Just Buy XEQT: Does This Simple Strategy Actually Work?

From Reddit phenomenon to mainstream investment thesis — an analysis of the cultural movement, the academic evidence, and the practical trade-offs of going all-in on a single ETF.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

TL;DR: XEQT returned 126% since 2019 at a 0.20% MER — 13.95% annualized since launch. One ticker, 8,400+ stocks, one decision. The catch: you need a long-term outlook and the discipline to hold through steep crashes — XEQT dropped 30% in 22 trading days during March 2020. Most investors overestimate their tolerance until they watch a third of their portfolio disappear.

- $14.8 billion in assets

- $500/month since inception → ~$60,000 on $40,000 contributed

- 98.8% of active funds underperformed over 10 years

The r/JustBuyXEQT subreddit has grown to over 44,000 members, making it one of the largest single-fund investing communities in the world — but “just buy XEQT” is more than a ticker recommendation. It’s a cultural rebellion against the high-fee mutual fund model that has cost Canadian investors billions in lost compounding, and a bet that radical simplicity beats the complexity the financial industry sells.

What Is the “Just Buy XEQT” Movement?

The “just buy XEQT” movement is a Canadian-born investing philosophy that rejects active management, portfolio complexity, and market timing in favour of a single, globally diversified ETF.1 The phrase originated organically within Reddit’s personal finance communities — r/PersonalFinanceCanada (1.8M members) and r/CanadianInvestor (640K members) — as a shorthand response to investors paralyzed by choice.

The movement has roots in the “Couch Potato” investing philosophy popularized by Dan Bortolotti, which championed low-cost, passive index investing.2 But where the original Couch Potato strategy required buying and rebalancing three to five separate ETFs, XEQT’s launch in August 2019 collapsed that complexity into a single purchase. One ticker. One decision. Done. The cultural momentum eventually produced a dedicated subreddit (r/JustBuyXEQT), educational websites, and mainstream media attention — the community functions as both an educational hub and a psychological anchor, encouraging automated contributions during market crashes rather than panic-selling.

XEQT is “just a magnificent piece of financial market engineering. I’m a huge, huge fan. I often comment XEQT and chill. I just think it’s a great, great product.”3

— Ben Felix, Portfolio Manager at PWL Capital and host of the Rational Reminder podcast

Why Did “Just Buy XEQT” Draw Pushback?

In September 2025, Motley Fool Canada published “Everyone’s Saying, ‘Just Buy XEQT.’ Please Don’t” — arguing that a 100% equity fund is unsuitable for risk-averse investors and that the strategy ignores the need for cash buffers.4 The critique is fair in its specifics (more on that in the “when it fails” section below), but it missed the broader point: the movement is a rebellion against what the Rational Reminder podcast calls “ETF slop” — the explosion of high-fee, behaviourally engineered funds that prioritize asset gathering over investor outcomes.5

As Globe and Mail columnist Rob Carrick noted, even a single diversified ETF can be the foundation of a lifetime’s successful investing6 — and XEQT takes that simplicity to its logical extreme.

What Are You Actually Buying With XEQT — and Does It Deliver?

XEQT is a fund-of-funds managed by BlackRock that holds four underlying iShares ETFs — covering U.S. (~45%), Canadian (~25%), international developed (~25%), and emerging market (~5%) equities — all for a single 0.20% MER. One ticker replaces what used to require buying and rebalancing three to five separate funds. For the full breakdown of how the wrap fee, rebalancing, and foreign withholding tax work under the hood, see our XEQT ETF Review.

The numbers back the thesis. XEQT has delivered approximately 126% cumulative return since its August 2019 inception — a 13.95% CAGR earned through a global pandemic, an inflationary correction, and tariff-driven market volatility.7

What Does $500 Per Month in XEQT Actually Look Like?

An investor contributing $500 per month since XEQT’s August 2019 inception would have contributed approximately $40,000 and hold a portfolio worth roughly $60,000 as of early 2026.8 That’s approximately $20,000 in gains — a 50% return on invested capital — earned by doing nothing except automating a monthly purchase.

The path to that $60,000 included a 30% COVID crash in March 2020, a -10.93% correction in 2022, and a roughly 10% tariff-driven drop in April 2025. In every case, investors who stayed the course recovered — financial planner Robb Engen describes the optimal approach as behaving like an “emotionless robot.”9 These drawdowns are the price of admission for 100% equity exposure, and the core risk the “just buy XEQT” strategy demands you accept.

Wealthsimple is the most popular platform for buying XEQT in Canada — commission-free trades, fractional shares starting at $1, and automatic DRIP reinvestment. Opening a self-directed account takes about five minutes.

Should You Choose XEQT or Wealthsimple Managed Investing?

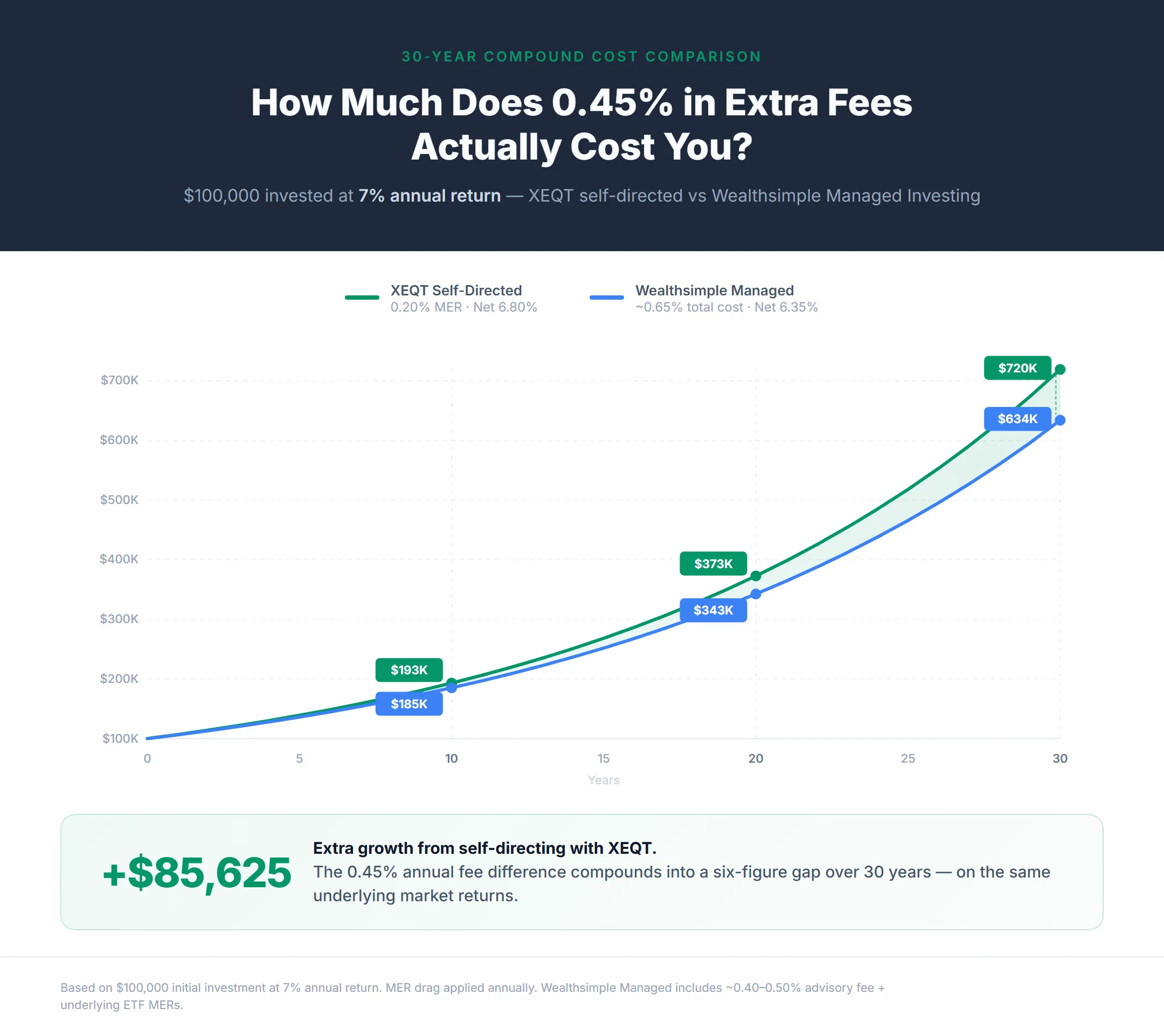

The real decision for most readers of this site isn’t XEQT vs another ETF — it’s XEQT self-directed (0.20% MER) vs Wealthsimple’s managed investing robo-advisor (0.40-0.50% fee + underlying ETF MERs, totaling approximately 0.60-0.70% annually). Both paths lead to a Wealthsimple account.

The math is straightforward. On a $100,000 portfolio:

| Approach | Annual Cost | 30-Year Cost on $100K (7% return) |

|---|---|---|

| XEQT self-directed | $200/year | ~$18,000 in lost growth |

| WS Managed (~0.65%) | $650/year | ~$56,000 in lost growth |

| Difference | $450/year | ~$38,000 |

That $38,000 gap compounds further on larger portfolios. For every $10,000 invested, XEQT saves approximately $40-50 per year compared to the managed option.10

Try it with your own numbers:

Projection assumes constant annual returns compounded monthly. Actual returns vary year to year. Past performance does not guarantee future results.

But here’s what the fee comparison misses: the robo-advisor’s real value is behavioural, not mathematical. Wealthsimple designed the managed portfolio to be invisible. You don’t log in and see a buy button. You don’t watch your holdings drop 30% and wonder if you should sell. For investors who know they’d panic-sell during a crash, the 0.40-0.50% management fee is insurance against their own worst instincts — and it’s dramatically cheaper than the 2%+ charged by bank mutual funds or traditional advisors.

In our experience, if you have the discipline to set up automatic XEQT purchases and ignore your portfolio during drawdowns, self-directed wins on cost. If you can’t, managed investing is the smarter choice. Either way, you’re investing in globally diversified index funds through Wealthsimple.

For accounts of $30,000 or more with a 10+ year horizon, there is now a third path: the Wealthsimple Summit Portfolio blends public ETFs with a 20%-30% private credit and private equity allocation. The trade-off is a four-layer fee stack reaching roughly 1.20%-1.40% all-in once the private sleeve activates, plus 30 to 60 day private redemption windows. Most cost-conscious DIY investors will still prefer XEQT; Summit is the institutional-access lane for the narrower band of investors who specifically want private market exposure inside a managed wrapper.

XEQT or VEQT: Which is Better?

The difference between XEQT (iShares) and VEQT (Vanguard) is negligible for long-term returns — choosing between them is functionally a coin flip. Both are all-equity, globally diversified fund-of-funds targeting nearly identical geographic allocations. XEQT charges 0.20% MER with quarterly dividends; VEQT charges 0.24% (expected to drop to ~0.20% after its November 2025 fee cut) with annual distributions and a slightly higher 30% Canadian tilt vs XEQT’s 25%.

We completely ignore the 0.04% MER difference — it only amounts to $4 per $10,000 per year. The 5% variance in Canadian allocation is unlikely to produce a statistically significant performance difference over a 20+ year horizon. VEQT’s higher stock count (13,000 vs 8,400) reflects different index coverage but the practical diversification benefit is minimal at that scale.

Other all-equity alternatives include ZEQT (BMO, 0.20% MER, higher U.S. tilt at ~50%) and HEQT (Global X, 0.20% MER, variable allocation). For a detailed head-to-head analysis with performance data, see our full XEQT vs VEQT comparison.

When Does the “Just Buy XEQT” Strategy Fail?

The “just buy XEQT” strategy is academically sound for investors with a long time horizon and high risk tolerance — but it fails when either of those conditions isn’t met. This is where the Motley Fool critique and the academic literature converge.

If your time horizon was infinite and your behaviour was perfect, it’s pretty hard to argue against anything other than 100% equity portfolio. The problem is neither of those two things are true for anyone.11

— Dan Bortolotti, Portfolio Manager at PWL Capital and creator of the Canadian Couch Potato blog

Here’s when the strategy breaks down:

You’re close to retirement. Sequence of returns risk is real. If XEQT drops 30% in your first year of retirement and you’re withdrawing to cover living expenses, you lock in losses and deplete shares that can’t recover. Retirees drawing down capital should consider XGRO (80/20 equity/bond) or XBAL (60/40) for built-in volatility cushioning.

You’re saving for a home in your Wealthsimple FHSA with less than 10 years to purchase. A 100% equity allocation in an account with a short, fixed horizon is a gamble. If the market crashes the year before you need your down payment, you could lose a third of it. Consider a balanced allocation for FHSA money you’ll need within 5-7 years. If your strategy is to combine the FHSA with the RRSP Home Buyers’ Plan for a larger down payment, our FHSA + HBP down payment strategy guide covers when to keep that money in cash vs. equity.

You can’t handle drawdowns without selling. This is the biggest risk. XEQT guarantees you will experience 20-30%+ drops at some point. The Lifecycle Investing research by Ayres and Nalebuff supports 100% equity for young investors on mathematical grounds, but the math assumes you don’t panic-sell at the bottom.12 If you’ve never held an investment through a 30% crash and aren’t sure you can, an 80/20 fund like XGRO gives you 80% of the equity upside with significantly smaller drawdowns.

You need income. XEQT yields approximately 2%. That’s not an income strategy. If you’re investing for cash flow, dividend-focused ETFs or a balanced portfolio serve that purpose better.

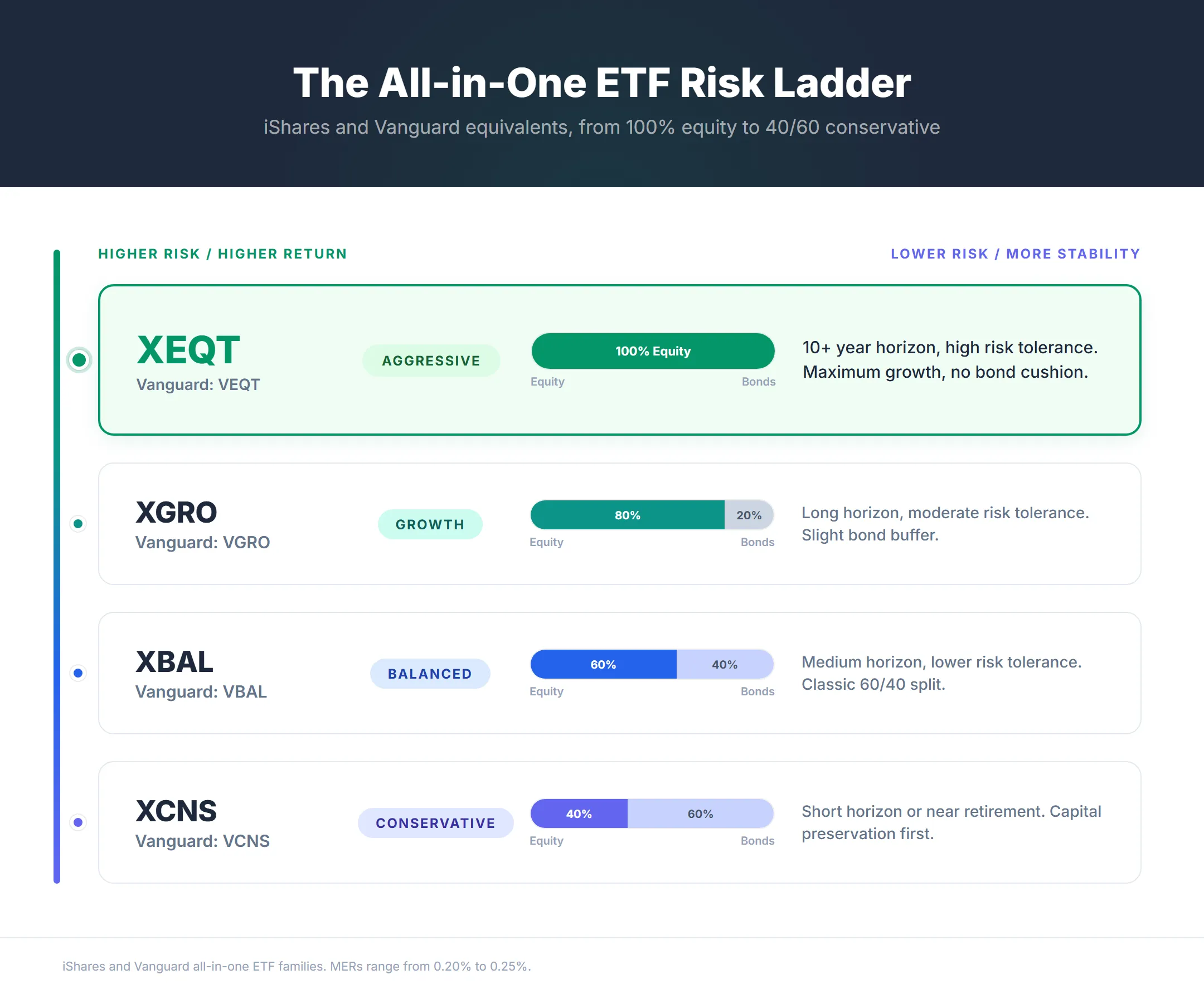

For investors who don’t fit the “just buy XEQT” profile, the same fund-of-funds structure exists at every risk level:

| Risk Tolerance | iShares | Vanguard | Equity / Bond |

|---|---|---|---|

| Aggressive | XEQT | VEQT | 100 / 0 |

| Growth | XGRO | VGRO | 80 / 20 |

| Balanced | XBAL | VBAL | 60 / 40 |

| Conservative | XCNS | VCNS | 40 / 60 |

How Do You Buy XEQT on Wealthsimple?

You can buy XEQT on Wealthsimple with as little as $1 using fractional shares, commission-free, in a Wealthsimple TFSA, Wealthsimple RRSP, FHSA, or non-registered account.

Here’s how:

- Open a Wealthsimple account — Use our Wealthsimple referral code 9C6DMQ to get a $25 cash bonus on your first deposit of $100 or more

- Choose your account type — TFSA is ideal for most investors (tax-free growth). RRSP if you want the tax deduction. FHSA if you’re buying a first home (but be cautious with 100% equity for short timelines)

- Search for XEQT — Type “XEQT” in the search bar on the Trade platform

- Buy fractional or full shares — Enter any dollar amount ($1 minimum). Wealthsimple supports fractional shares, so every dollar goes to work immediately

- Set up automatic deposits — Automate weekly or biweekly contributions. The “just buy XEQT” strategy works best when you remove the decision from the process entirely

A note on taxes: XEQT is a Canadian-listed fund, so the RRSP’s U.S. withholding tax exemption does not apply to the U.S. dividends inside the fund. This creates an unrecoverable tax drag of approximately 0.20-0.30% annually in registered accounts.13 For most investors, the simplicity of a single-fund solution outweighs this cost. Investors with portfolios exceeding $500,000 may want to explore multi-ETF structures for tax optimization — but that’s a Wealthsimple vs Questrade comparison about platform features.

Should You Actually Just Buy XEQT?

For Canadian investors with a decade or more ahead of them and the discipline to stay invested through crashes, yes — the “just buy XEQT” strategy is one of the most efficient wealth-building approaches available. The academic evidence is overwhelming: passive indexing beats active management for the vast majority of investors. XEQT’s 0.20% MER, automatic rebalancing, and global diversification solve the mechanical side of investing.

What the Reddit community gets right is that simplicity is the feature, not a limitation. The fewer decisions you make, the fewer opportunities you have to make the wrong one.

What they sometimes miss is that 100% equity isn’t for everyone. If your timeline is short, your risk tolerance is low, or you need income, the same fund-of-funds structure exists at every risk level — XGRO, XBAL, XCNS.

The strategy works. The question is whether it works for you.

Frequently Asked Questions

Is XEQT a good long-term buy?

For investors with a 10+ year horizon, XEQT has strong fundamentals: 13.95% annualized since its August 2019 inception, a 0.20% MER, and automatic rebalancing across over 8,400 global stocks. The S&P SPIVA 2025 scorecard shows 98.8% of actively managed Canadian funds underperformed their benchmark over 10 years.14

Why is XEQT so cheap?

XEQT trades at approximately $35-40 per share because BlackRock priced it at a low NAV at inception to maximize accessibility. The share price has no bearing on fund quality — what matters is the total return, which has been 126% cumulative since August 2019.

Is XEQT too diversified?

XEQT holds over 8,400 stocks, but diversification is a feature, not a bug. Global diversification protects against regional downturns — during the 2025 U.S. tariff volatility, XEQT’s international holdings offset some of the concentrated U.S. risk that S&P 500-only portfolios faced. For a full analysis, see our XEQT vs VFV comparison.

How much does XEQT return each year?

XEQT’s annual returns since inception: 2020 (11.71%), 2021 (19.57%), 2022 (-10.93%), 2023 (17.05%), 2024 (24.67%), 2025 (20.45%). The annualized return since the August 2019 launch is approximately 13.95%.

What is XEQT’s MER?

XEQT’s MER is 0.20%, with a management fee of 0.17% following a December 2025 reduction by BlackRock.15 This is a wrap fee — investors don’t pay the underlying ETF MERs on top, so there’s no double-charging.

Can I buy fractional shares of XEQT?

Yes. Wealthsimple supports fractional share purchases of XEQT starting at $1. This means you can invest any dollar amount immediately without waiting to afford a full share, maximizing your time in the market.

Should I switch from VEQT to XEQT after the 2025 fee cuts?

With both funds now charging a 0.17% management fee, there is no fee-based reason to switch. VEQT and XEQT overlap by approximately 90% in underlying holdings. In a taxable account, selling VEQT to buy XEQT triggers capital gains for effectively zero benefit — keep whichever you already own.

What happens to XEQT if the US market crashes?

XEQT allocates approximately 45% to U.S. stocks, so a U.S. crash would impact the fund. However, the remaining 55% in Canadian, international developed, and emerging market stocks provides a buffer. During the 2025 tariff-induced volatility, XEQT’s global diversification mitigated some of the concentrated U.S. risk.

Does XEQT pay dividends?

XEQT pays quarterly distributions with a trailing yield of approximately 2%. The dividend growth rate has averaged 9.06% over three years.16 BlackRock designed it primarily for capital growth — if you need higher yield, consider dividend-focused ETFs.

Is a TFSA or RRSP better for the “just buy XEQT” strategy?

A TFSA is the default choice for most investors — all growth is completely tax-free, and withdrawals don’t affect government benefits. The RRSP’s U.S. tax treaty exemption does not apply to XEQT because it’s a Canadian-listed ETF, so neither account has a foreign withholding tax advantage. Choose the TFSA unless you’re in a high tax bracket and need the RRSP deduction. For a side-by-side walkthrough that also weighs the FHSA, see our TFSA vs RRSP vs FHSA decision guide.

What’s the difference between XEQT and a robo-advisor?

XEQT charges 0.20% MER. Wealthsimple’s robo-advisor charges 0.40-0.50% on top of underlying ETF fees, totaling approximately 0.60-0.70% annually. Over 30 years, that 0.40-0.50% difference compounds into tens of thousands of dollars. The trade-off: robo-advisors prevent emotional tampering during crashes.

Should I put all my money in XEQT?

It depends on your time horizon and risk tolerance. XEQT dropped 30% during the March 2020 COVID crash and lost 10.93% in 2022. If you can stomach those drawdowns without selling, a 100% XEQT allocation is academically sound for a 10+ year horizon. If not, consider XGRO (80/20) or XBAL (60/40) for built-in bond cushioning.

Sources

Footnotes

Vanguard Canada — The case for global equity diversification ↩

Rational Reminder — Episode 343: How to Choose an Asset Allocation ↩

Motley Fool Canada — “Everyone’s Saying, ‘Just Buy XEQT.’ Please Don’t” (September 2025) ↩

The Globe and Mail — Rob Carrick on balanced ETFs (via Reddit) ↩

BlackRock — iShares Core Equity ETF Portfolio Historical Performance ↩

Estimated using BlackRock’s published annual total returns (2020-2025) with monthly contributions of $500 starting August 2019. Model assumes returns distributed evenly across months within each year. Cross-validated against independent DCA tracker justbuyxeqt.ca (end-of-2024 values within 2.5%). Actual results may vary based on exact purchase dates and reinvestment timing. ↩

Boomer & Echo — Weekend Reading: Is Stay The Course Helpful Advice Edition ↩

Based on comparison of published fee schedules: Wealthsimple Trade (0% commission + XEQT 0.20% MER) vs Wealthsimple Invest (0.40-0.50% management fee + underlying ETF MERs) as of March 2026 ↩

Rational Reminder — Episode 343: How to Choose an Asset Allocation ↩

Ayres, I. & Nalebuff, B. (2010). Lifecycle Investing: A New, Safe, and Audacious Way to Improve the Performance of Your Retirement Portfolio. Yale University. ↩

Canadian Portfolio Manager — Foreign Withholding Tax on International Equity ETFs (Justin Bender) ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.