Wealthsimple Summit Portfolio Review (2026): Institutional Private Markets at $30K

Wealthsimple Summit opens LGT private equity and Sagard private credit to Canadian retail investors at $30,000 — institutional managers that traditionally required accredited-investor status and $1M+ LP minimums. After June 2026, those private holdings unify into a single Private Market Fund accessible standalone or via Summit's 30% private sleeve.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

The Bottom Line: Wealthsimple Summit Portfolio gives Canadian retail investors access to LGT Capital Partners and Sagard Holdings — institutional managers behind a combined $137 billion in alternative assets — at a $30,000 entry threshold with monthly redemption windows instead of the 7-to-12-year lockups of traditional accredited-investor LPs.12

- $30,000 investable-asset entry + $50,000 liquid-asset suitability check (no accredited-investor status required)

- LGT Capital Partners runs the private equity sleeve ($110B AUM, 700+ institutional clients)

- Sagard Holdings runs the private credit sleeve (CPPIB-anchored, $27B AUM)

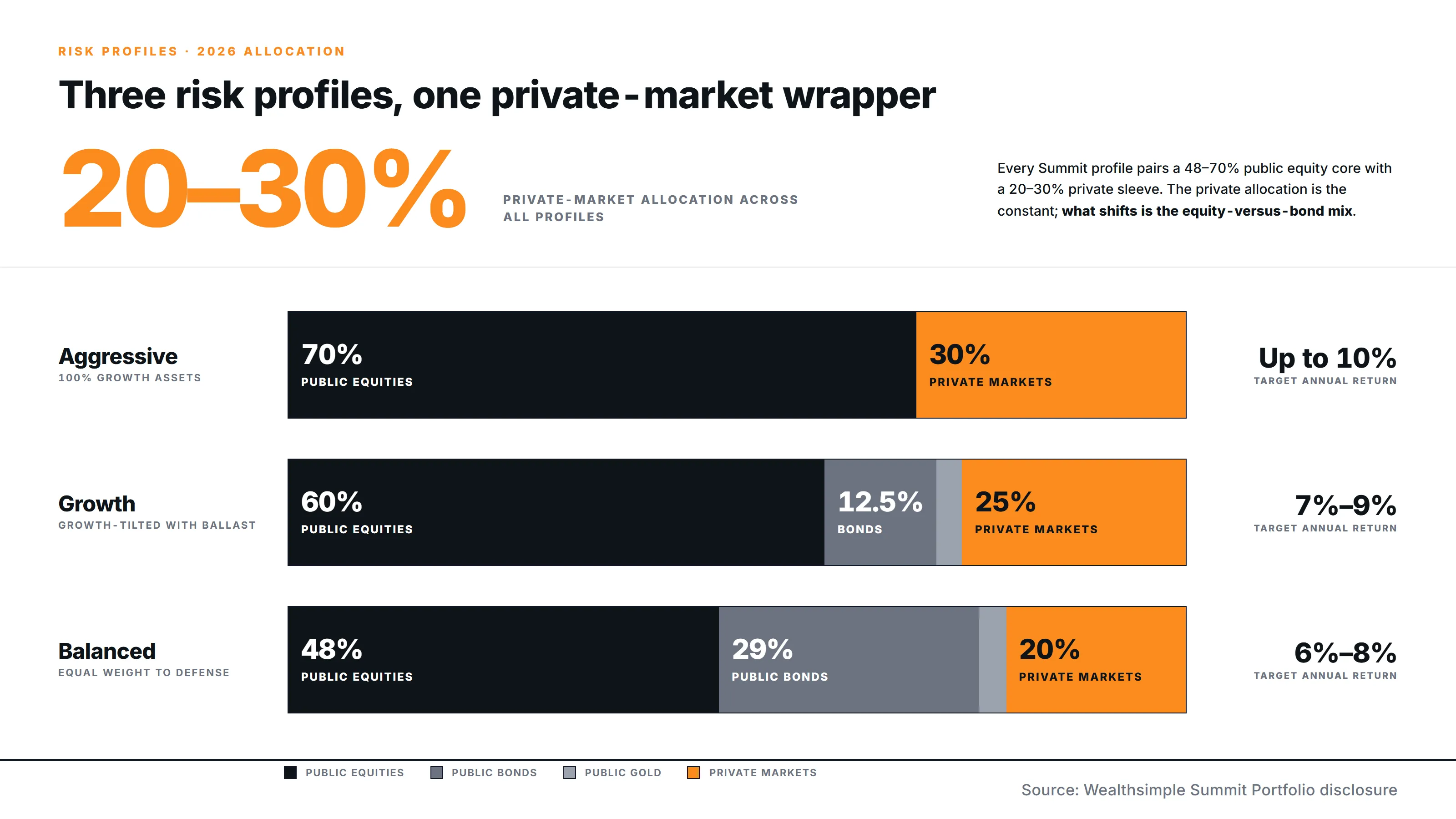

- Three risk profiles: Aggressive (30% private), Growth (25%), Balanced (20%)

- From June 1, 2026, private holdings unify into a single Private Market Fund accessible standalone or via Summit’s private sleeve3

What’s Inside the Wealthsimple Summit Portfolio’s Architecture in 2026?

The Wealthsimple Summit Portfolio is a managed account that blends public ETFs with a private allocation across credit, private equity, and (from June 2026) private infrastructure, available to Wealthsimple Core, Premium, and Generation clients who pass a suitability assessment with at least $50,000 in liquid assets and meet the $30,000 investable-asset client qualification listed on the Summit product page.41 Three risk profiles map to three different public-private splits.

| Profile | Public Equities | Public Bonds | Public Gold | Private Markets | Targeted Annual Return |

|---|---|---|---|---|---|

| Aggressive | 70% | — | — | 30% | Up to 10% |

| Growth | 60% | 12.5% | 2.5% | 25% | 7% to 9% |

| Balanced | 48% | 29% | 3% | 20% | 6% to 8% |

Aggressive is the only profile with no public fixed income; the 30% private allocation is the sole non-equity diversifier. Balanced is the only profile where traditional public bonds (32%) outweigh the private allocation (20%).

The private sleeve does not invest until the account crosses $10,000 in net deposits. Below that threshold, contributed capital sits 100% in public ETFs. Once the account exceeds $10,000, Wealthsimple’s rebalancing engine deploys the appropriate target percentage into the private sleeve during the next monthly subscription window. The deployment is not instant: the private cash sits in a high-interest savings proxy until the next window opens, which means an investor depositing $50,000 on the first business day after a window closes will hold the private-allocation cash for up to four weeks before deployment.1

The eligibility numbers are not a single threshold. The marketing page references $30,000 in investable assets, the Help Centre adds a $50,000 minimum-liquid-assets check, and the activation logic uses $10,000 in net deposits. The $50,000 figure reads as a Canadian KYC/suitability risk-capacity gate, not a deposit floor: clients with $30,000 in Wealthsimple plus material liquid assets elsewhere can clear it. The Wealthsimple Core, Premium, and Generation tiers each have distinct qualification thresholds and advisory rates that determine the Summit advisory layer cost.

Summit’s 70/30, 72.5/27.5, and 80/20 public-private splits sit a tier below the allocation target the world’s largest asset manager now positions as the forward default.

The future standard portfolio may look more like 50/30/20—stocks, bonds, and private assets like real estate, infrastructure, and private credit.5

— Larry Fink, Chairman and CEO of BlackRock

The Fink framing matters less for what it predicts than for what it codifies: institutional allocators are no longer treating a meaningful private sleeve as exotic. Summit is a retail-accessible vehicle inside that broader migration, with the public sleeve doing the liquidity work and the private sleeve doing the illiquidity-premium work.

Sign-up bonus applied with our link.

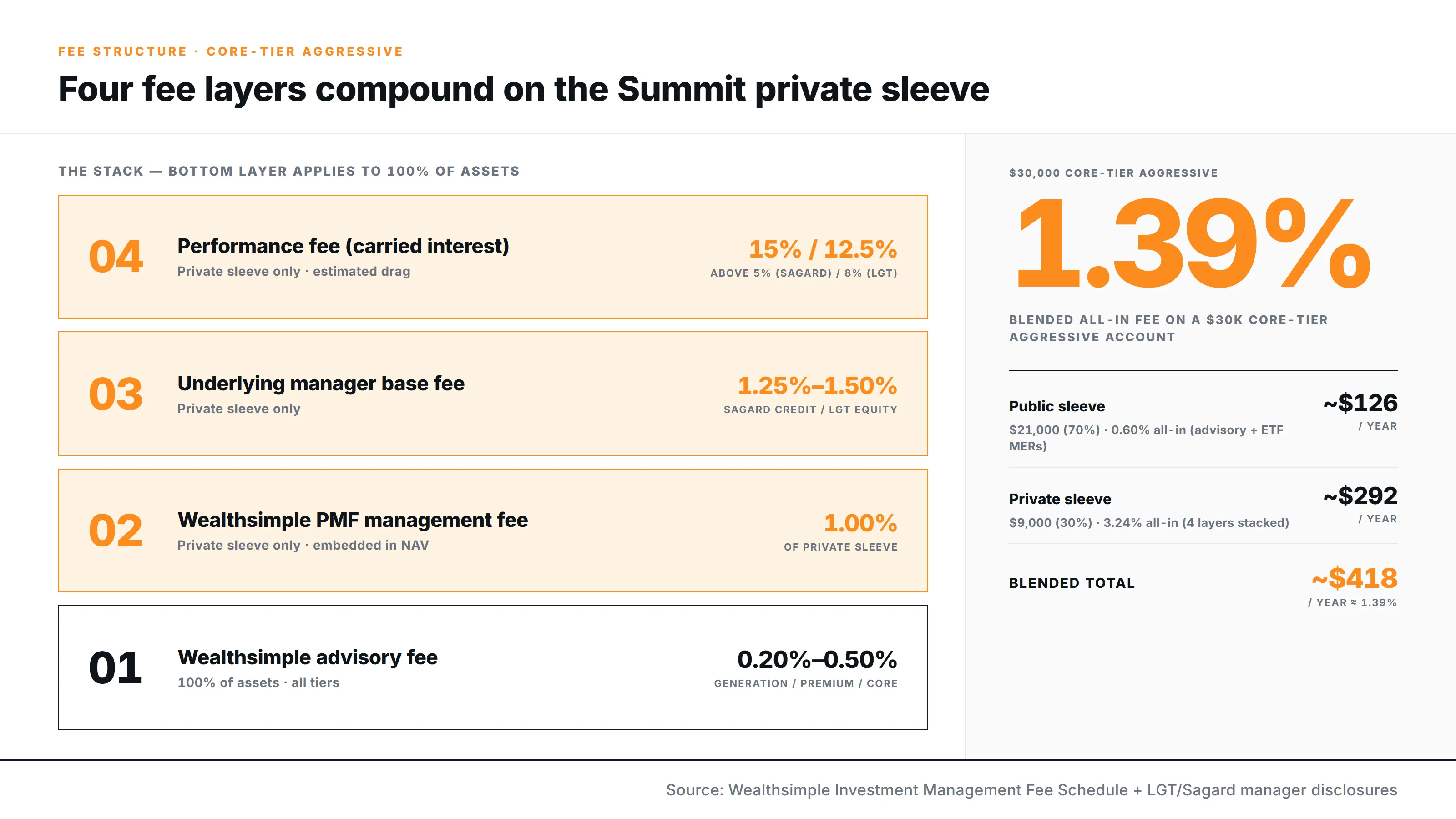

What Are the Costs in Wealthsimple Summit Portfolio’s Four-Layer Fee Stack?

The Wealthsimple Summit Portfolio’s underlying carry rates sit below the institutional 2-and-20 standard, but the fee stack reaches four layers once the private sleeve activates above $10,000 in net deposits.67 The first layer applies to all assets and varies by client tier per the published Investment Management Fee Schedule.8 Layers 2 through 4 apply only to the private sleeve.

| Layer | Where it applies | Rate |

|---|---|---|

| Wealthsimple advisory fee | 100% of assets | 0.50% / 0.40% / 0.20%–0.40% (Core / Premium / Generation) |

| Wealthsimple PMF management fee | Private sleeve only | 1.00% (embedded in NAV) |

| Underlying manager base fee | Private sleeve only | 1.25% (Sagard credit) / 1.50% (LGT equity) |

| Performance fee (carried interest) | Private sleeve only | 15% above 5% hurdle (Sagard); 12.5% above 8% (LGT) |

Public ETF MERs add another roughly 0.10% on the public sleeve (Wealthsimple’s own assumption in the Summit projection disclosure). When benchmarked against the major retail-accessible private market funds, Summit’s underlying carry structure is investor-friendly relative to industry standards.9

| Fund / Manager | Asset Class | Base Mgmt Fee | Performance Fee | Hurdle Rate |

|---|---|---|---|---|

| Institutional Standard | PE / PC | 1.50%–2.00% | 20.0% | 8.0% |

| Blackstone (BXPE) | Private Equity | 1.25% | 12.5% | 5.0% |

| Apollo S3 | Private Markets | 1.25% | 12.5% | 5.0% |

| KKR (K-Prime) | Private Equity | 1.25% | 15.0% | 5.0% |

| Ninepoint Monroe | Private Debt | 1.55% | 20.0% | 7.0% |

| Wealthsimple (LGT) | Private Equity | 1.50% | 12.5% | 8.0% |

| Wealthsimple (Sagard) | Private Credit | 1.25%–1.40% | 15.0% | 5.0% |

The LGT line is the standout: an 8% hurdle rate combined with a compressed 12.5% carry. Earning a 5% return in an environment where risk-free, three-month Treasury bills yield roughly 4.3% requires no genuine alpha — which is why BXPE, Apollo S3, and KKR K-Prime standardized at 5%. Securing an 8% hurdle for the LGT sleeve means the manager must deliver true equity-like premiums before extracting performance fees. Sagard’s 15% carry on the private credit sleeve sits noticeably below the 20% performance fee charged by Canadian competitors like Ninepoint Monroe, leaving more of the generated yield with the end investor.

How the fees stack on a $30,000 Core-tier Summit Aggressive account

A 70% public, 30% private split applies. The public sleeve carries the 0.50% advisory fee plus the ~0.10% ETF MER. The private sleeve carries the 0.50% advisory fee plus the 1.00% PMF management fee plus an average ~1.375% manager base fee plus a performance fee that varies with returns.

At a 9% gross blended return, the Sagard sleeve clears the 5% hurdle by 4 percentage points, capturing a 0.60% performance fee on its half of the private sleeve. The LGT sleeve clears the 8% hurdle by 1 point, capturing 0.125%. Average performance drag across the private sleeve: ~0.36 percentage points.

| Sleeve | Allocation | Total fee on the sleeve | Contribution to blended fee |

|---|---|---|---|

| Public ETFs | $21,000 | 0.60% | 0.42% |

| Private (incl. carry) | $9,000 | 3.24% | 0.97% |

| Recommended pick. Blended all-in fee | $30,000 | — | ~1.39% |

That blended ~1.39% is roughly three times the 0.44% rate Wealthsimple uses in its 47% richer marketing illustration. At a $100,000 Premium tier with the same Aggressive mix, the blended fee compresses to roughly 1.29%. At a $500,000 Generation tier (assumed 0.30% effective advisory rate), the blended fee compresses to roughly 1.19%.

Why Is the Wealthsimple Summit Portfolio 47% Richer Than Bank Mutual Funds?

The math is internally consistent with Wealthsimple’s selected inputs — 0.44% Summit fee, 1.85% legacy mutual fund fee, $10,000 invested at 10% gross over 30 years — and reproduces the headline 47% terminal-wealth gap.6 The honest reframe is the comparison baseline: a 1.85% bank-channel mutual fund is a dying product, not the alternative most cost-conscious retail investors weigh today.

The disclosure inputs are explicit:

- Initial investment: $10,000

- Time horizon: 30 years

- Assumed gross pre-fee return: 10% annualized

- Summit assumed annual management fee: 0.44%

- Comparison “leading mutual fund” annual management fee: 1.85%

- Compounding: monthly

- Excluded from the model: capital gains taxes, trading costs, loads, transaction fees, account-level fees

Under the simplification that the net annual return equals (gross return − fee), the terminal-wealth gap between a 9.56% net portfolio (10% gross less 0.44%) and an 8.15% net portfolio (10% gross less 1.85%) over 30 years is approximately 47.5%.

How the comparison lands against alternatives

The 0.44% input is the public-sleeve advisory rate, not Summit’s all-in cost. Once the private sleeve activates, the actual all-in fee runs 1.19% to 1.39% depending on tier and risk profile (above). Wealthsimple’s own Summit graph disclosure assumes a 1% fee for the private sleeve and a 0.10% average ETF MER for projections — even Wealthsimple’s internal modeling uses a higher number than the marketing 0.44%.7

Three reference points matter for how Summit positions against actual alternatives:

- Against a self-directed ETF strategy. Substitute Summit’s realistic blended fee of ~1.20% for the 0.44%, and substitute XEQT’s 0.20% MER for the 1.85% baseline, then run the same 30-year compounding model. The gap reverses sign — a DIY ETF strategy ends up roughly 35% to 40% ahead of Summit on cost alone. Summit’s value proposition is not low-fee public-market beta. The cost-driven case for XEQT is covered in our XEQT ETF review.

- Against accredited-investor limited partnerships. Traditional private equity and private credit access in Canada requires clearing the Accredited Investor test under National Instrument 45-106 ($200K individual or $300K spousal income, or $1M in financial assets, or $5M in net assets), with $250K to $5M minimum commitments, T5013 partnership tax slips that arrive late in tax season, and 7-to-12-year lockups with unpredictable capital calls.2 Summit replaces all of that with a $30,000 entry, T3 trust slips, monthly redemption windows, and a fully funded evergreen structure that mitigates the J-curve.

- Against retail interval funds. Mackenzie Northleaf Private Credit ($5,000-$25,000 minimum), Ninepoint Monroe U.S. Private Debt ($25,000 USD with early-redemption penalties), and BMO Partners Group Private Markets ($25,000 minimum) are the comparable retail vehicles.10 Summit’s hurdle rates (LGT’s 8%) and integrated multi-asset allocation framework offer institutional-grade pricing absent in single-asset interval funds.

What about the 18-year backtest?

The Summit page also surfaces a hypothetical historical return chart from September 2006 to December 2024. The chart is not a Wealthsimple performance history; Summit and its specific Sagard and LGT sleeves did not exist before 2023. The chart is a backtest applied to Preqin private market indices. Wealthsimple’s own graph disclosure states: “previous returns for the Private Market Fund are based on private asset indices that aggregate performance across multiple managers and may differ materially from the performance of the specific managers we use.”7

Non-parametric estimation reveals structural reporting biases that artificially boost private equity fund IRRs by an average of 3% per annum.11

— Simon Hayley and Onur Sefiloglu, Bayes Business School, City University of London

The finding applies industry-wide to Preqin-style indices, including the one underlying Wealthsimple’s Summit chart. Brav, Lakan, and Yafeh’s broader analysis of private equity performance documents that commercial private market databases omit small funds and poor performers, with failing managers ceasing to report in order to protect future fundraises.12 Treat the 18-year Summit chart as asset-class history under index conditions, not as a guide to what Wealthsimple’s specific managers would have delivered. The trailing returns from the live Sagard and LGT sleeves (covered in the FAQ below) are the more direct evidence base.

How Does Wealthsimple Summit Portfolio Liquidity Compare to 7-Year LP Lockups?

The Wealthsimple Summit Portfolio public sleeve assets settle in 2 to 3 business days. Private sleeve redemptions process in monthly windows capped at 5% of fund NAV with 30 to 60 day payouts — a liquidity profile vastly superior to the 7-to-12-year lockups of traditional accredited-investor limited partnerships, but more restrictive than the T+1 settlement of public ETFs.3 The 5% gating mechanism is a protective feature designed to prevent forced liquidations of underlying illiquid assets during market panics.13

| Dimension | Public sleeve | Private sleeve | Public ETF (XEQT/VGRO benchmark) | Traditional LP (accredited) |

|---|---|---|---|---|

| Redemption frequency | Daily; standard settlement | Monthly windows, 30 to 60 day payout | Daily during market hours | None — capital locked 7 to 12 years |

| Settlement timeline | T+1 to T+3 | T+30 to T+60 | T+1 | End of fund life |

| Formal gating cap | None | 5% of fund NAV per month; pro-rata beyond cap | None | N/A — no redemptions exist |

| Stress fallback | None | Manager may issue 95% promissory note, up to 2-year maturity | None (price gaps, spreads widen) | Secondary-market discount sale |

The 5% cap is an industry-standard semi-liquid mechanism. Blackstone’s BREIT vehicle in late 2022 limited withdrawals to 2% of NAV per month and 5% per quarter, fulfilling excess requests pro rata for nearly a year after redemption requests breached the cap.3 Romspen Mortgage Investment Fund, a Canadian private debt vehicle, suspended redemptions outright during a 2022 stress period. Both are reminders that the underlying assets are fundamentally illiquid; the wrapper smooths access without changing that.

The denominator effect during a crash

Split-liquidity rebalancing during a crisis produces what institutional investors call the denominator effect. If public equities drop 30% in a month, the public sleeve marks down in real time while the private sleeve appears artificially stable because private NAVs are determined by lagged appraisals, not market prices. The portfolio becomes structurally over-allocated to illiquid private assets relative to its target risk profile. If the investor requests a withdrawal at that moment, Wealthsimple’s engine sells the depressed public sleeve to fund the cash payout — leaving the illiquid (and now disproportionate) private allocation intact. This is a structural feature of any blended public-private wrapper and not unique to Summit. Investors should size the private allocation as 10-year capital, not contingency reserves.

Summit’s monthly redemption window and 5%-of-NAV-per-month gate are wrapper-level mechanics — distinct from the underlying fund’s own redemption math, which uses quarterly windows and a 5%-per-quarter gate. For fund-level redemption mechanics, sector exposures, sleeve-level fee stacks, and the standalone-vs-Summit access decision, see our Wealthsimple Private Market Fund review.

What Does the 2026 PMF Migration Mean for Wealthsimple Summit Holders?

On June 1, 2026, Wealthsimple consolidates standalone Private Equity and Private Credit holdings into a unified Private Market Fund (PMF) with a target allocation of 40% private equity, 35% private infrastructure, and 25% private credit.3 The infrastructure sleeve, managed by IFM Investors, is new exposure — adding CPI-linked cash flows from toll roads, regulated utilities, renewable energy, and data centers as a structural inflation hedge.14

We delivered solid financial results during the quarter, underpinned by our strong balance sheet and growing cash flow that is highly contracted and indexed to inflation.15

— Sam Pollock, CEO of Brookfield Infrastructure

The Brookfield commentary on contracted, inflation-indexed cash flows describes the same structural feature IFM is bringing into the Summit private sleeve through PMF: toll roads, regulated utilities, and contracted renewables produce revenues that step up with CPI by contract or regulatory formula, not by market sentiment.

Three friction points apply specifically to Summit holders during the transition:

1. Tax friction in non-registered accounts. We verified that the Canada Revenue Agency treats the exchange of standalone fund units for PMF units as a disposition at fair market value, which triggers immediate capital gains or losses for the 2026 fiscal year — even though no cash leaves the account. Investors holding gains in non-registered accounts owe tax on a transaction they did not initiate. RRSP and TFSA accounts are unaffected because registered structures shield the exchange from CRA disposition rules.

2. Fee reset (with grandfather rebate). The new PMF carries a standardized 1.00% Wealthsimple fee at the fund level, plus underlying manager fees and performance fees across all three asset classes. A “High Value Customer Fee Rebate” automatically offsets the new top-layer Wealthsimple fee for legacy investors on their original balances, preserving the prior fee structure. The rebate does not offset the newly aggregated underlying performance fees.

3. Distribution cessation. The standalone Private Credit fund pays a quarterly distribution; the unified PMF reflects returns in NAV growth instead of cash distributions. The final Private Credit distribution covers the period ending May 30, 2026 and pays out June 30, 2026.3 Holders who were drawing on the 9.6% distribution yield as cash flow need to plan for the change.

The migration is not all friction. Legacy Private Equity holders gain a meaningful liquidity improvement: the PMF’s roughly 2.5-month redemption window collapses what was a 6- to 9-month exit lag for the standalone Private Equity fund, materially shortening cashflow planning horizons inside TFSA and non-registered accounts.3

Migration timeline:

- 2025

October — PMF redemption schedule begins

Monthly redemption windows open for the new Private Market Fund structure.

- 2026

May 20 — Private Equity opt-out deadline

Final date for certain Private Equity fund holders to elect out of the migration.

- 2026

June 1 — Automatic migration to PMF

Eligible private-market clients are migrated to the unified Private Market Fund.

- 2026

June 30 — Final Private Credit distribution paid

Last quarterly cash distribution from the standalone Private Credit fund.

- 2026

2026 tax year — Disposition treatment

Non-registered migration treated as disposition at fair market value for CRA purposes.

For Quebec residents in non-registered accounts, the disposition is reported on parallel federal and provincial slips: T3 federally, RL-3 provincially (and RL-15 if any sleeve uses partnership structure). Combined federal-Quebec marginal tax rates exceeding 53% apply to the interest-income component from the private credit allocation. The broader tax architecture at the Generation tier — including Tax Pro inclusion and its Quebec exclusion — is covered in our Wealthsimple Generation review.

After June 1, two access routes to the Private Market Fund coexist: keep Summit at its 30% private sleeve, or open a standalone Private Market Fund account with 100% private exposure. The standalone route holds the full 40% private equity, 35% private infrastructure, 25% private credit allocation undiluted; Summit caps that same allocation at 30% of portfolio assets and pads the other 70% with public ETFs. The decision is whether the public-ETF buffer is part of the goal or a dilution of the goal.

The cost on the other side of the migration is loss of asset-class targeting. Holders who chose the standalone Private Credit fund specifically to avoid Private Equity’s longer redemption profile find their exposure comingled by default — and per Wealthsimple’s published migration mechanics, only legacy Private Equity holders received an opt-out window into the new structure.3

How Does Wealthsimple Summit Allocate Between LGT and Sagard Inside the Wrapper?

Wealthsimple Summit splits the 20%-30% private sleeve between two institutional managers — LGT Capital Partners runs the private equity allocation, Sagard Holdings runs the private credit allocation — chosen for sleeve-specific fit, not interchangeably. The allocation logic matters because it directly affects how the wrapper behaves under stress and where Summit’s risk concentration actually sits.

Why LGT runs the private equity sleeve

LGT was selected for the PE sleeve specifically because its strategy concentrates on secondaries and direct co-investments rather than primary fund commitments. Primary PE funds carry a pronounced J-curve: capital is drawn down slowly and early returns are mathematically negative due to immediate management fees dragging against unrealized asset values. For a retail wrapper that needs to mark NAV monthly and process redemption requests within 30 to 60 days, a J-curve drag at fund inception would distort early-year client outcomes. Secondary purchases of mature, cash-flowing LP stakes (often at NAV discounts) and direct co-investments alongside established GPs sidestep that drag and accelerate return-of-capital pacing — the structural feature that makes the PE allocation viable inside a monthly-window wrapper at all.

A second wrapper-level signal: LGT sits entirely outside the Power Corporation ecosystem (privately owned by the Princely Family of Liechtenstein), providing a third-party diversification check on Summit’s private allocation that Sagard alone could not provide given the related-party disclosure below.

Why Sagard runs the private credit sleeve

Sagard’s PC strategy concentrates on first-lien, senior-secured loans to middle-market companies at floating rates. Two features fit Summit’s wrapper specifically: first-lien position sits at the top of the capital structure (highest claim in default scenarios), and floating-rate yield adjusts with central bank base rates. Combined, this produces a duration profile that hedges against the same rate moves that would compress the public bond sleeve in the rest of the Summit portfolio — Sagard’s PC inside Summit isn’t competing with the public fixed-income allocation, it’s offsetting its duration risk.

Sagard cleared independent institutional diligence by CPP Investments and other sovereign-grade limited partners before being selected for retail wrapper exposure, which substantively addresses the related-party concern below — Sagard would have cleared institutional selection on its standalone credibility absent the Wealthsimple link.

Disclosed related-party material conflict of interest

Power Corporation of Canada is the controlling shareholder of both Wealthsimple (via Power Financial and IGM Financial) and Sagard, and Wealthsimple’s Relationship Disclosure Information filings and Sagard’s RDI both classify the arrangement as a related-party material conflict of interest.1617 The Ontario Securities Commission defines a material conflict as one where a registrant has a financial incentive to recommend securities of a related issuer over potentially superior third-party alternatives. Wealthsimple and Sagard maintain separate legal entities and assert arm’s length due diligence, and the PMF brochure further discloses that Wealthsimple may earn additional economics through fee spreads and rebates negotiated with third-party managers — disclosed mitigants, not absolute prohibitions.

For the underlying manager track records — LGT’s secondaries deal flow and Preqin top-quartile rankings, Sagard Credit Partners II’s reported gross/net IRRs, leadership pedigree, and historical AUM — see our Wealthsimple Private Market Fund review, which is the primary home for fund-level due diligence across the cluster.

How Does Wealthsimple Summit Compare to Wealthsimple Classic Managed Investing?

Wealthsimple Classic Managed Portfolio is the all-public-ETF managed product with no private market exposure, no monthly windows, no gating, and a single fee layer. Summit adds a 20%-30% private allocation across LGT private equity and Sagard private credit, monthly redemption windows, three additional fee layers, and a hypothetical illiquidity premium.

| Dimension | Wealthsimple Classic Managed | Wealthsimple Summit Portfolio |

|---|---|---|

| Eligibility | $1+, all tiers | $30K investable + $50K liquid + $10K activation, all tiers |

| Asset mix | 100% public ETFs (equities/bonds, by risk profile) | 70%–80% public ETFs + 20%–30% private allocation |

| Daily liquidity | Yes, T+1 to T+3 | Public sleeve only; private sleeve T+30 to T+60 |

| Fee structure | Single advisory fee (0.50%/0.40%/0.20%–0.40%) | 4-layer stack (advisory + 1% PMF + 1.25%–1.50% manager + carry) |

| Realistic blended cost | 0.30%–0.60% | 1.20%–1.40% before performance fees |

How to choose between Classic Managed and Summit

Wealthsimple Summit Portfolio: Summit fits when & Look elsewhere when

Summit fits when

- 1. 10+ year horizon with no realistic chance of needing the locked capital before each monthly window opens

- 2. Portfolio large enough that the 20%–30% private allocation adds genuine diversification rather than asset-complexity overhead

- 3. Want institutional-grade LGT and Sagard access without the accredited-investor paperwork or seven-figure LP minimums

- 4. Generation tier ($500K+) where the 0.20%–0.40% advisory layer compresses the fee-stack disadvantage to roughly 1.19% blended

- 5. Holding the allocation in registered accounts (RRSP/TFSA) where phantom-distribution and forced-disposition tax frictions are shielded

Look elsewhere when

- 1. Need daily liquidity and simple tax slips Wealthsimple Classic Managed delivers 100% public ETFs with a single advisory layer and T+1 to T+3 settlement.

- 2. Want 100% private exposure (not a 30% diversifier) Standalone Private Market Fund delivers undiluted 40% PE / 35% Infrastructure / 25% PC without the public-ETF buffer.

- 3. Cost-driven and would otherwise build a self-directed ETF portfolio XEQT or VEQT at a 0.20% MER ends roughly 35%–40% ahead of Summit on terminal wealth across 30 years.

- 4. Below the $30K investable + $50K liquid suitability thresholds Account does not qualify for the Summit product until both gates clear; classic managed has no comparable floor.

For investors who would otherwise build a self-directed ETF portfolio, the cost-driven argument favors public ETFs: our XEQT ETF review covers the all-in-one passive alternative, and the just buy XEQT framing addresses why the simplest answer often wins on a 30-year horizon when access to private markets is not the objective.

Is the Wealthsimple Summit Portfolio Worth It in 2026?

The Wealthsimple Summit Portfolio is a legitimate, regulator-disclosed, institutional-grade private market access vehicle for Canadian retail investors who would otherwise face accredited-investor paperwork or million-dollar minimums to reach LGT and Sagard. The question is fit, not legitimacy.

Strong fit for Summit:

- Long-horizon accumulators (10+ year time-to-need) at the Generation tier, where the 0.20%-0.40% advisory layer compresses the fee disadvantage and the all-in cost lands near 1.19% blended.

- Investors with strong income, no realistic need for the locked capital, and a meaningful preference for institutional-grade alternative access over self-directed liquid alternatives.

- Clients holding the allocation in registered accounts (RRSP/TFSA) where the phantom-distribution and forced-disposition tax frictions are fully shielded.

Different decision if you’d otherwise DIY:

- Cost-driven, long-horizon investors with realistic portfolio construction outside a managed wrapper. The 30-year compounding math favors low-cost ETFs by 35% to 40% on terminal wealth — but Summit’s value proposition is access to LGT and Sagard, not low-fee public-market beta. The two products answer different questions.

Different decision if you want 100% private exposure:

- The standalone Private Market Fund account delivers undiluted exposure to the same LGT + Sagard + IFM allocation without the 70% public ETF buffer. Standalone holders run the full 1.00% Wealthsimple PMF fee plus underlying manager fees on 100% of assets, where Summit holders run the same fee stack on only the 30% private sleeve and the cheaper public-ETF advisory rate on the 70% buffer. The fee architecture compounds differently on each route across a 10-year horizon.

Wealthsimple’s own self-disclosure on the Private Market Fund migration — “for most investors, total fees will be higher in the Private Market Fund than in the previous standalone funds. Wealthsimple has a financial interest in this migration, and we believe you should weigh that in your decision” — is the strongest credibility anchor on the product.

Summit and Generation are routinely confused: Summit is a managed product available across all client tiers; Generation is the $500K+ client tier. Our Wealthsimple Generation review covers the tier directly. For the broader tier economics that determine which Wealthsimple advisory rate applies to your Summit allocation, see our Wealthsimple Core vs Premium vs Generation comparison.

Sign-up bonus applied with our link.

Frequently Asked Questions

Is the Wealthsimple Summit Portfolio 47% richer claim true?

Yes. The math is consistent with Wealthsimple’s selected inputs: 0.44% Summit fee versus 1.85% legacy mutual fund fee at a 10% gross return over 30 years produces a roughly 47.5% terminal-wealth gap. The honest reframe is the comparison baseline. A 1.85% bank-channel mutual fund is a dying product, not the alternative most cost-conscious investors weigh today. The more relevant comparison for Summit’s actual audience is private-market alternatives — accredited-investor LPs at 2-and-20 with capital calls and 7-to-12-year lockups — where Summit’s monthly redemptions, $30,000 entry, and T3 tax slips win on access economics.

Do Wealthsimple Summit Portfolio performance fees apply if the fund loses money?

No. Performance fees only trigger when private sleeve returns exceed the hurdle rate — 5% annually for Sagard private credit, 8% annually for LGT private equity. In a year where returns fall below those thresholds, no carry is collected. The underlying base fees (1.25% Sagard, 1.50% LGT), the 1.00% Wealthsimple PMF management fee, and the tiered Wealthsimple advisory fee continue to apply regardless of performance. The 15% (Sagard) and 12.5% (LGT) performance layers are upside-only; the base layers run at all times.

Do RRSP or TFSA holders need to take any action for the June 2026 Wealthsimple Private Market Fund migration?

No. The migration is automatic and non-taxable for RRSP and TFSA accounts because registered-account exchanges are shielded from Canada Revenue Agency disposition rules. Wealthsimple handles the unit-for-unit conversion administratively. The May 20, 2026 opt-out deadline applies only to certain Private Equity holders in non-registered accounts. If you hold Summit only in registered accounts, no action is required and no 2026 tax slip is generated for the migration itself.

How long does it take to get money out of the Wealthsimple Summit Portfolio?

Public sleeve assets settle in 2 to 3 business days. Private sleeve redemptions process in monthly windows built around private-asset settlement, with payouts taking 30 to 60 days, capped at 5% of total fund value per month. If aggregate redemption requests exceed 5%, payouts fill pro rata and the manager can issue a non-transferable promissory note for 95% of the residual value with a maturity of up to two years. The monthly cap is intentional design: it prevents managers from holding return-destroying cash buffers or fire-selling underlying assets during market panics.

What returns has the Wealthsimple Summit Portfolio actually delivered since launch?

Wealthsimple’s published Private Credit performance reports a 22.6% net-of-fees cumulative return from the Sagard sleeve’s June 2023 inception through early 2026, with a 9.6% annualized distribution yield.18 The standalone Private Equity sleeve has reported a 52.7% cumulative return / 21.6% annualized since January 2024. Standalone Private Equity AUM has reached $434 million and standalone Private Credit AUM $387 million as of March 2026 per Wealthsimple’s official disclosure. After the June 2026 migration, the consolidated Private Market Fund reflects returns in NAV growth instead of cash distributions (final PC distribution paid June 30, 2026). These are sleeve-level returns from Sagard and LGT, and 18 to 24 months is too short a window to test structural risks over a full credit cycle. Treat the numbers as encouraging early data on manager execution.

Does the Wealthsimple Summit Portfolio include private infrastructure exposure after the June 2026 PMF migration?

Yes, indirectly through the PMF migration. Pre-June 2026, Summit’s private sleeve allocates only to LGT Capital Partners private equity and Sagard private credit. Post-June 2026, the private sleeve holds units of the unified Wealthsimple Private Market Fund, which targets a 40% private equity / 35% private infrastructure / 25% private credit allocation. Summit holders therefore gain a roughly 7% to 11% indirect infrastructure exposure (35% of the 20% to 30% private sleeve) after the migration — toll roads, regulated utilities, renewable generation, and data centers held through PMF’s open-ended infrastructure mandate.

How are Wealthsimple Summit Portfolio holdings taxed in a non-registered account?

Sagard private credit produces interest income at the full marginal rate; LGT private equity produces capital gains at the 50% inclusion rate. Summit reinvests distributions automatically rather than paying them out as cash, which creates a “phantom distribution” effect: T3 trust slip income owed in tax even though no cash was received. Investors must manually adjust the cost base each year to avoid double taxation on eventual sale. Quebec residents reconcile parallel federal T3 slips with provincial RL-3 (and RL-15 if any sleeve uses partnership structure), at combined federal-Quebec marginal rates that exceed 53% for high earners.

What is the minimum to open a Wealthsimple Summit Portfolio?

There are three thresholds, not one. The marketing page references $30,000 in investable assets as the entry point.4 The Help Centre adds a $50,000 minimum-liquid-assets check applied during the suitability assessment, which acts as a risk-capacity gate rather than a deposit floor.1 Once an account opens with $30,000, capital invests entirely in public ETFs until the account hits $10,000 in net deposits — the activation threshold for the private sleeve. Below that line, Summit holds public ETF exposure only.

What happens if my Wealthsimple Summit account drops below $10,000?

The private market sleeve may be removed until the account is re-funded above the threshold.1 If the balance falls below $10,000 after the private sleeve has activated, whether through withdrawal or market drawdown, Wealthsimple’s rebalancing engine triggers an automated liquidation of the private allocation during the next monthly window. The liquidation executes at the next monthly window NAV — a reality of any semi-liquid private-market wrapper, not a Summit-specific quirk.

At what return level would the Wealthsimple Summit Portfolio beat a self-directed XEQT account?

The XEQT comparison is a different decision than the Summit-vs-private-market-alternatives question Summit is built to answer. For an apples-to-apples accounting, Summit’s net-of-fee return must exceed XEQT’s by enough to overcome the roughly 1.19 percentage point fee gap between Summit’s blended Core-tier fee and XEQT’s 0.20% MER, which compounds to a 35-40% terminal-wealth disadvantage over 30 years. Whether the private sleeve’s illiquidity premium clears that hurdle is the empirical question. Summit’s value proposition is access to institutional managers at retail thresholds, not low-fee public-market beta.

Sources

Footnotes

Wealthsimple Help Centre — Open a Summit portfolio ↩ ↩2 ↩3 ↩4 ↩5

British Columbia Securities Commission — National Instrument 45-106 Prospectus Exemptions and Autorité des marchés financiers — Regulation 45-106 respecting Prospectus Exemptions ↩ ↩2

Wealthsimple Help Centre — About the Wealthsimple Private Market Fund — including direct disclosure: “For most investors, total fees will be higher in the Private Market Fund than in the previous standalone funds. Wealthsimple has a financial interest in this migration, and we believe you should weigh that in your decision.” ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7

BlackRock — Larry Fink’s 2025 Annual Chairman’s Letter to Investors ↩

Wealthsimple — Summit Portfolio Fee Savings Estimate (47% richer disclosure) ↩ ↩2

BXPE: Offering Terms | Blackstone Private Equity Strategies Fund, WealthManagement.com: Apollo Offers Private Investors Fee Bonus to Lock Up Capital, and iCapital: An Explanation of Private Market Fund Fees ↩

Investment Executive: Mackenzie introduces interval private credit fund, Ninepoint: Ninepoint-Monroe U.S. Private Debt Fund, and Investment Executive: BMO releases all-in-one private markets fund ↩

Hayley, S. and Sefiloglu, O. — “Biases in Private Equity Returns” (Bayes Business School, City University of London, 2022) ↩

Brav, A., Lakan, G., and Yafeh, Y. — “Private Equity and Venture Capital Fund Performance: Evidence from a Large Sample of Israeli Limited Partners” (Harvard Law School Forum on Corporate Governance, August 2023) ↩

Bernstein — In Private Credit, Illiquidity is a Feature, Not a Flaw ↩

IFM Investors — Infrastructure Capex Supercycle Set to Accelerate in 2026 and Infrastructure Investment & Asset Management ↩

Brookfield Infrastructure Partners — Q1 2025 Results Press Release ↩

Power Corporation of Canada — Wealthsimple announces $750 million equity offering (May 3, 2021) ↩

Sagard Holdings — Relationship Disclosure Information (July 2025) ↩

Wealthsimple Help Centre — Private Credit performance and Private Equity performance. ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.