption windows.1 The 35% allocation to private infrastructure is the reason the fund exists in this shape: the standalone PE and PC funds did not include infrastructure, and the new sleeve adds CPI-linked cash flows from toll roads, regulated utilities, renewable generation, and data centers as a structural inflation hedge through an open-ended infrastructure mandate.

The migration mechanic is unit-for-unit at fair market value. Eligible standalone PE and PC unitholders are exchanged into PMF units of equal NAV. Only legacy Private Equity holders received an opt-out window, with a deadline of May 20, 2026; standalone PC holders did not receive an opt-out and migrate by default. Wealthsimple has selectively delayed migration for non-registered PE holders carrying material embedded capital gains to defer the disposition trigger.

KKR’s Evergreen Fund educational framework explains why retail capital benefits from this structure relative to traditional drawdown private equity.9 In drawdown funds, capital is committed but only “called” when deals close, often years after the commitment date. Uncalled capital sits in cash or low-yielding public assets, dragging IRR. Evergreen funds — including PMF — deploy capital immediately upon deposit into an existing mature portfolio, then continuously recycle proceeds and profits back into new investments. The capital-efficiency gain matters most for tax-sheltered accounts: a $10,000 RRSP or TFSA deposit begins compounding in private assets on day one rather than waiting through capital calls, maximizing the tax-deferred or tax-free growth window.

Wealthsimple’s own self-disclosure on the migration is unusually direct: “For most investors, total fees will be higher in the Private Market Fund than in the previous standalone funds. Wealthsimple has a financial interest in this migration, and we believe you should weigh that in your decision.”1

Who Manages Wealthsimple’s New PMF (Private Market Fund)?

Wealthsimple’s PMF allocates the private equity sleeve to LGT Capital Partners ($110 billion AUM, owned by the Princely Family of Liechtenstein) and the private credit sleeve to Sagard Holdings ($45 billion AUM following its April 2026 Unigestion combination, with Canada Pension Plan Investment Board as a limited partner).107 Wealthsimple has not yet publicly named the sub-advisor for the private infrastructure sleeve as of April 2026; the canonical disclosure will appear in the PMF brochure linked from Wealthsimple’s help center at fund launch.

LGT’s investment thesis runs on alignment economics that publicly traded peers cannot replicate. The Princely Family, alongside LGT executives and employees, maintains a principal co-investment of around $4 billion across the firm’s investment programs.10 LGT closed over $1.7 billion in secondary private equity transactions in the first half of 2025 and recently raised over $7 billion for Crown Global Secondaries VI. In the standard institutional ecosystem, allocating to an LGT mandate typically requires institutional commitments orders of magnitude beyond the retail tier — which is the reason Wealthsimple’s $10,000 retail threshold is non-trivial as access economics.

Sagard’s institutional credibility outside the Power Corporation umbrella is the answer to the related-party question. The fund’s limited partners include Canada Pension Plan Investment Board, the Wisconsin State Investment Board, the United Nations Joint Staff Pension Fund, and the Church Commissioners for England.7 Adam Vigna, Managing Partner and Chief Investment Officer of Sagard Credit Partners, previously served as Global Head of CPPIB’s Principal Credit Investments Group, overseeing roughly CAD $20 billion in AUM and leading the acquisition of Antares Capital. Sagard Credit Partners II reported a 16.8% gross IRR / 12.1% net IRR and closed at US$1.17 billion in 2022.7

Power Corporation of Canada is the controlling shareholder of both Wealthsimple (via Power Financial and IGM Financial) and Sagard, and the arrangement is classified as a related-party material conflict of interest in OSC filings.1112 Our Wealthsimple Summit Portfolio review covers the full disclosure mechanics, the mitigants Wealthsimple applies, and how the conflict surfaces specifically for Summit investors who hold both the public and private sleeves through the same managed wrapper.

The architectural philosophy underpinning the firm’s expansion into private markets traces back to Chief Investment Officer Ben Reeves, who joined Wealthsimple after a career at Bridgewater Associates and applies risk-parity principles to retail portfolio construction.

Markets move in cycles, so a strong, diversified portfolio has assets that perform well at different times.13

— Ben Reeves, Wealthsimple Chief Investment Officer

Reeves positions private markets as a mathematical necessity for retail rather than an institutional luxury. “We see a lot of opportunities for retail investors to improve their outcomes with alternatives,” Reeves stated, framing the firm’s mandate as making “high-quality private market investment opportunities available to investors beyond the ultra-wealthy.”13 His thesis on the illiquidity premium is grounded in the historical record: “From 2001 to 2023, private equity returned 10.5% versus the global stock market’s 5.7%.”13

Wealthsimple Private Equity vs Private Credit: Which Fits a Canadian Retail Portfolio?

The decision between standalone exposure to private equity, private credit, or the blended PMF turns on three variables: position in the corporate capital structure, intended portfolio role (capital appreciation versus income generation), and time horizon.

Private equity sits at the most junior position in the capital stack. Equity holders absorb the highest risk of loss in a corporate liquidation, and in exchange capture unbounded upside from enterprise value creation. Wealthsimple’s PE Fund targets aggressive long-term capital appreciation against mature, cash-flowing businesses rather than venture-stage companies, with an intended liquidity horizon exceeding 10 years. Private credit operates at the senior end. Lenders maintain a senior, often secured, claim on assets, intrinsically lowering the downside risk profile relative to equity, but the upside is mathematically capped at principal plus contracted interest. The PC Fund’s role is income generation across a 3-to-5-year horizon with a 9% targeted distribution yield. PMF blends both into a single endowment-model vehicle with a 7-to-10-year practical horizon, optimized for passive diversification rather than precise tactical allocation.

| Vehicle | Optimal investor profile | Primary objective | Risk position | Horizon | Optimal tax shelter |

|---|---|---|---|---|---|

| Standalone Private Equity (legacy until June 2026) | Aggressive growth; multi-decade timeline | Maximum long-term capital appreciation | High; junior unsecured | 10+ years | TFSA or RRSP |

| Standalone Private Credit (legacy until June 2026) | Income-focused; near or in retirement | Stable, high-yield cash flow | Moderate; senior secured | 3 to 5 years | RRSP or non-registered |

| Recommended pick. Blended PMF (post-June 2026) | Passive; endowment-model diversification | Balanced growth, yield, inflation hedge | Moderate to high | 7 to 10 years | TFSA or RRSP |

The blended PMF inherently eliminates precise tactical allocation. An investor near retirement who specifically required the 9% yield of standalone PC for immediate income generation cannot tolerate the 40% PE sleeve and the longer aggregate horizon. Conversely, a young accumulator with a multi-decade compounding window may treat the 25% PC and 35% Infrastructure allocations as an unnecessary anchor on aggregate returns and prefer concentrated PE exposure. After June 1, 2026, neither standalone option remains available to new investors — PMF is the only access route.

How Do You Access Wealthsimple PMF? Standalone Account vs Summit Portfolio Sleeve

The Wealthsimple Private Market Fund has two access routes after June 2026: the standalone PMF account routes 100% of deposited capital into private markets, while the Summit Portfolio sleeve caps private exposure at 30% within a 70% public, 30% private blend. The architectural decision determines fee burden, liquidity profile, and target investor type.

| Architectural feature | Standalone PMF account | Summit Portfolio sleeve |

|---|---|---|

| Accredited-investor required | No (OM exemption) | No (OM exemption) |

| Suitability — minimum liquid assets | $50,000 internal or external | $50,000 internal or external |

| Minimum investment | $10,000 deposit, 100% private | $10,000 net deposit, 30% private |

| Resulting private exposure | $10,000 of $10,000 deposited | $3,000 of $10,000 deposited |

| Wealthsimple advisory fee | 1.00% flat on total balance | 0.20%–0.50% public + 1.00% private |

| Liquidity profile | 100% subject to 5% NAV monthly gate | 70% liquid (T+1 to T+3); 30% gated |

| Target investor | Self-directed; pure-play satellite | Mass-affluent; fully outsourced endowment |

The standalone route fits investors who already manage their core public portfolios independently — typically through a self-directed brokerage — and want PMF as a satellite allocation without an accompanying Wealthsimple-managed public sleeve. The Summit route fits mass-affluent investors who prefer a fully outsourced wrapper where Wealthsimple manages the public 70% alongside the private 30%.

Costs converge at the underlying fund level. Both routes expose investors to the same Sagard 1.25% / 15% / 5% hurdle on private credit and the same LGT 1.50% / 12.5% / 8% hurdle on private equity. The divergence happens at Wealthsimple’s advisory layer: standalone applies a flat 1.00% to total account balance, while Summit applies the tiered 0.20%-0.50% advisory rate to the 70% public sleeve and 1.00% to the 30% private sleeve. On a total-account basis, Summit’s blended fee is mathematically lower because the public sleeve dilutes the advisory cost — but the dilution comes at the price of giving up 70% of capital to a managed-investing framework.

For Generation-tier clients, the advisory rate compresses from 0.40% at the $500K threshold down to 0.20% at $10M+, which materially narrows the standalone-vs-Summit fee differential. The full tier breakpoint mechanics, downgrade rules, and Quebec exclusions are covered in our Wealthsimple Generation review. The broader tier comparison and which Wealthsimple advisory rate applies to a Summit sleeve sits in our Wealthsimple Core vs Premium vs Generation comparison.

How Liquid Is Wealthsimple PMF: 5% NAV Monthly Windows vs the 7-Year LP Lockup?

PMF is structurally illiquid relative to public ETFs but materially more liquid than a traditional 7-to-10-year drawdown LP commitment, with redemptions processed in monthly windows that cap aggregate withdrawals at 5% of fund NAV. Cash arrives 30 to 60 days after submission rather than immediately on a sell click, and the fund manager retains discretion to suspend windows outright during stress events.

Redemption requests are submitted through a dedicated form rather than an in-app one-click flow, where holders enter account numbers and the dollar amount they wish to redeem. The form route is the default; holders can also place the request by phone with a Wealthsimple support agent.

Northleaf Capital’s institutional framing captures the structural logic: liquidity is not free.14 By accepting that capital cannot be liquidated on 24 hours’ notice, the investor provides long-term certainty to the underlying borrower or acquired company, and the borrower pays a distinct premium for that certainty — the illiquidity premium that manifests as the higher gross yields seen in private credit and private equity.15 Northleaf’s empirical observation is that retail investors rarely require 100% of their retirement portfolio to be liquidated on any given day, yet they continuously pay a performance penalty by keeping the entire portfolio in highly liquid, lower-yielding public stocks and bonds.

The 5% gating cap is structurally identical to comparable open-ended retail private market vehicles. Blackstone’s BREIT vehicle limited withdrawals to 2% of NAV per month and 5% per quarter through late 2022 and into 2023, gating excess requests pro rata for nearly a year before normalizing. Romspen Mortgage Investment Fund, a Canadian private debt vehicle, suspended redemptions outright during a 2022 stress period. Both episodes underscore that the underlying assets are fundamentally illiquid; the wrapper smooths access without changing the asset class’s underlying reality. PMF’s gating mechanism is the protective feature that prevents managers from holding return-destroying cash buffers in normal markets or fire-selling underlying assets during panics.

The gating implication differs sharply across the two access routes. Standalone PMF subjects 100% of the investor’s allocated capital to gating risk and potential suspension. The Summit Portfolio’s blended structure preserves 70% public-sleeve liquidity with T+1 to T+3 ETF settlement, which provides an immediately accessible liquidity buffer — exactly the angle Wealthsimple references when it positions Summit as the route that does not force investors to wait through monthly windows for unexpected cash needs.1 On a $50,000 Summit balance, that mechanic preserves roughly $35,000 of T+1-to-T+3 accessible capital alongside the $15,000 of gated PMF exposure, compared with the standalone route where the full $50,000 sits behind the 5% NAV gate.

How Does Wealthsimple PMF Compare to BMO Partners Group, iA, and Mackenzie-Northleaf?

PMF is not the only retail-accessible private market vehicle in Canada. Three institutional incumbents compete on overlapping mandates with materially different access economics.

| Fund | Asset mix | Minimum | Accredited required | Distribution channel |

|---|---|---|---|---|

| Wealthsimple PMF (standalone) | 40% PE / 35% Infra / 25% PC | $10,000 | No (OM exemption) | Direct, retail platform |

| Wealthsimple PMF (Summit sleeve) | 30% private (PMF) + 70% public | $10,000 net deposit | No (OM exemption) | Direct, managed-investing wrapper |

| BMO Partners Group Private Markets Fund | PE + PC + real estate + infra | $25,000 | Yes (NI 45-106) | iA Financial Group advisor channel |

| Mackenzie Northleaf Private Credit Interval Fund | Private credit only | $5,000 to $25,000 | No (interval-fund structure) | Mackenzie advisor channel |

| Ninepoint-Monroe U.S. Private Debt | Private credit only | $25,000 USD | No | Independent advisor channel |

Wealthsimple PMF’s distinctive angle is access economics. The OM exemption removes the accredited-investor test that gates BMO Partners Group, the $10,000 standalone minimum sits below BMO’s $25,000 and at the low end of Mackenzie-Northleaf’s range, and direct retail distribution removes the advisor-channel friction.16 BMO Partners Group’s countervailing strength is the longer institutional track record across Partners Group’s two-decade book of multi-asset private market mandates and the embedded distribution muscle of iA Financial Group, which manages over $341 billion in assets and operates one of Canada’s largest independent advisor networks.17

The Mackenzie Northleaf Private Credit Interval Fund and Ninepoint-Monroe U.S. Private Debt are single-asset competitors against PMF’s PC sleeve specifically.16 Mackenzie-Northleaf uses an interval-fund structure that offers periodic redemption windows comparable to PMF’s gating mechanics. Ninepoint-Monroe applies early-redemption penalties on capital withdrawn within the first one to two years, which is a friction PMF does not impose. KKR’s K-Prime and Blackstone’s BXPE are the institutional standards for retail-accessible private equity globally — both carry a 1.25% management fee and 12.5%-15% carry above a 5% hurdle, sitting at lower hurdle rates than LGT’s 8% but with higher carry rates than Sagard’s 15% on credit. Apollo’s S3 sits in the same retail-private-equity tier but has eliminated performance fees entirely to compete more aggressively on cost.

PMF’s competitive position is strongest against accreditation-gated alternatives like BMO Partners Group and weakest against single-asset interval funds where the issuer’s track record outruns Wealthsimple’s three-year history. For investors who specifically require the multi-asset 40/35/25 structure without accredited status, PMF is currently the only Canadian retail option matching that profile.

Should You Hold Wealthsimple PMF in an RRSP, TFSA, or Non-Registered Account?

The Wealthsimple Private Market Fund is fully eligible for RRSP, TFSA, and non-registered accounts, but the optimal architecture is account-type-dependent because the three sleeves generate distinct tax characters. The general TFSA-vs-RRSP-vs-FHSA priority logic sets the baseline; PMF’s three-sleeve mix layers further considerations on top.

TFSA shelters the entire upside. The 40% PE sleeve’s unbounded capital appreciation, the infrastructure sleeve’s growth component, and the PC sleeve’s interest income all compound tax-free in a Wealthsimple TFSA. For long-horizon accumulators, TFSA is the most tax-efficient container for PMF.

RRSP defers PC interest income. The PC sleeve’s distribution yield, which is otherwise taxed at the full marginal rate as interest income in non-registered accounts, compounds tax-deferred until withdrawal. RRSP is also the optimal home for retirees drawing on the PC yield as cash flow, since withdrawals are taxed at the (typically lower) post-retirement marginal rate. The PE and infrastructure sleeves benefit from RRSP tax deferral but lose the capital-gains advantage they would carry in a non-registered account.

Non-registered accounts trigger T3 trust slip reporting and require manual cost-base adjustment each year to avoid double taxation on eventual sale. Sagard’s PC sleeve generates interest income at the full marginal rate; LGT’s PE sleeve generates capital gains at the 50% inclusion rate. Quebec residents reconcile parallel federal T3 slips with provincial RL-3 (and RL-15 if any sleeve uses partnership structure), at combined federal-Quebec marginal rates that exceed 53% on the interest component for high earners. For non-registered investors carrying material embedded gains in the standalone PE fund, the June 2026 migration creates a forced disposition — Wealthsimple has selectively delayed migration for that book to allow strategic timing of the realization.

Who Should Hold Wealthsimple PMF and Through Which Access Route?

The Wealthsimple Private Market Fund is a legitimate, regulator-disclosed institutional-grade private market access vehicle for Canadian retail investors who would otherwise face NI 45-106 accredited-investor paperwork or seven-figure minimums to reach LGT and Sagard. The fit decision turns on three thresholds.

Standalone PMF account fits investors who hold at least $50,000 in liquid assets (the suitability hurdle), can commit $10,000+ as 7-to-10-year capital without dependence on monthly liquidity, and want concentrated 100% private exposure as a satellite allocation alongside an independently managed public portfolio. The route is structurally optimized for self-directed investors building their own core ETF allocations through a discount brokerage.

Summit Portfolio sleeve fits mass-affluent investors who want a fully outsourced wrapper where Wealthsimple manages the public 70% alongside the private 30%, and who prefer the 70% public-sleeve liquidity buffer over concentrated private exposure. The case strengthens at the Generation tier where the advisory rate compresses the all-in cost. The full Summit-specific architecture — risk profiles, blended liquidity, four-layer fee stack — is covered in our Wealthsimple Summit Portfolio review.

Neither route fits investors whose portfolio role for this allocation is daily liquidity, who require precise tactical asset allocation (PMF blends 40/35/25 by default and cannot be reweighted by the unitholder), or whose primary goal is low-fee public-market beta rather than alternative-asset access. For the cost-driven public-ETF case, our XEQT ETF review covers the all-in-one passive alternative.

Sign-up bonus applied with our link.

Frequently Asked Questions

Do I need to be an accredited investor to open a Wealthsimple Private Market Fund account?

No. The Wealthsimple Private Market Fund relies on the Offering Memorandum exemption under National Instrument 45-106, which allows distribution of private securities to retail investors without the accredited-investor test (the $200,000 income, $300,000 spousal income, $1 million financial-asset, or $5 million net-asset thresholds).2 Both the standalone PMF account and the Summit Portfolio sleeve apply a $50,000 minimum-liquid-assets suitability check, but neither requires formal accredited status.

What is the minimum to open a standalone Wealthsimple Private Market Fund account?

The standalone PMF route requires a $10,000 direct deposit allocated entirely to the private market vehicle, plus a $50,000 minimum-liquid-assets suitability gate held internally at Wealthsimple or externally across other institutions.1 The Summit Portfolio route applies the same $50,000 liquid-asset hurdle but invests only 30% of the account in PMF, so a $10,000 Summit deposit produces $3,000 of actual private exposure compared with $10,000 in the standalone account.

Can I keep my standalone Wealthsimple Private Equity or Private Credit fund after June 2026?

Only legacy Private Equity holders received an opt-out window, and the deadline expires May 20, 2026. After June 1, 2026, automatic migration moves all eligible standalone PE and PC unitholders into the unified PMF at a unit-for-unit exchange. Private Credit holders did not receive an opt-out option, so the migration is forced for that book. Wealthsimple has selectively delayed migration for non-registered Private Equity holders carrying material embedded capital gains to defer the disposition.1

What happens to my Wealthsimple PE or PC fund tax-wise during the June 2026 migration?

In RRSP and TFSA accounts the migration is non-taxable because the Canada Revenue Agency shields registered-account exchanges from disposition rules. In non-registered accounts the unit-for-unit exchange is treated as a disposition at fair market value, triggering immediate capital gains or losses for the 2026 tax year even though no cash leaves the account.1 Quebec residents reconcile parallel federal T3 slips with provincial RL-3 (and RL-15 if any sleeve uses partnership structure).

Why does Warren Buffett not like private equity?

Buffett raises three structural objections. First, the 2-and-20 fee model rewards asset gathering over capital allocation — managers earn regardless of outcome, in his words: “They are going to get rich no matter what happens.” Second, Internal Rate of Return is mathematically inflated by Subscription Lines of Credit that delay capital calls and shorten the official deployment window without raising cash-on-cash returns. Third, the industry’s reliance on debt to magnify returns introduces existential downside risk during downturns and rate hikes. Buffett contrasts this with Berkshire’s permanent-capital model, where acquired companies are run as long-term operating businesses rather than tradable assets.

What is the realistic yield I receive from Wealthsimple Private Credit after all fees?

The 9.6% headline distribution yield is calculated net of Sagard’s 1.25% management fee and 15% performance fee on returns above the 5% hurdle, but it does not include Wealthsimple’s platform advisory layer.4 The standalone PMF route reduces the realistic delivered yield to approximately 8.0% after the 1.00% Wealthsimple management fee. The Summit Portfolio route lands at approximately the same 8.0% delivered yield on the private sleeve once the blended advisory layer is applied.

Who manages the private equity allocation inside Wealthsimple PMF?

LGT Capital Partners runs the private equity sleeve.10 LGT manages over $110 billion globally for 700+ institutional clients, is privately owned by the Princely Family of Liechtenstein, and the Princely Family plus LGT executives co-invest more than $4 billion alongside client capital. The strategy emphasizes secondary-market transactions and direct co-investments rather than primary fund commitments, which mitigates the J-curve drag that typically depresses early-year private equity returns.

Is investing in private credit a good idea for a Canadian retail investor?

Private credit fits a Canadian retail portfolio when the allocation is sized as long-horizon discretionary capital and capped at roughly 20% to 30% of total assets. The post-2008 banking-retreat thesis is structurally sound — regulatory capital constraints pushed traditional banks out of middle-market lending, and private credit funds captured the resulting illiquidity premium. Floating-rate senior-secured loans hedge against rate hikes, and near-zero correlation with public equities provides genuine diversification. The asset class fails as a substitute for emergency reserves, since the 5% NAV gate and 30-to-60-day payouts make capital structurally unavailable during shocks.

How does the 5% NAV redemption gate actually work in practice?

Investors submit redemption requests within a defined monthly window (for example, June 1 to June 29 for a June 30 redemption date), and cash payout follows 30 to 60 days later.1 If aggregate redemption requests exceed 5% of fund NAV in that window, requests fill pro rata and the fund manager retains discretion to suspend withdrawals entirely. The mechanism prevents forced asset sales at distressed prices during macro shocks; Blackstone’s BREIT vehicle gated for nearly a year through 2022-2023 under similar mechanics, and Romspen Mortgage Investment Fund suspended redemptions outright during a 2022 stress episode.

How does Wealthsimple PMF compare to the BMO Partners Group Private Markets Fund?

Both vehicles bundle private equity, private credit, and private infrastructure into a single retail-accessible wrapper. BMO Partners Group requires accredited-investor status with a $25,000 minimum and is distributed through iA Financial Group’s advisor channel.1617 Wealthsimple PMF uses the OM exemption to remove the accreditation requirement, sets a $10,000 standalone minimum, and applies a $50,000 minimum-liquid-assets check rather than the income or asset thresholds of NI 45-106 accreditation. PMF lands lower on entry friction; BMO carries a longer issuer track record across institutional mandates.

Sources

Footnotes

Wealthsimple Help Centre — About the Wealthsimple Private Market Fund — including direct disclosure: “For most investors, total fees will be higher in the Private Market Fund than in the previous standalone funds. Wealthsimple has a financial interest in this migration, and we believe you should weigh that in your decision.” ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8

British Columbia Securities Commission — National Instrument 45-106 Prospectus Exemptions and Autorité des marchés financiers — Regulation 45-106 respecting Prospectus Exemptions ↩ ↩2

Wealthsimple Help Centre — Private Credit performance ↩ ↩2 ↩3

Hayley, S. and Sefiloglu, O. — “Biases in Private Equity Returns” (Bayes Business School, City University of London, 2022) ↩

Brav, A., Lakan, G., and Yafeh, Y. — “Private Equity and Venture Capital Fund Performance: Evidence from a Large Sample of Israeli Limited Partners” (SSRN, August 2023) ↩

Sagard — Retail Invest and Sagard Private Credit Fund ↩ ↩2 ↩3 ↩4

LGT Capital Partners — Who we are and LGT Capital Partners completes final close of Crown Global Secondaries VI ↩ ↩2 ↩3

Power Corporation of Canada — FinTech investment in Wealthsimple ($750M offering disclosure) ↩

Sagard Holdings — Relationship Disclosure Information (June 30, 2025) ↩

Direct quotes attributed to Ben Reeves, Wealthsimple Chief Investment Officer, sourced from Wealthsimple investor communications and CIO commentary including the Wealthsimple investor letter introducing private equity and the Wealthsimple Private Equity portal commentary. ↩ ↩2 ↩3

Mackenzie Investments — Mackenzie Northleaf Private Credit Interval Fund and Northleaf Capital Partners — Insights ↩

Bernstein — In Private Credit, Illiquidity is a Feature, Not a Flaw ↩

Investment Executive: BMO releases all-in-one private markets fund, Investment Executive: Mackenzie introduces interval private credit fund, and Ninepoint: Ninepoint-Monroe U.S. Private Debt Fund ↩ ↩2 ↩3

iA Financial Group — Investor Relations and Annual Reports and iA Capital Markets — About Us ↩ ↩2

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.