XEQT ETF Review 2026: The Complete Guide to Canada's Most Popular ETF

BlackRock's $14.8B all-equity fund-of-funds — what the wrap fee, rebalancing mechanics, and foreign withholding tax drag actually mean for your returns.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

TL;DR: BlackRock manages $14.8 billion in XEQT — Canada’s largest all-equity ETF. Most reviews stop at the 0.20% MER, but the real cost is closer to 0.40-0.50% once foreign withholding tax drag hits your TFSA, RRSP, or FHSA. Despite that, XEQT is still likely the best single-fund option for most Canadians investing long-term.

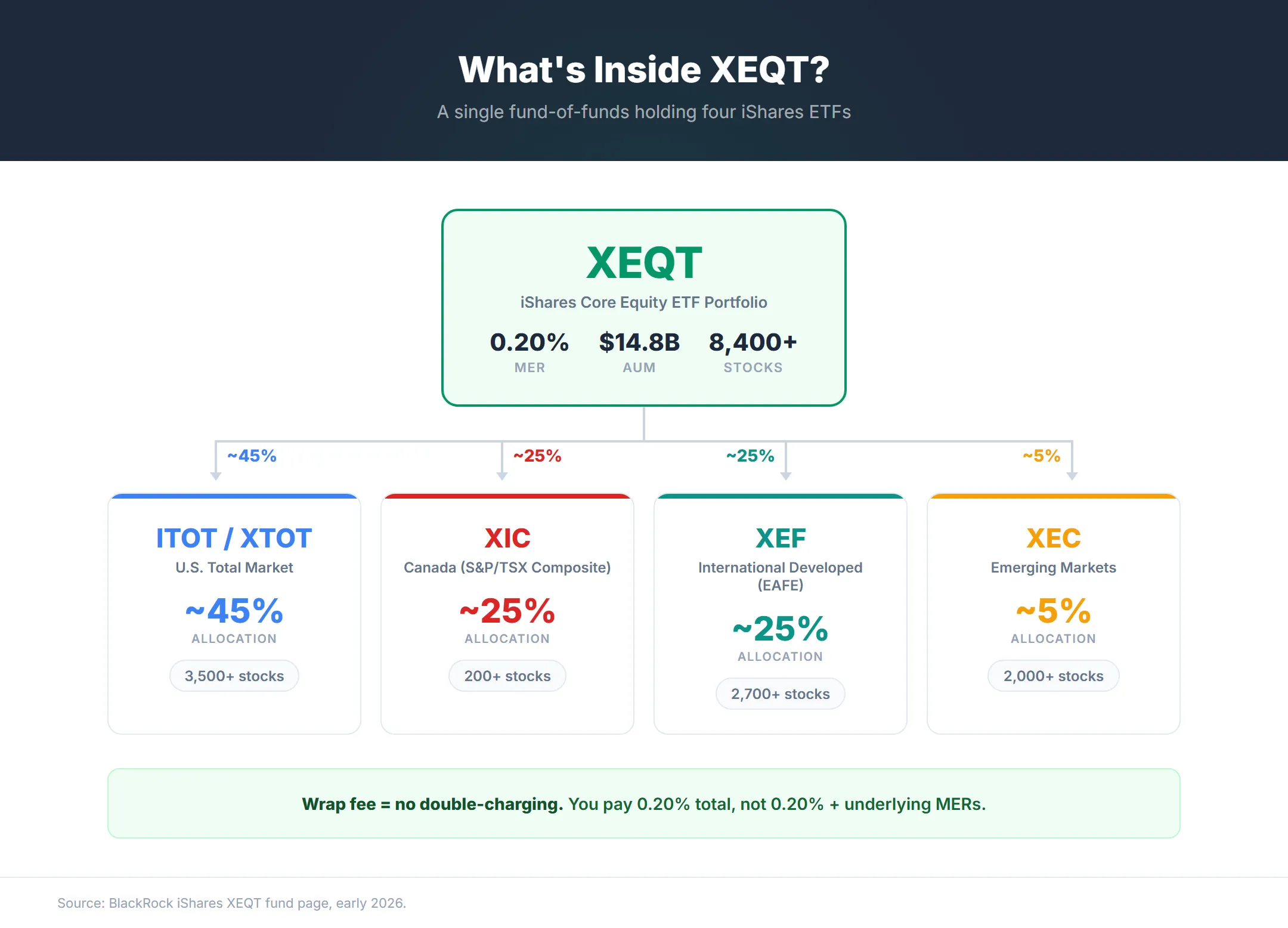

- 4 underlying iShares ETFs: ~45% U.S., 25% Canada, 25% international, 5% emerging

- Auto-rebalances when any holding drifts more than 10%

- Below ~$250K, the simplicity is worth more than the MER savings of going DIY

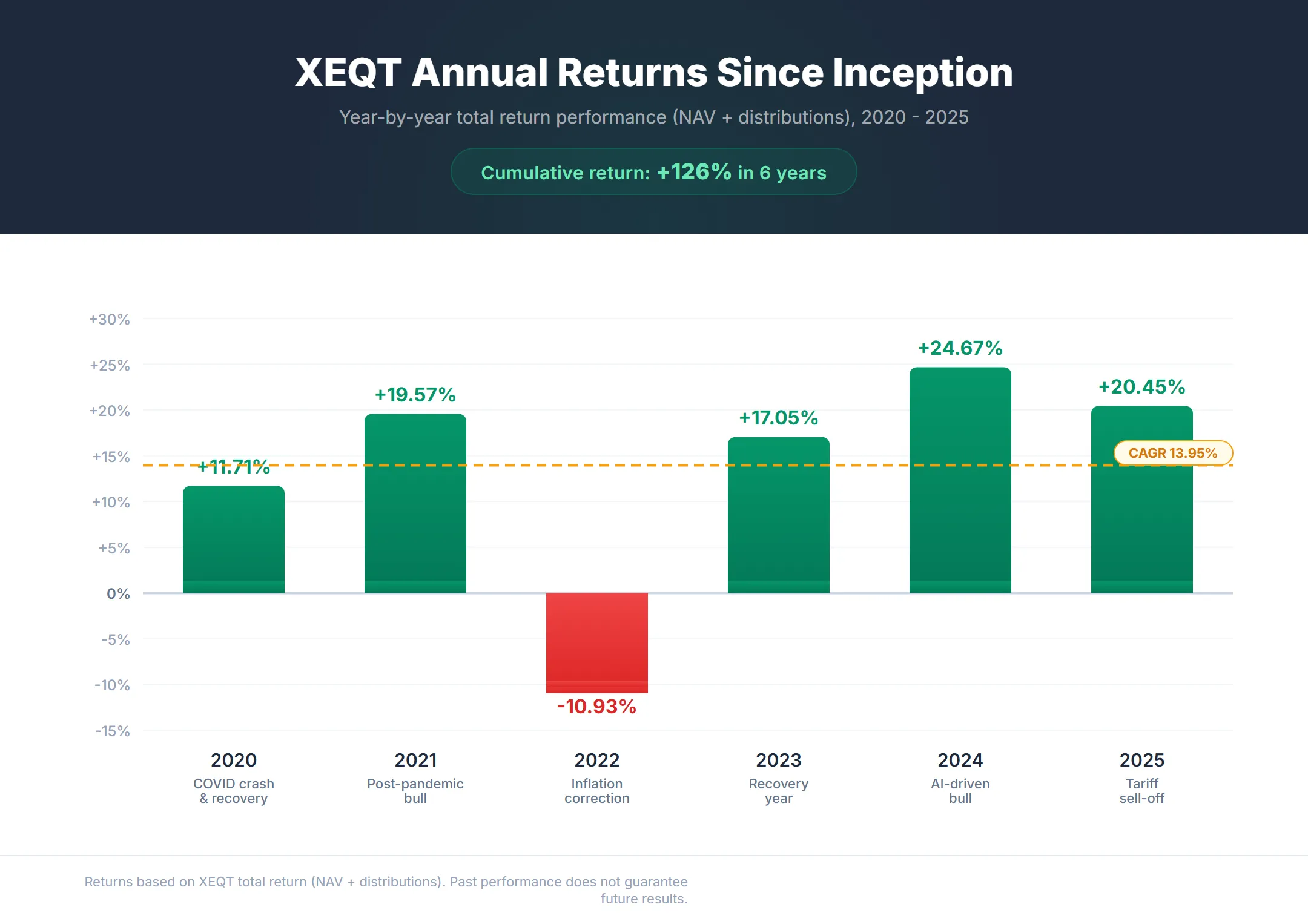

XEQT replaced what used to require buying and rebalancing three to five separate ETFs — one purchase, automatic rebalancing, done. The fund has returned 13.95% annualized since its August 2019 launch, including a 30% COVID drawdown and a -10.93% year in 2022. That track record, combined with a 0.20% wrap fee and $14.8 billion in assets, is why it became the largest all-equity ETF in Canada. For the cultural story behind the movement, see our “Just Buy XEQT” guide.

How Is XEQT’s Fund-of-Funds Structure Built?

The iShares Core Equity ETF Portfolio (TSX: XEQT) is a fund-of-funds that holds four underlying iShares ETFs covering 8,400+ stocks across 50+ countries for a single 0.20% MER — replacing what used to require buying and rebalancing three to five separate funds. BlackRock Canada launched XEQT on August 7, 2019.

XEQT Holdings and Geographic Breakdown

| Underlying ETF | Region | Target Weight | What It Covers |

|---|---|---|---|

| ITOT/XTOT | United States | ~45% | Total U.S. stock market (large, mid, small-cap) |

| XIC | Canada | ~25% | S&P/TSX Composite — broad Canadian equities |

| XEF | International Developed | ~25% | Europe, Australasia, Far East |

| XEC | Emerging Markets | ~5% | China, India, Brazil, Taiwan, and others |

XEQT’s MER is 0.20%, with a management fee of 0.17% following BlackRock’s December 2025 reduction.1 This is a wrap fee — investors do not pay the underlying ETF MERs on top. There is no double-charging. On a $100,000 portfolio, XEQT costs $200 per year.

The fund-of-funds structure is what Dan Bortolotti, creator of the Canadian Couch Potato blog, described as something he “used to dream of” early in his career — a single product that eliminated the friction of manual multi-ETF portfolio construction.2 Before all-in-one ETFs existed, achieving the same global diversification required buying ITOT, XIC, XEF, and XEC separately, calculating rebalancing thresholds, and executing trades quarterly. XEQT collapsed that complexity into one purchase.

You can buy XEQT on Wealthsimple with commission-free trades and fractional shares starting at $1 — the simplest way to get the 0.20% MER fund into your TFSA, RRSP, or FHSA.

Why Does XEQT Allocate 25% to Canada?

BlackRock deliberately set XEQT’s 25% Canadian allocation overweight relative to Canada’s 3% share of global market capitalization — an overweight factor of roughly 8x. Research from Vanguard and PWL Capital suggests a 25-35% home bias is optimal for Canadian investors for three reasons.3

First, holding Canadian-dollar-denominated assets reduces currency volatility across a quarter of the portfolio. Second, Canadian equities generate eligible dividends that qualify for the Canadian Dividend Tax Credit — a significant tax advantage in non-registered accounts. Third, a moderate home bias has historically lowered overall portfolio volatility without meaningfully degrading long-term expected returns.

International diversification is crucial, both theoretically and empirically, to sensible portfolio construction.4

— Ben Felix, Portfolio Manager at PWL Capital and host of the Rational Reminder podcast

While some argue that overweighting a small, resource-heavy market concentrates sector risk, we find this trade-off manageable at 25%. VEQT (Vanguard) takes a slightly more aggressive home bias at 30%, while ZEQT (BMO) lands at roughly 24%. All three fund providers independently arrived at similar allocations.

How Does XEQT Rebalance — and When Should You DIY Instead?

BlackRock automatically rebalances XEQT when any underlying ETF drifts more than 10% from its target weight. Rather than selling overweight positions (which would trigger capital gains in taxable accounts), BlackRock uses daily cash flows from new investor purchases and internal dividend reinvestments to buy whichever holding is currently underweight.1

This natural rebalancing eliminates three costs that manual investors face: trading commissions, bid-ask spreads, and the behavioural drag of selling winners to buy losers. For most retail investors, these invisible costs matter more than the 0.20% MER.

The $250,000 breakpoint. In our experience, for portfolios under $250,000, the mathematical and operational costs of manual rebalancing negate the minor MER savings from holding the underlying ETFs directly.5 Above that threshold — and especially above $500,000 — a multi-ETF structure may offer meaningful savings through foreign withholding tax recovery and more granular account placement. But below it, XEQT’s automatic rebalancing is worth paying for.

Is XEQT Currency Hedged?

XEQT is fully unhedged. None of its four underlying ETFs — ITOT/XTOT, XIC, XEF, or XEC — use currency hedging. This means your returns reflect both equity performance and currency movements between the Canadian dollar and foreign currencies.1

When the CAD weakens against the USD (as it did through much of 2024-2025), unhedged investors benefit from the currency tailwind — U.S. holdings are worth more in Canadian dollar terms. When the CAD strengthens, it acts as a drag.

Over long time horizons, currency effects tend to wash out. This is why BlackRock and Vanguard both default to unhedged structures in their all-in-one ETFs. Currency hedging adds cost (typically 0.10-0.30% annually), introduces tracking error, and only benefits investors with short time horizons where a sudden CAD appreciation could lock in losses. For a 10+ year holding period, the academic consensus favours unhedged exposure.

For a detailed comparison of how XEQT’s unhedged structure performs against the S&P 500 (which carries concentrated USD exposure), see our XEQT vs VFV analysis.

How Has XEQT Performed Through Every Crisis Since 2019?

XEQT has delivered approximately 13.95% annualized since its August 2019 inception — a return earned through a global pandemic, an inflationary correction, and tariff-driven market volatility. The honest picture includes the drawdowns.

| Year | Return | Context |

|---|---|---|

| 2020 | 11.71% | COVID crash (-30% in March) and recovery |

| 2021 | 19.57% | Post-pandemic bull market |

| 2022 | -10.93% | Inflation + aggressive rate hikes |

| 2023 | 17.05% | AI-driven recovery |

| 2024 | 24.67% | Continued global growth |

| 2025 | 20.45% | Strong year despite tariff volatility |

| Timeframe | Annualized Return |

|---|---|

| 1-year (2025) | 20.45% |

| 3-year (2023-2025) | 20.59% |

| 5-year (2021-2025) | ~14.00% |

| Since inception (Aug 2019) | ~13.95% |

During the March 2020 COVID crash, XEQT dropped approximately 30% — its price fell below $17 on March 20, 2020.6 The 2022 correction cost investors 10.93% for the year. In April 2025, U.S. “Liberation Day” tariffs triggered a roughly 10% drop in two days across global markets.

In every case, investors who stayed the course recovered. Financial planner Robb Engen of Boomer & Echo describes the optimal XEQT strategy as behaving like an “emotionless robot” — automated contributions, no market timing, no portfolio changes during drawdowns.7 XEQT ended 2025 up 20.45%.

These drawdowns are the price of admission for 100% equity exposure. If you can’t hold through a 30% crash without selling, consider XGRO (80/20 equity/bond) for built-in cushioning.

Does XEQT Pay Dividends?

XEQT pays quarterly distributions at the end of March, June, September, and December/January, with a trailing 12-month yield of approximately 2%. Distributions have grown steadily since inception, though payout amounts fluctuate quarter-to-quarter because the four underlying ETFs pay on different internal schedules.8

BlackRock designed XEQT for capital growth, not income. The 2% yield is a byproduct of the dividends paid by the 8,400+ underlying stocks — it’s not a distribution strategy. If you turn on Dividend Reinvestment (DRIP) in Wealthsimple’s self-directed platform, distributions are automatically reinvested into more XEQT shares, compounding your position without requiring manual purchases. Wealthsimple’s DRIP is synthetic — it reinvests at market price rather than offering a discount from the fund provider, but it removes the manual step.

In our experience, distributions don’t always appear on the exact payout date — they typically process after trading hours and may show up the next business day.

In our experience, for investors who need income, XEQT is the wrong tool. Dividend-focused ETFs like VDY or income-oriented balanced funds serve that purpose better.

What Is the Foreign Withholding Tax Drag on XEQT?

XEQT loses approximately 0.20-0.30% annually to foreign withholding taxes — a hidden cost that most XEQT content ignores. Understanding why requires the Justin Bender framework of Level I and Level II withholding taxes.9

Level I tax: The U.S. government withholds 15% on dividends paid by American companies to foreign investors. Under the Canada-U.S. tax treaty, this tax is waived for U.S.-listed assets held directly in an RRSP.

Level II tax: When international dividends pass through a U.S.-listed ETF before reaching Canada, the U.S. takes an additional 15% cut on top of what the originating country already withheld.

Here’s the trap: the RRSP exemption does NOT apply to XEQT. Because XEQT is a Canadian-listed ETF (traded on the TSX), the IRS does not recognize the end-investor’s Wealthsimple RRSP treaty-exempt status. The U.S. withholds 15% on the dividends generated by XEQT’s underlying U.S. component (ITOT/XTOT) before the cash enters the Canadian wrapper.

| Account Type | Level I (U.S.) | Recoverable? |

|---|---|---|

| Wealthsimple TFSA | Withheld | No — lost permanently |

| RRSP | Withheld | No — RRSP exemption doesn’t apply to Canadian wrappers |

| Wealthsimple FHSA | Withheld | No |

| Non-registered | Withheld | Yes — recoverable via foreign tax credit |

Globe and Mail columnist Rob Carrick has noted that Canadian retail investors had about “$47-billion invested in U.S.-listed ETFs,” urging investors to “buy domestic” instead for simplicity.10 In our assessment, the simplicity argument holds for most investors — XEQT’s simplicity outweighs the ~0.25% annual FWT drag. For portfolios above $500,000, however, holding U.S.-listed ETFs directly in an RRSP through Norbert’s Gambit can recover some of that tax. If you’re still deciding which registered account to fund first across your TFSA, RRSP, and FHSA, our TFSA vs RRSP vs FHSA decision guide walks through the trade-offs by life stage.

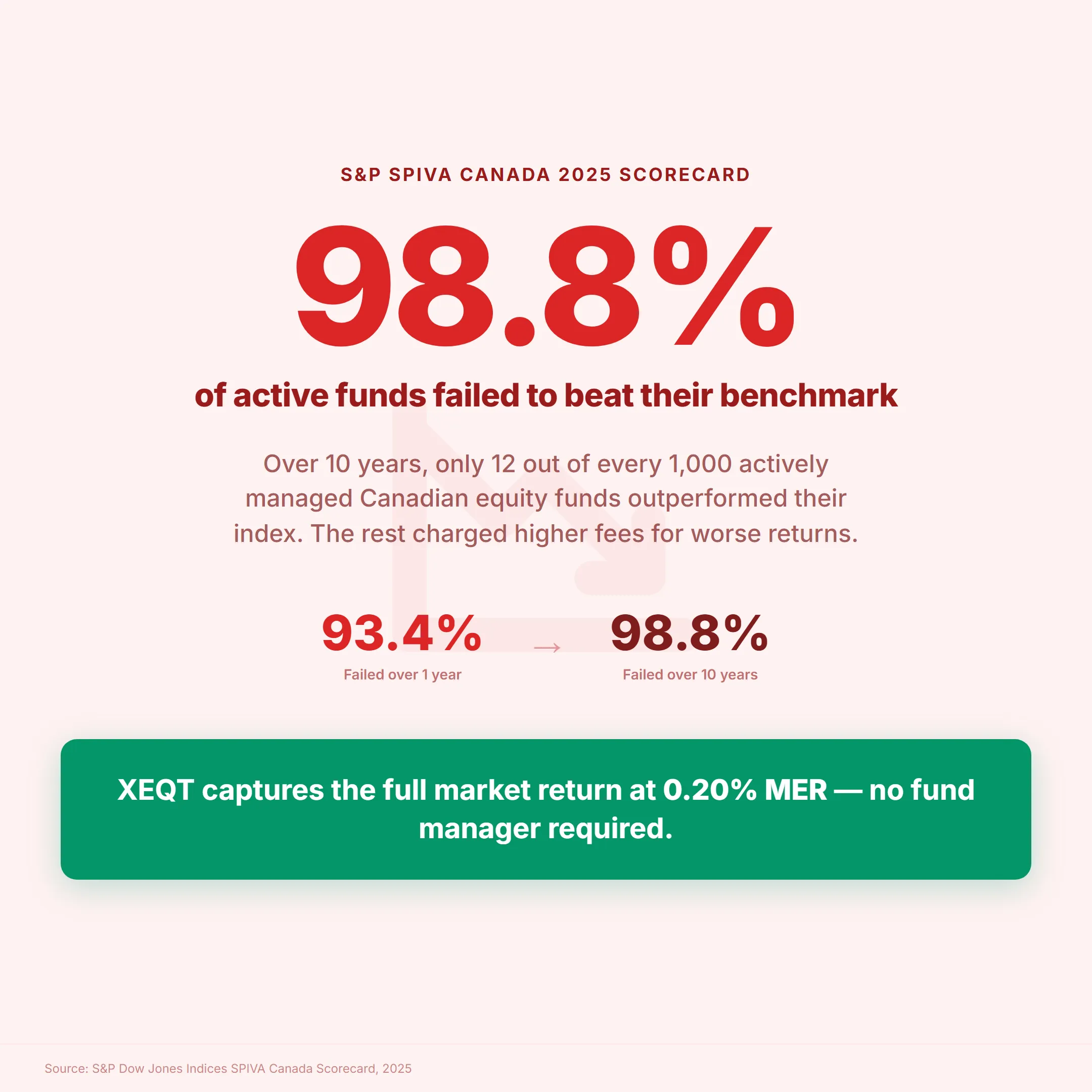

Why Do 98.8% of Active Funds Underperform XEQT?

The S&P SPIVA Canada 2025 scorecard found that 93.4% of actively managed Canadian equity funds underperformed their benchmark over one year, and 98.8% underperformed over 10 years.11 These are not cherry-picked numbers — SPIVA adjusts for survivorship bias (funds that closed due to poor performance) and measures net-of-fee returns.

The primary driver is fees. The average Canadian mutual fund charges a MER above 2% — ten times XEQT’s 0.20%. Over a 30-year compounding horizon, a 1.8% annual fee drag on a $500,000 portfolio costs roughly $300,000 in lost growth over 30 years. The math is unforgiving and cumulative.

The academic backbone supporting XEQT’s approach comes from Lifecycle Investing by Ian Ayres and Barry Nalebuff of Yale University, which argues that younger investors should maximize equity exposure early in life to achieve temporal diversification — spreading market risk across their entire lifespan rather than concentrating it in the years before retirement.12 XEQT’s 100% equity allocation is the practical implementation of this framework.

This does not mean active management never works. It means that identifying the 1.2% of funds that will outperform over the next decade — in advance — is functionally impossible for retail investors. XEQT is a bet on the base rate.

How Does XEQT Compare to Other All-Equity ETFs?

XEQT, VEQT, ZEQT, and HEQT all provide similar global equity exposure at MERs between 0.20% and 0.24% — the differences are marginal, and choosing one matters far less than choosing to invest at all.

| Feature | XEQT | VEQT | ZEQT | HEQT |

|---|---|---|---|---|

| Provider | BlackRock (iShares) | Vanguard | BMO | Global X |

| MER | 0.20% | 0.24% | 0.20% | 0.20% |

| Canada weight | ~25% | ~30% | ~24% | Variable |

| U.S. weight | ~45% | ~40-45% | ~50% | Variable |

| Holdings | ~8,400 | ~13,000 | ~9,000 | Variable |

| Distributions | Quarterly | Annual | Quarterly | Quarterly |

The 0.04% MER difference between XEQT and VEQT amounts to $4 per $10,000 per year — functionally irrelevant. VEQT’s higher Canadian allocation (30% vs 25%) and larger stock count (13,000 vs 8,400) reflect different index coverage but produce negligible performance differences at scale.

For detailed head-to-head analysis, see our XEQT vs VEQT comparison.

Is XEQT Worth Buying in 2026?

XEQT is worth buying in 2026 for any Canadian investor with a 10+ year time horizon and the discipline to hold through drawdowns. The fund’s 0.20% MER, automatic rebalancing, and global diversification solve the mechanical side of investing — and the 98.8% active fund underperformance rate makes it very hard to argue for the alternative.

The fund is not right for everyone. If you’re saving for a home in your FHSA with less than 10 years until purchase, a 30% crash could delay homeownership — consider a balanced allocation instead. If you’ve never held an investment through a major drawdown and aren’t confident you can resist selling, an 80/20 fund like XGRO removes the decision while keeping most of the equity upside. And if you need income, XEQT’s ~2% yield isn’t a distribution strategy. If you’d rather hand off construction entirely and want private market exposure inside a managed wrapper at $30,000+, the Wealthsimple Summit Portfolio is the in-platform alternative — in exchange for a four-layer fee stack and monthly private-sleeve redemption windows.

You can buy XEQT on Wealthsimple with as little as $1 using fractional shares, commission-free. Use our Wealthsimple referral code 9C6DMQ to get a $25 cash bonus on your first deposit. Set up automatic contributions, turn on DRIP, and let the fund do what it was engineered to do. For small automated buys, market orders work fine — but when deploying a larger lump sum, a limit order set just above the ask price protects against spread spikes.

Frequently Asked Questions

What are XEQT’s four underlying ETFs?

XEQT holds four iShares ETFs: ITOT/XTOT (U.S. total market, ~45%), XIC (Canadian equities, ~25%), XEF (international developed markets, ~25%), and XEC (emerging markets, ~5%). Together they provide exposure to over 8,400 individual stocks across 50+ countries.1

Is XEQT hedged or unhedged?

XEQT is fully unhedged. None of its four underlying ETFs use currency hedging, so returns reflect both equity performance and currency movements between the Canadian dollar and foreign currencies. Over long time horizons, currency effects tend to wash out.

Why does XEQT hold 25% Canadian stocks when Canada is only 3% of global markets?

The 25% Canadian allocation is deliberate. Research from Vanguard and PWL Capital suggests a 25-35% home bias is optimal for Canadian investors — it reduces currency volatility and maximizes the Canadian Dividend Tax Credit benefit on eligible dividends from domestic holdings.3

Can XEQT’s rebalancing trigger taxable events in a non-registered account?

No. BlackRock rebalances XEQT internally using daily cash flows — buying whichever underlying ETF is underweight with new money rather than selling overweight holdings. Because no assets are sold inside the fund, no capital gains distributions are triggered. This is one of the structural advantages of the fund-of-funds wrapper.

What is a wrap fee and does XEQT charge one?

XEQT’s 0.20% MER is a wrap fee — it covers both the portfolio management and the underlying ETF costs. Investors do not pay the MERs of ITOT, XIC, XEF, and XEC on top of XEQT’s MER. There is no double-charging.

How much foreign withholding tax does XEQT lose?

XEQT loses approximately 0.20-0.30% annually to foreign withholding taxes. Because XEQT is Canadian-listed, the RRSP’s U.S. withholding tax exemption does not apply — the U.S. withholds 15% on dividends from ITOT/XTOT before the cash enters the Canadian wrapper.9

Should I hold XEQT in my RRSP or TFSA?

Both work well. A TFSA offers completely tax-free growth but foreign withholding taxes are unrecoverable. An RRSP provides a tax deduction on contributions but the RRSP’s U.S. tax treaty exemption does not apply to XEQT’s Canadian wrapper. For most investors, the TFSA’s flexibility makes it the default choice.

What is XEQT’s current dividend yield?

XEQT’s trailing 12-month dividend yield is approximately 2%, with quarterly distributions paid at the end of March, June, September, and December/January. Distributions have grown steadily since inception.8

How does XEQT compare to ZEQT?

XEQT and ZEQT both charge 0.20% MER. ZEQT (BMO) has a slightly higher U.S. tilt (~50% vs ~45%) and lower Canadian allocation (~24% vs ~25%). Performance differences are negligible. The choice typically comes down to provider preference — BlackRock vs BMO.

At what portfolio size should I switch from XEQT to individual ETFs?

Below approximately $250,000, the operational costs of manual rebalancing — trading spreads, tax drag from selling winners, and behavioural drag — typically negate the minor MER savings from holding the underlying ETFs directly.5 Above $500,000, multi-ETF structures may offer meaningful tax optimization through foreign withholding tax recovery.

Sources

Footnotes

BlackRock — iShares Core Equity ETF Portfolio (XEQT) ↩ ↩2 ↩3 ↩4

Vanguard Canada — The case for global equity diversification ↩ ↩2

Based on analysis of trading costs, bid-ask spreads, and rebalancing frequency for Canadian retail portfolios under $250,000, as discussed across PWL Capital research and Canadian investing communities (2025-2026) ↩ ↩2

BlackRock — iShares Core Equity ETF Portfolio Historical Performance ↩

Boomer & Echo — Weekend Reading: Is Stay The Course Helpful Advice Edition ↩

Canadian Portfolio Manager — Foreign Withholding Tax on International Equity ETFs (Justin Bender) ↩ ↩2

The Globe and Mail — Rob Carrick on balanced ETFs (via Reddit) ↩

Ayres, I. & Nalebuff, B. (2010). Lifecycle Investing: A New, Safe, and Audacious Way to Improve the Performance of Your Retirement Portfolio. Yale University. ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.