Wealthsimple Generation Review (2026): Is It Worth It at $500K+?

Wealthsimple Generation's management fee runs 110 basis points lower than a Big Five private banker — about $5,500/year in savings.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: Wealthsimple Generation activates at $500,000 in total deposits or market value, saves roughly $5,500/year in fees against a Big Five private banker, and delivers about $1,000-$1,500/year in measurable upgrades over Premium — plus access to private-fund products that are otherwise gated to institutional capital. The economics work decisively for HNW accumulators with active cash, crypto, or private-fund appetite, but the tier doesn’t replicate bespoke fixed-income engineering or holding-company tax structuring.

- 0.40% management fee at $500K, scaling to 0.20% above $10M (self-directed Trade is free at every tier)

- 2.25% CAD / 3.25% USD Cash interest — no direct-deposit requirement

- $240 Visa Infinite Privilege annual fee waived

- Private equity access at a $10,000 minimum (vs the $250K-$1M institutional norm)

- Tax Pro included (excluded for Quebec residents per AMF rules)

Wealthsimple Generation Deposit Qualification: 3 Paths to $500K

Wealthsimple Generation deposit qualification activates at $500,000 in total net deposits or total market value, whichever is higher, aggregated across your entire Wealthsimple ecosystem: managed and self-directed RRSPs, TFSAs, corporate accounts, crypto holdings, and Wealthsimple Cash balances all count.1 The dual-metric logic means there are three practical deposit paths to the $500,000 threshold, each with different timelines and edge cases.

Path 1. Own funds. Deposit or transfer $500,000 in any combination across your accounts. Net deposits are calculated as lifetime deposits minus lifetime withdrawals. Internal FX fees count as withdrawals, which means large USD conversions slightly reduce your tracked net-deposit figure. In-kind transfers via the ATON system take 2 to 4 weeks for standard registered, non-registered, LIRA, LIF, and corporate accounts; 2 to 6 weeks for pensions; and 6 to 8 weeks for RESPs. RESPs in particular can stretch beyond the published 6-8 week window when the relinquishing institution still requires physical cheques or manual “Part C” grant-transfer forms — capital sits uninvested during transit. Once assets physically settle and clear the threshold, the Generation upgrade processes in roughly one business day.

Path 2. Household pooling. Two members at the same residential address link profiles; combined assets satisfy the threshold for both. A couple with $350,000 and $150,000 in separate accounts linking up instantly unlocks Generation status for both individuals. Once linked, household members only see the combined total asset figure; partner-level account balances and trading activity remain private. See the Household Feature section below for the mechanics.

Path 3. Market-induced upgrade. Deposit less than $500,000, then allow time and compounding to carry your market value across the threshold. A client who deposited $250,000 in 2019 and whose portfolio has compounded to $510,000 triggers the automatic upgrade once the market value crosses the line. This path is asymmetric: if a subsequent market correction pulls the portfolio back under $500,000 but net deposits never reached that number, clients typically receive a 7-day grace period followed by a 90-day buffer before the downgrade executes, far more forgiving than the 1-day plus 30-day grace period applied to withdrawal-induced drops.

Referral bonus cash credits deposited into your account are not classified as deposits for the net-deposit calculation, but any principal you deposit to earn that bonus does count toward the qualifying ledger. Limited-time match promotions (like the Wealthsimple 1% Match 2026) also count toward the net-deposit ledger when active; see our promotions page for what’s running today. Net deposits during a Monthly Millionaire contest also earn contest entries ($1 net = 1 entry, capped at 100,000 per contest), so a single transfer toward the $500K Generation threshold can max the entry cap and feed the tier-qualifying ledger at the same time.

Sign-up bonus applied with our link.

What Wealthsimple Generation Benefits Do You Get at $500K in 2026?

Wealthsimple Generation’s headline draw at $500K is gated access to investment categories typically reserved for institutional capital — Private Credit, Private Equity, and the Summit Portfolio fund-of-funds — bundled with eight distinct fee and service upgrades that lower management, cash, crypto, and staking costs; add dedicated advisor access and a metal Visa Infinite Privilege card; and include Tax Pro filing software free.2

The Generation management fee applies only to Wealthsimple’s managed investing product; self-directed Wealthsimple Trade accounts remain free at every tier regardless of balance. On the managed side, the fee operates on a tiered scale ranging from 0.40% at the $500K threshold to 0.20% for clients with $10,000,000 or more in managed assets. Wealthsimple does not publicly disclose the intermediate breakpoints; clients consult an advisor to confirm the exact rate at their asset level.

The Wealthsimple Generation interest rate on Cash sits at 2.25% CAD base and 3.25% USD, 50 basis points higher than the Premium tier’s 1.75% base rate, and critically, Generation clients earn that rate without the direct-deposit requirement Premium clients must satisfy. The boost compounds against uninvested balances: a Generation client holding $100,000 in Cash earns roughly $500 per year more than a Premium client holding the same balance without direct deposit. USD-denominated Wealthsimple Cash, available at Generation tier, eliminates the conversion drag that erodes yield for clients transacting in U.S. dollars. These rates move with the Bank of Canada’s policy rate; Wealthsimple updates the posted rate within roughly 5 business days of a policy change. All Wealthsimple Cash balances are held in trust accounts at Canadian Schedule I banks with CDIC coverage up to $1,000,000 across the eligible institutions; see our Wealthsimple Cash account review for the full interest-tier structure.

The auxiliary services are where Generation earns its keep alongside the headline management fee. A client holding $100,000 in actively traded crypto saves $500 per $100,000 of volume at the 0.50% tier. The Visa Infinite Privilege card alone carries a $240 annual fee for Core clients, waived entirely at Generation.3 For frequent travelers, combining the 6 Visa Airport Companion passes with 4 additional DragonPass visits selected as a Milestone Reward yields 10 annual lounge visits entirely free of annual-fee friction.

The Visa Infinite Privilege offering diverges sharply from the legacy Big Five version. Wealthsimple Payments Inc. issues the card directly under a Visa Canada license, not through a partner bank, and earns a flat 2% cash back on all eligible purchases with 0% foreign transaction fees, both materially better than the tiered-points and 2.5% FX markup structure on a comparable RBC or TD Infinite Privilege card.4 Dedicated advisor access, Tax Pro software (an $80 retail value), Medcan Health discounts for Ontario residents (40% off Year-Round Care, 30% off Assessment), and a highest-priority 1-day technical support SLA round out the non-fee benefits.

Generation status also opens individual concessions that aren’t published in the standard pricing. The dedicated advisor relationship creates a channel to negotiate FX rates on six-figure conversions, request custom Cash interest tiers on uninvested balances above $250,000, or arrange one-off accommodations on transfer fees and account-opening logistics. None of this is documented or guaranteed; it’s an artifact of the relationship rather than a tier benefit. The door opens at Generation in a way it does not at Premium.

Younger DIY investors are more likely to seek the advice of a financial professional than their older DIY counterparts. Very few of those investors say there is sufficient information online to gain investment expertise.5

— Kapil Vora, Senior Director of Wealth Intelligence at J.D. Power

The Vora finding maps directly onto the Generation tier’s value proposition. The dedicated advisor relationship isn’t a vestigial perk for HNW clients who could otherwise self-direct — it’s the bridge between a DIY ledger and the structured investment categories (Private Credit, Private Equity, Summit Portfolio) that gate behind the $500K threshold.

Wealthsimple Generation vs Wealthsimple Premium: Is It Worth It?

Upgrading from Wealthsimple Premium ($100K+) to Wealthsimple Generation ($500K+) unlocks roughly $1,000 to $1,500 per year in quantifiable incremental benefits plus access to a category of investments otherwise gated to institutional money. The recurring fee reductions come from the 50-basis-point cash yield bump, halved crypto trading fees, the 15% (versus 30%) staking cut, the upgraded Tax Pro benefit, and dedicated advisor access. The access category covers Private Credit, Private Equity, and Summit Portfolio funds.

| Feature | Wealthsimple Premium ($100K+) | Wealthsimple Generation ($500K+) | Generation Advantage |

|---|---|---|---|

| Managed Investing Fee | 0.40% flat | 0.40% → 0.20% only above $10M | Same fee until $10M+ assets |

| Cash Interest (no-DD path) | 1.75% CAD | 2.25% CAD / 3.25% USD | +$500/yr per $100K Cash |

| Crypto Trading Spread | 1.00% | 0.50% | –$500 per $100K traded |

| Crypto Staking (WS takes) | 30% | 15% | +0.675 SOL/yr per 100 SOL staked |

| Tax Software | Tax Plus ($40 value) | Tax Pro ($80 value) | +$40/yr |

| Advisor Access | Pooled | Dedicated team (CIM/CFA Level 1 baseline) | Dedicated team vs. pool |

| Private Credit / Private Equity | Not available | Eligible ($10,000 minimum) | Generation-only access |

| Summit Portfolio Eligibility | Not available | Available | Generation-only access |

| Visa Infinite Privilege Card | Fee waived | Fee waived | Same waiver in both tiers |

| Medcan Health (Ontario) | Not available for Wealthsimple Premium | 40% Year-Round Care / 30% Assessment | Generation-only benefit |

| Support SLA | Priority | Highest priority (1-day technical) | Faster SLA at Generation |

One clarification matters before running the upgrade math: most Premium-to-Generation upgraders see no immediate change in the headline 0.40% management fee. Wealthsimple discloses the Generation fee as a tiered scale ranging from 0.40% at the $500K threshold to 0.20% at $10M+, with intermediate breakpoints not publicly disclosed; the marketed “as low as 0.20%” floor applies at the upper end of that scale. For clients between Premium and the upper Generation breakpoints, the upgrade economics live in private-markets access and the auxiliary-service lift, not in the management line item — and for many Generation clients, the gated access to Private Credit, Private Equity, and Summit Portfolio funds is the headline draw.

Premium and Generation both waive the $240 Visa Infinite Privilege annual fee, so the card itself is neutral on the upgrade math. The case for upgrading rests entirely on the cash, crypto, staking, advisor, and private-markets columns above.

For a client already at Premium with $100,000 in Cash, active crypto trading, and moderate staking exposure, the upgrade recaptures roughly $1,000 to $1,500 per year in fee reductions plus the qualitative lift of dedicated advisory and private-markets eligibility. For a client holding mostly ETFs in registered accounts with minimal cash and no crypto activity, the quantifiable delta narrows toward $100 per year, in which case the decision hinges on whether private-markets access matters. The framing question is which Generation services your portfolio actually uses, not whether the tier is “better” in the abstract.

Is Wealthsimple Generation Worth It vs Full-Service Wealth Managers?

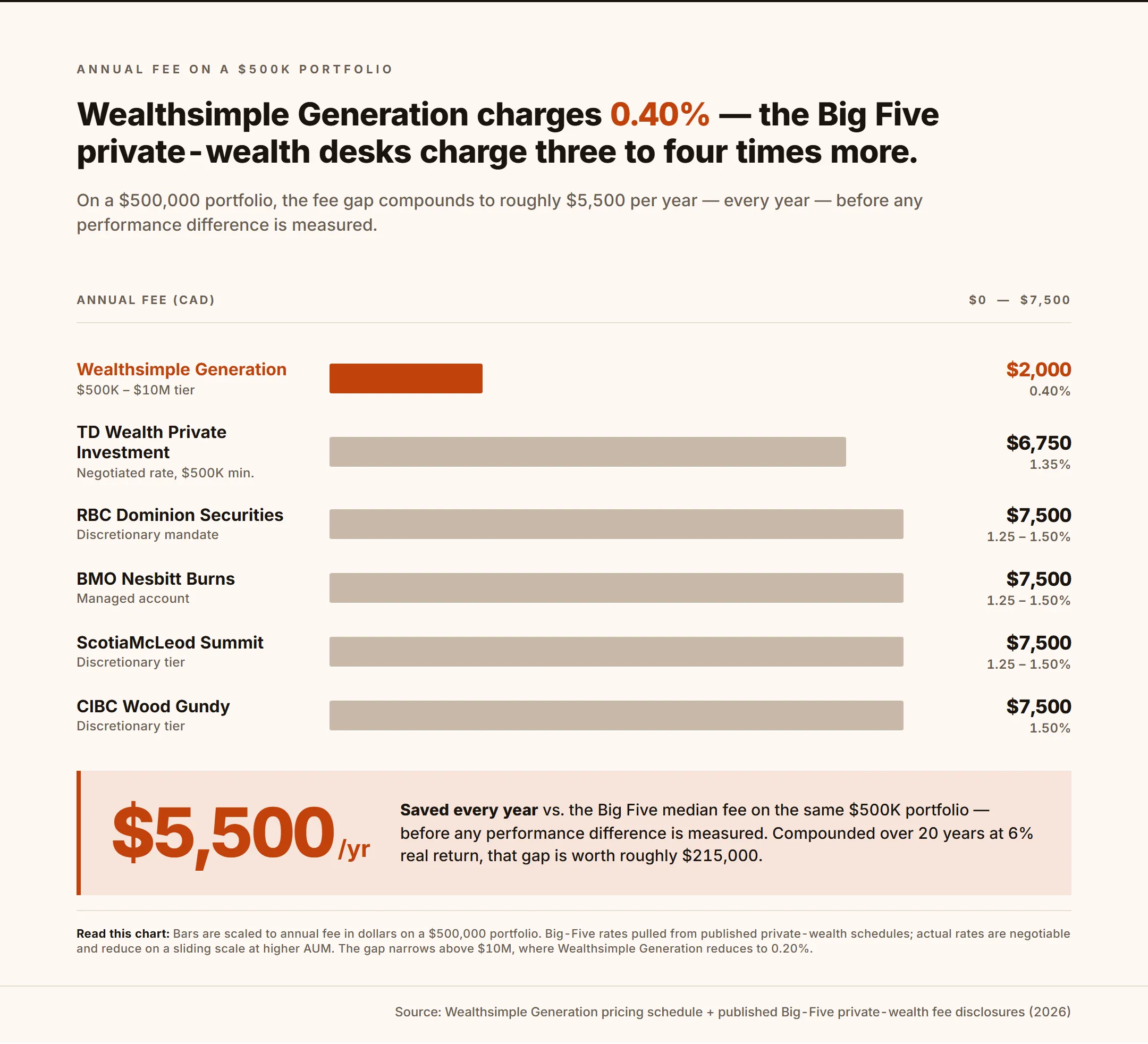

Wealthsimple Generation charges roughly $2,000 per year on a $500,000 portfolio (0.40% × $500K). A comparable program at RBC Dominion Securities, TD Wealth Private Investment Advice, or BMO Nesbitt Burns typically sits at a grid rate of 1.25% to 1.50% at the same portfolio size, roughly $6,250 to $7,500 per year, though Big Five advisors frequently negotiate these down to 1.10%–1.25% to win competitive accounts. The 110-basis-point midpoint spread equals $5,500 in annual fee drag a Generation client avoids.6

| Institution & Program | Minimum Threshold | Annual Fee at $500K–$1M | Included at $500K |

|---|---|---|---|

| Recommended pick. Wealthsimple Generation | $500,000 | 0.40% + 0.12–0.23% MER | Algorithmic rebalancing, baseline financial planning, auto tax-loss harvesting |

| RBC Dominion Securities Private IM | $500,000 | 1.25%–1.50% | Dedicated portfolio manager, custom bond ladders, holistic estate planning |

| TD Wealth Private Investment Advice | $500,000 | 1.35% on first $1M | Discretionary management, integrated tax strategies, HNW network access |

| CIBC Wood Gundy Portfolio Partner | $150K–$250K | 1.50% at $500K–$1M | 100+ commission-free trades, customized asset allocation, waived registered fees |

| BMO Nesbitt Burns Advance/Architect | $100K–$150K | 1.25%–1.50% | Unified managed accounts, quarterly reviews, institutional money management |

| ScotiaMcLeod Summit Program | $250K+ | 1.25%–1.50% | Discretionary management via Northern Trust, detailed tax reporting |

Source: Published fee schedules from RBC Dominion Securities, TD Wealth, CIBC Wood Gundy, BMO Nesbitt Burns, and ScotiaMcLeod public documentation as of April 2026.6

The $5,500 annual spread is not free money. A Big Five advisor at $500,000 typically builds customized fixed-income architecture: institutional-grade corporate bond ladders with specific maturity dates and yield requirements, crossover strategies, and enhanced corporate credit. Wealthsimple Generation cannot build a custom bond ladder; clients are restricted to broad-market bond ETFs. The Big Five advisor also coordinates directly with external estate lawyers and CPAs to structure holding companies, family trusts, and intergenerational wealth transfers, coordination the Generation baseline advisor is not mandated to provide.

In our view, for a client who wants a globally diversified passive portfolio and does not require bespoke tax or estate engineering, the mathematics favor Generation decisively. For a client with a holding company and a 10-year decumulation plan, the extra 110 basis points at a Big Five advisor purchases meaningful structural value.

For the trading-fee and fee-schedule baseline that sits under both tiers, see our Wealthsimple Core vs Premium vs Generation tier comparison.

How Does Wealthsimple Generation Compare to Wealthsimple Summit Portfolio?

Wealthsimple Generation is a client tier; Wealthsimple Summit Portfolio is a managed product. The two are routinely confused because both became available in the same product release and both reference private markets. A client can be at Generation tier and not own Summit. A client can own Summit and be at Core tier; the Summit product page positions it for clients with $30,000 in investable assets, with a hard $10,000 net-deposit threshold required to activate the private market allocation.7

Summit Portfolio is a fund-of-funds structure blending public market ETFs with Private Credit and Private Equity in three risk profiles: Aggressive (70% public equities / 30% private), Growth (60% public / 15% fixed income / 25% private), and Balanced (48% public / 32% fixed income / 20% private). Fees stack in two parts: the standard Generation management fee (0.40% → 0.20%) on the public sleeve plus a separate 1.00% management fee on the private sleeve, on top of the underlying LGT and private credit fund fees.

For the detailed audit of the Summit Portfolio’s “47% richer” marketing claim, two-part fee math, and monthly subscription windows that cause onboarding cash drag, see our Wealthsimple Summit Portfolio review.

What Is the Wealthsimple Generation Household, and Can It Extend Beyond Two Members?

The Wealthsimple Generation household links two members at the same residential address to pool assets toward the $500,000 threshold. Wealthsimple has extended that cap to additional household members on a case-by-case basis for clients with assets well above $500,000.8 For full mechanics on the address-based two-person rule, common-law eligibility, and Premium-tier interactions, see the Wealthsimple tier comparison.

The two-person household cap extension is not a published entitlement. Wealthsimple handles these requests individually through priority support; an account manager will typically ask for proof of address to verify the additional family member resides at the same home before overriding the standard two-person limit. The path generally fits a primary user who independently holds well over $500,000 in personal assets and wants to extend benefits to adult children, siblings, or elderly parents at the same address. Clients exploring this should first register, fund their account, and qualify as a Generation member on their own merit, then reach out to Wealthsimple client support once onboarded.

Sign-up bonus applied with our link.

What Are the Real Liquidity Constraints on Wealthsimple Generation Private Assets?

Wealthsimple Private Credit and Private Equity redemptions can take four to five months from the withdrawal decision to cash in hand, a liquidity profile most competitor reviews either skip or understate.9 Public ETFs in a managed Generation account settle in roughly T+1 business day. Private allocations are a different instrument class with quarterly windows, mandatory notice periods, and structural gating during liquidity crises — material friction for an HNW client who might need to fund a real estate purchase, business acquisition, or other liquidity event on short notice.

A client holding private assets who later drops below the $100,000 Premium threshold is not force-liquidated. Forcing liquidation would violate the quarterly liquidity constraints of the underlying funds and trigger unintended tax events. Instead, existing positions are retained indefinitely, but the client is barred from making new contributions while at Core status.

For the full mechanics — fund-level gating math, sector exposures, sleeve-level fees, post-June 2026 unified PMF redemption windows, account-type fit, and TFSA suitability — see our Wealthsimple Private Market Fund review.

What Tax Benefits Do Wealthsimple Generation Clients Get?

Wealthsimple Tax Pro is included free for Generation clients, an $80 retail value that covers up to 20 returns (to the CRA NETFILE limit), a 30-minute live video or phone consultation with a tax expert, and audit defense if the CRA or Revenu Québec flags a filed return.10 Auto-fill-my-return syncs T-slips and brokerage capital gains data directly from Wealthsimple accounts, and unlimited access to forms for rental income, foreign dividends, and charitable donations removes the escalating-paywall structure typical of legacy tax software.

Beyond the software, the managed investing product executes automated tax-loss harvesting within non-registered accounts, flagging eligible losses daily and crystallizing them to offset realized gains when the 30-day superficial-loss window allows. This is mechanical, not advisory; it operates inside the 0.40% management fee and does not require client action.

Two important limitations shape the real value of the Tax Pro benefit:

Quebec exclusion. The 1-on-1 expert advice components of Tax Pro are not offered to Quebec residents in either English or French. Quebec Generation clients can still file their core return (federal and provincial) through the software itself, but cannot access premium audit defense against Revenu Québec or the pre-filing expert consultation. For mediation on filing disputes, Quebec residents rely on the free service offered directly by the Autorité des marchés financiers.

When to engage an external CPA instead. The bundled Tax Pro consultation handles routine return prep but doesn’t substitute for senior tax planning. Specific gaps observed in 2025 and 2026 tax seasons include advisors instructing clients to split capital gains 50/50 with a non-working spouse on jointly held accounts (which violates CRA income attribution rules that tax based on source of capital), and providing incorrect guidance on USD-denominated T5008 slips and brokerage commission treatment (these should factor into adjusted cost base, not carrying charges). The software is elite; the bundled human team functions more like entry-level software troubleshooters than sophisticated tax strategists. Clients with holding company structures, corporate dividend sprinkling, or complex estate rollovers should engage an external CPA rather than rely on the free consultation.

For a deeper treatment of Wealthsimple Tax’s capabilities, pricing tiers, and feature-by-feature comparison against TurboTax and H&R Block, see our Wealthsimple Tax review.

Open a Wealthsimple account to start consolidating toward Generation status. Large transfers qualify for the 1% cash match on deposits of $25,000+ paid as 24 monthly payments, which stacks with the standard referral credit on your first deposit; see our promotions page for the full stack of active incentives.

When Is Wealthsimple Generation Not Worth It?

Wealthsimple Generation is best paired with external expertise for three client profiles: retirees executing decumulation strategies, business owners with complex corporate architecture, and liquidity-constrained investors eyeing private markets. The wealth accumulator with a globally diversified passive portfolio, active cash and crypto balances, and appetite for private-markets access gets full value standalone. For the three profiles, Generation still delivers the quantifiable fee economics and product access; the gap is in advisory depth, best addressed by adding a fee-only CFP or external CPA.11

Profile 1: Retirees running a decumulation strategy. Retirement drawdown requires nuanced, case-specific work: RRSP meltdown timing, OAS clawback avoidance, systematic withdrawal ordering across corporate and personal accounts, pension integration, and coordinated CPP start-date optimization. The Generation 0.40% fee covers the managed investing product and goal-setting sessions but is not designed to subsidize the 15 to 20 hours per year of CFP-level drawdown modeling. Retirees typically pair Generation with a one-time fee-only engagement (commonly $2,000 to $4,000 every two to three years) for the planning depth, while keeping the portfolio’s all-in cost low. Clients still accumulating toward retirement who want to accelerate contributions should consider the Wealthsimple Retirement Accelerator as a complement to the Generation portfolio.

Profile 2: Business owners with complex corporate architecture. Wealthsimple supports corporate accounts for retained-earnings investment, and the 0.40% Generation fee on those balances is materially below what a Big Five private bank charges. Capital dividend account (CDA) tracking, refundable dividend tax on hand (RDTOH), intercompany dividend flows, and holding-company tax optimization sit outside the standard Generation advisor’s scope. Most business owners pair Generation with their existing CPA or move to the separate paid 0.90% Wealth Management tier when corporate complexity warrants year-round advisory.

Profile 3: Liquidity-constrained investors eyeing private markets. Private Credit and Private Equity carry a four-to-five-month redemption window plus a 5% quarterly gate. Clients with realistic probability of needing to liquidate a large position for a business acquisition, real estate purchase, or other liquidity event should keep that capital in public market instruments, where same-day exits are possible. The rest of the portfolio still benefits from the Generation tier; private-markets allocations are an opt-in, not a requirement.

The strategic alternative for any client who falls into one of these patterns is to use Generation for the portfolio and add an external specialist for the depth: a fee-only financial planner for retirees, a CPA for business owners, or a portfolio specialist for liquidity sequencing. Over a 10-year horizon on a $500K portfolio, this combination secures both the Generation fee economics and deep tailored planning at roughly the same all-in cost as a single Big Five engagement, with materially higher planning alpha. For a self-directed alternative outside the managed product entirely, see our XEQT ETF review or the just buy XEQT rationale.

The Generation tier is the right destination for the wealthy accumulator who wants a globally diversified passive portfolio, a premium credit card, sovereign-insured cash yields, private-markets access, and a single mobile interface covering the entire banking relationship. For clients whose financial complexity has already outgrown the algorithm, Generation still works as the portfolio engine; the planning depth comes from a complementary external engagement.

Frequently Asked Questions

Is Wealthsimple Generation basically the same as having a private banker?

No. A private banker at RBC Dominion Securities or CIBC Wood Gundy builds custom corporate bond ladders, coordinates with external estate lawyers and accountants, and structures holding companies, family trusts, and intergenerational transfers. Wealthsimple Generation provides algorithmic ETF portfolios, a baseline financial goal-setting session, and a 0.40% all-in fee that decisively beats Big Five economics on any portfolio that does not require bespoke fixed-income engineering. For clients who do need that depth, Wealthsimple offers a separate paid Wealth Management tier starting at 0.90%.

Can I get a dedicated human advisor with Wealthsimple Generation, or is it just algorithmic?

Generation clients get access to a team of advisors holding CIM or CFA Level 1 credentials, plus complimentary financial goal-setting sessions. These are scheduled consultations rather than continuous, year-round fiduciary relationships. Continuous advisory access requires opting into the paid 0.90% Wealth Management tier.

What is the Wealthsimple Generation interest rate?

Wealthsimple Generation pays 2.25% on CAD Cash balances and 3.25% on USD Cash balances as of April 2026, 50 basis points above the Premium tier base rate of 1.75%. Generation clients earn these rates without the direct-deposit requirement Premium clients must meet. Rates move in line with Bank of Canada policy and typically update within roughly 5 business days of a policy change. All Cash balances are held in trust accounts at Canadian Schedule I banks with CDIC coverage up to $1,000,000 across the eligible institutions.

What happens to my Generation status if I withdraw a large sum?

A downgrade only triggers if both your net deposits and total market value fall below $500,000 simultaneously. If you withdraw $100,000 and the withdrawal pulls both metrics under the threshold, Wealthsimple applies a 1-day initial notice followed by a 30-day grace period before the formal downgrade. Market-only drops (net deposits still above $500K) do not trigger a downgrade at all.

How long does it take to get Generation status after transferring $500K in?

Holders typically report that status upgrades are not instantaneous upon initiating a transfer. The assets must physically settle and clear the $500,000 threshold first. Standard ATON transfers from a Big Five brokerage take 2 to 4 weeks; complex accounts like LIRAs or corporate structures can take 6 to 8 weeks. Once the deposit crosses the threshold, the upgrade typically processes within one full business day.

What is the Wealthsimple 0.80% Wealth Management tier, and how is it different from Generation?

The Wealth Management tier is a separate paid service launched in late 2025, requiring $1,000,000+ in managed assets. It replaces the 0.40% Generation fee with a 0.80% Service Fee at the $1M entry tier (scaling to 0.50% at $10M+) and adds a dedicated fiduciary partner, advanced tax-loss harvesting, estate planning, and year-round advisory. It targets clients who previously would have used an RBC Dominion Securities or TD Wealth full-service program.

Are Quebec residents excluded from Wealthsimple Tax Pro under Generation?

Yes. Wealthsimple Tax Pro, which includes the 1-on-1 expert consultation and audit protection components, is legally excluded from being offered to Quebec residents. The core tax software still files Revenu Québec returns, but francophone Generation clients cannot access the premium audit defense or expert pre-filing consultation. For mediation on filing disputes, Quebec residents use the free service offered directly by the Autorité des marchés financiers.

Does the Wealthsimple Visa Infinite Privilege card allow supplementary cardholders?

No. Wealthsimple Payments Inc. issues the Visa Infinite Privilege directly and does not currently support supplementary cards. Legacy Big Five VIP cards typically offer supplementary cards at $99 to $149 each, which households often use to consolidate spending under a single rewards account. This is the primary reward-structure limitation for affluent families using the Wealthsimple VIP card.

How much do Generation clients keep on Wealthsimple crypto staking rewards?

Generation clients keep 85% of staking yield (Wealthsimple takes 15%), versus 70% at Core and Premium (Wealthsimple takes 30%). For the full crypto fee schedule, volume-tiered trade fees, and the SOL math behind the staking cut, see our Wealthsimple Core vs Premium vs Generation comparison.

What FX rate do Wealthsimple Generation clients pay on USD conversions?

Generation clients receive permanent access to USD-denominated Wealthsimple Cash accounts, with the $10 monthly USD account fee applied to Core waived entirely. This eliminates FX conversion for USD holdings and spending. For conversions that do occur, Wealthsimple applies a volume-tiered rate: 1.50% under $10,000, 1.00% from $10,000 to $25,000, 0.50% from $25,000 to $100,000, and 0.00% on single conversions of $100,000 and over (executed at the WSII Corporate rate with a 0.42% embedded spread). For HNW clients liquidating US RSUs or repatriating cross-border proceeds, a six-figure conversion avoids the 1.50% retail penalty entirely.

Sources

Footnotes

Wealthsimple Help Centre — Understand the different client statuses ↩

Wealthsimple — Compare Generation, Premium, and Core Plans & Fees ↩

Wealthsimple — Premium and Generation rewards and benefits ↩

Wealthsimple — Credit Card Account Agreement and Wealthsimple Help Centre — Credit Card Benefits ↩

Investment Executive — Younger DIY investors more likely to seek human advisor: J.D. Power ↩

Published fee schedules from RBC Dominion Securities Private Investment Management, TD Wealth Private Investment Advice (Premier Guided Portfolios), CIBC Wood Gundy Portfolio Partner, BMO Nesbitt Burns Advance/Architect, and ScotiaMcLeod Summit Program as of April 2026. ↩ ↩2

Wealthsimple Help Centre — Create a Wealthsimple household ↩

Wealthsimple Help Centre — About the Wealthsimple Private Credit Fund and About the Wealthsimple Private Equity Fund ↩

Failure-mode categorization based on Wealthsimple Financial Advice Terms & Conditions and aggregated client experience reports as of April 2026. ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.