Wealthsimple Business Account Review: $0 Fees, Tiered Interest, and What's Missing

Wealthsimple's business chequing pays up to 2.25% interest with zero monthly fees — but the rate depends on your total platform assets, not just your business balance.

Disclosure: This article contains referral links. Compensation may be received at no cost to you — this does not influence our analysis or recommendations.

TL;DR: The Wealthsimple Business Chequing Account is $0/month for Canadian-controlled private corporations (CCPCs) — with 1.25–2.25% tiered interest, unlimited e-Transfers, and free CRA tax payments. The rates are significantly higher than Big 5 banks (which pay 0%), but your actual rate depends on your total Wealthsimple assets across personal and corporate accounts. For now, there is no multi-signer approval and no sole proprietor support — and the announced USD Business account and Business Portfolio Line of Credit haven’t launched yet.

- Interest tiers: Core 1.25% (under $100K), Premium 1.75% ($100K–$499K), Generation 2.25% ($500K+)

- A CCPC with $50K in cash nets $313–$438/year vs losing $72 at a Big 5 bank

- Quebec businesses accepted — EQ Bank and Float exclude Quebec entirely

Launched March 19, 2026, the Wealthsimple Business Chequing Account is the first business chequing product from a major Canadian fintech.1 Not to be confused with the existing Wealthsimple corporate investing account (for holding stocks and ETFs inside a CCPC), this is a separate product built for daily operations. Looking past the $0 price tag, we look at the interest tiers, CDIC limits, and the integration gaps and limitations that matter to business owners.

Who Can Open a Wealthsimple Business Chequing Account?

The Wealthsimple Business Account is available to Canadian-controlled private corporations (CCPCs), CRA-registered charities, and CRA-registered associations — including professional corporations for doctors, lawyers, and consultants (PCs and APLPs).2 Physicians who already hold a Wealthsimple corporate investing account can add business chequing under the same login.

Professional corporations for doctors, lawyers, and consultants qualify — but the business must have a single layer of ownership with shares held directly by individuals.

The key eligibility constraint is “single layer of ownership”: shares must be held directly by individuals, not by a parent holding company. If your OpCo is owned by a HoldCo, the multi-layered structure disqualifies you — Wealthsimple’s automated onboarding cannot trace ultimate beneficial ownership through corporate layers.3

Excluded entity types: sole proprietorships, partnerships, strata/condominium corporations, multi-layered corporate structures (OpCo/HoldCo), non-Canadian corporations, and financial institutions.

Quebec businesses: Wealthsimple accepts businesses registered anywhere in Canada, including Quebec. This is a significant differentiator — both EQ Bank and Float Financial exclude Quebec businesses entirely.4 For Quebec-incorporated CCPCs, the Wealthsimple Business Account may be the only $0 business chequing option available from a fintech.

How Much Interest Does the Wealthsimple Business Account Actually Pay?

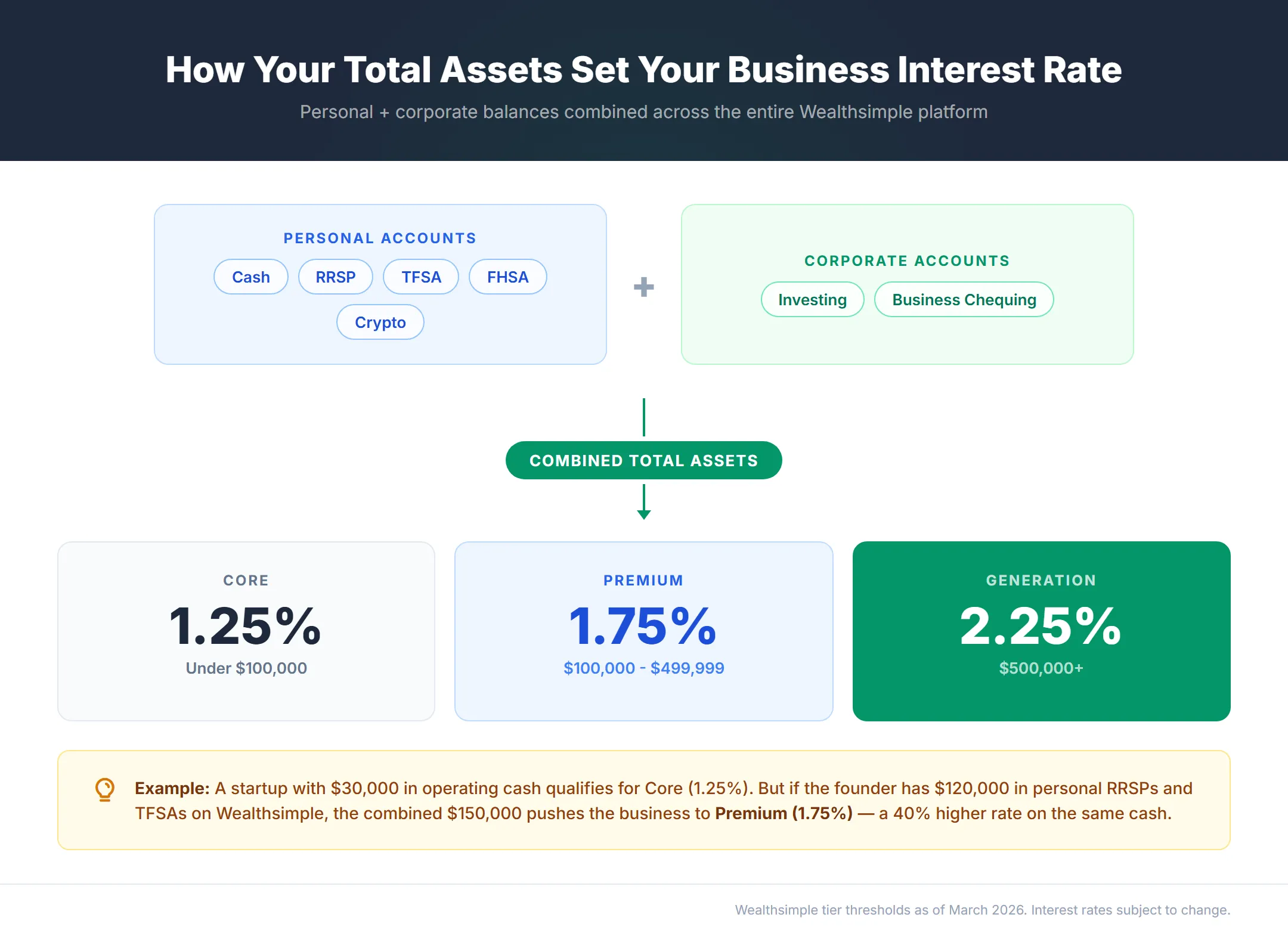

The Wealthsimple Business Account pays 1.25% to 2.25% interest, determined by your total assets across the entire Wealthsimple platform — not just your business balance.5 The rate you actually get depends on more than your corporate cash.

| Tier | Total Wealthsimple Assets | Business Chequing Rate |

|---|---|---|

| Core | Under $100,000 | 1.25% |

| Premium | $100,000–$499,999 | 1.75% |

| Generation | $500,000+ | 2.25% |

“Combined assets” includes everything: personal chequing, RRSPs, TFSAs, crypto holdings, AND corporate investment accounts. A lean startup with $30,000 in operating cash — but whose founder has $120,000 in personal registered accounts — qualifies for Premium (1.75%), not Core.

Core and Premium clients can earn an additional +0.5% by receiving $2,000 or more in eligible direct deposits within a rolling 30-day period. Generation clients are already at the cap — no further boost available. For a deeper breakdown of how these tiers work across all Wealthsimple products, see our Core vs Premium vs Generation comparison.

Practical reality: To get the advertised 2.25%, you need $500,000 across the platform OR $100,000+ with regular $2,000 direct deposits. EQ Bank offers a flat 2.25% regardless of your total financial profile — for low-capital businesses with no personal Wealthsimple accounts, EQ wins on yield alone.6

What Does the Wealthsimple Business Account’s $0 Monthly Fee Actually Include?

The Wealthsimple Business Account charges $0 per month with no minimum balance requirement, covering unlimited incoming wires, direct deposits, EFTs, unlimited Interac e-Transfers (up to $25,000/day), and all CRA bill payments.1 Note: you must manually configure a receiving email address for business e-Transfers in your account settings — they don’t automatically route to your personal Wealthsimple email.

Wealthsimple claims businesses save $230 per year compared to Big 5 banks. Their legal disclaimers show the methodology: an average entry-level business account assuming 12 Interac e-Transfers, 10 standard purchases, 3 cheque deposits, and 1 CRA tax payment per month.7

Costs that do exist:

- Outbound domestic wire: $15 flat (competitive — Big 5 charge $30–$50)

- Incoming USD payments: forced conversion to CAD at up to 1.5% FX spread (no native USD holding today; a USD Business account with no monthly fee was announced May 21, 2026 — launch date TBD)

Year One: What a CCPC Actually Saves

The $230 claim only covers fee avoidance. The real comparison includes interest earned on operating cash that Big 5 banks pay 0% on:

| Big 5 ($6/mo, 0% interest) | WS Core (1.25%) | WS Premium (1.75%) | |

|---|---|---|---|

| Monthly fees | -$72/year | $0 | $0 |

| Interest on $50,000 | $0 | +$625 | +$875 |

| Tax on interest (~50%) | — | -$313 | -$438 |

| Net Year One benefit | -$72 | +$313 | +$438 |

A CCPC with $50,000 in operating cash nets $313–$438 in Year One at Wealthsimple versus losing $72 at a Big 5 bank.8 That’s the gap between earning 50% of something and earning 100% of nothing.

Can You Pay CRA Corporate Taxes Directly from a Wealthsimple Business Account?

Yes — corporate income tax (T2), GST/HST remittances, and payroll deductions (CPP, EI, income tax withheld) can all be paid directly through the Wealthsimple bill pay feature.9 Search for CRA payees using your 15-digit federal business number (e.g., 123456789RC0001), and payments can be scheduled in advance for the full fiscal year.

All CRA payments are free. Big 5 banks charge $1.50–$2.00 per bill payment transaction — a CCPC making monthly GST/HST remittances plus quarterly installments saves $20–$30/year on CRA payments alone.10

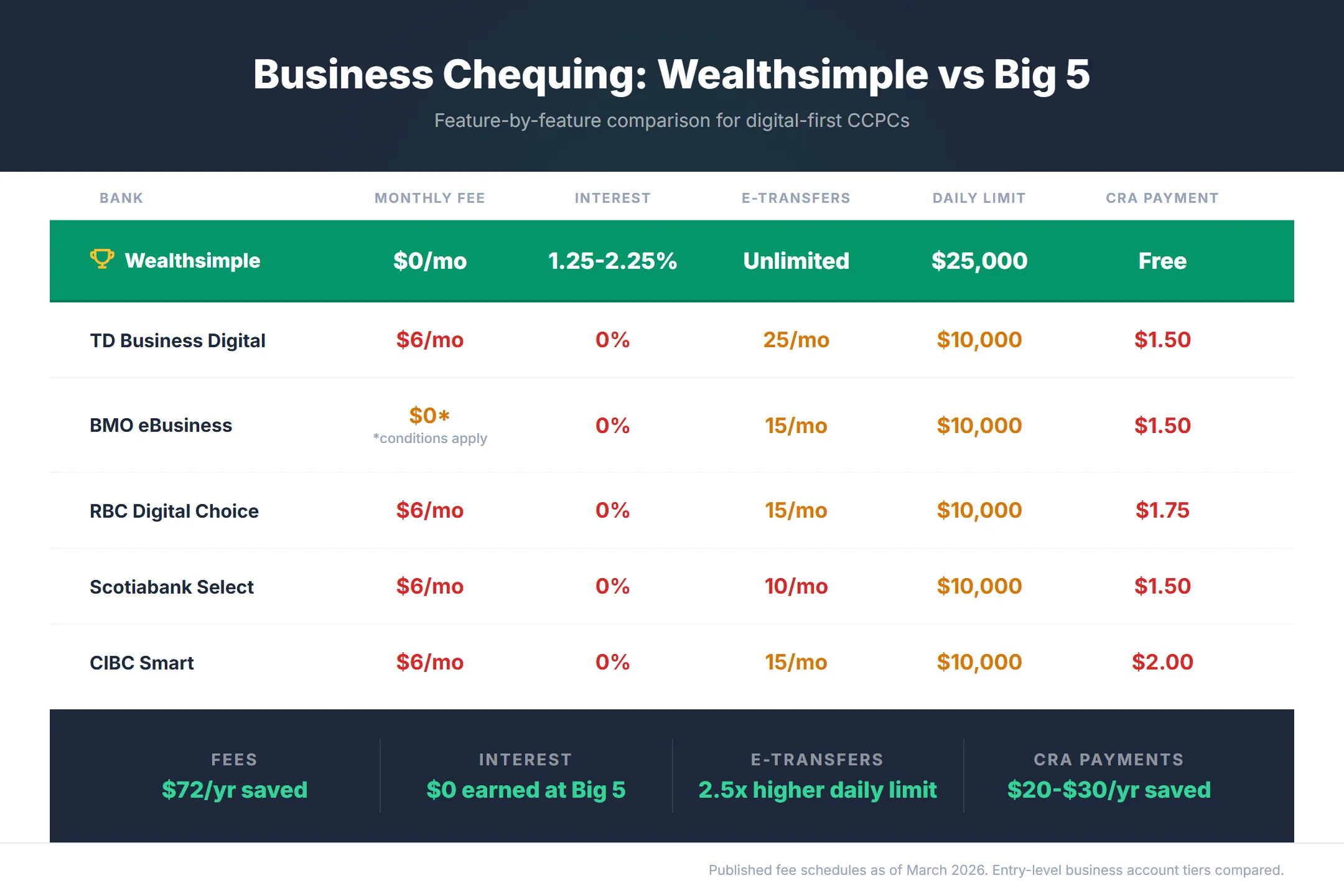

How Does the Wealthsimple Business Account Compare to Big 5 Banks in 2026?

The Wealthsimple Business Account eliminates the core costs of Big 5 business banking — monthly fees, per-transaction charges, and the 0% interest that makes operating cash a dead asset. For digital-first CCPCs that don’t need branch access, the comparison is decisive.

The banks don’t do this because it harms them, and they’re unwilling to cannibalize existing businesses and existing workflows.11

— Jeremy Black, VP of Product at Avara, on why traditional banks haven’t matched fintech pricing.

| Feature | Wealthsimple | TD Business Digital | BMO eBusiness | RBC Digital Choice | Scotiabank Select | CIBC Smart |

|---|---|---|---|---|---|---|

| Monthly fee | $0 | $6 | $0* | $6 | $6 | $6 |

| Interest on chequing | 1.25–2.25% | 0% | 0% | 0% | 0% | 0% |

| e-Transfers included | Unlimited | 25/mo | 15/mo | 15/mo | 10/mo | 15/mo |

| e-Transfer daily limit | $25,000 | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| CRA bill payments | Free | $1.50 | $1.50 | $1.75 | $1.50 | $2.00 |

| Branch access | None | Yes | Yes | Yes | Yes | Yes |

| Cash deposits | None | Yes | Yes | Yes | Yes | Yes |

| Credit products | None | Yes | Yes | Yes | Yes | Yes |

*BMO eBusiness waives fee with conditions but offers limited transactions.

Where Wealthsimple wins clearly: fees ($0 vs $5–$7/month), interest (any percentage vs 0%), e-Transfer volume (unlimited vs capped), CRA payment costs (free vs $1.50–$2.00), and daily e-Transfer limits ($25,000 vs $10,000).

Where Big 5 banks still win: physical branches for cash deposits (retail, restaurants), in-person service, business credit cards and commercial lending, and multi-signer approval workflows. If your CCPC handles cash or needs traditional credit products, a Big 5 account remains necessary — at least as a secondary account alongside Wealthsimple for digital operations. Wealthsimple’s announced Business Portfolio Line of Credit (Prime −0.5%, as low as 3.95%) will narrow the credit gap when it launches, though no date has been confirmed.

What Makes Wealthsimple’s Business Account Different from Other Fintechs?

Wealthsimple is the only platform that combines business chequing with corporate self-directed investing, managed portfolios, and personal registered accounts (RRSP, TFSA, FHSA) under one login. No other fintech offers this integration — EQ Bank is banking-only, Venn and Float are operations-only. If you already hold a personal Wealthsimple Cash account, those balances count toward your total assets — adding business chequing means your combined personal and corporate holdings push you closer to the 2.25% Generation rate.

EQ Bank offers a flat 2.25% interest regardless of total assets — but excludes Quebec entirely.6 Venn pays a flat 2% on both CAD and USD balances with multi-currency accounts — but is a smaller, newer platform without investing integration. Float advertises up to 4% interest — but that headline rate requires significant monthly corporate card spend that most CCPCs won’t hit.12

For most CCPCs already on Wealthsimple, the ecosystem advantage outweighs the yield gap. Your total assets across personal and corporate accounts — from personal RRSPs to corporate investments — determine your tier, and every dollar you consolidate pushes you toward the 2.25% Generation rate.

What Can’t You Do with a Wealthsimple Business Account Yet?

The Wealthsimple Business Account has meaningful gaps that affect specific business types — and understanding them matters more than the $0 price tag.

No sole proprietor support. This is the most-requested missing feature. Only incorporated entities (CCPCs, charities, associations) qualify. Sole props, partnerships, and freelancers are excluded.

No USD account today — but one is coming. Incoming USD payments are force-converted to CAD at up to a 1.5% FX spread — on a $10,000 USD invoice that’s up to $150 in conversion cost. Wealthsimple announced a USD Business account at its May 21, 2026 Presents event (no monthly fee, no cross-border transfer fees, USD interest, US payment rails), but launch date is TBD. Until it ships, the workaround is Wise Business or Venn for USD holding and distribution.13

No multi-signer or dual authorization. Any authorized director has full unilateral access. There is no approval workflow for large payments — if your corporate governance requires a preparer/approver model (e.g., a bookkeeper sets up a vendor payment, a director signs off), you cannot execute that workflow here. This limits the account to single-founder access models for now.

Unified login with personal accounts. There is no separate login for your business account — it shares your existing personal Wealthsimple credentials. Web has Personal/Business tabs (added March 2026), but the mobile app does not. This means anyone with business account access — including a bookkeeper or accountant — sees your personal RRSP, TFSA, and crypto balances. For founders who delegate bookkeeping, handing over credentials means giving full visibility into your personal net worth. Wealthsimple announced an Authorized Traders feature for Summer 2026 that lets you delegate trading authority on specific accounts without sharing passwords — useful for a spouse or CFO who needs to execute trades, but permission-scoped at the account level. It does NOT solve the bookkeeper-visibility gap above: full-login access still exposes personal balances.

No trust accounts for professionals. If you are a lawyer or real estate professional who needs to hold client funds in a formal trust, Wealthsimple cannot support this structure yet. You will still need a Big 5 bank for trust operations.

Where Are the Wealthsimple Business Account’s Integration Gaps?

Accounting integration is still being refined. QuickBooks Online and Wave connect via Plaid, but early users report intermittent failures — connections establish but pull no data. Xero has no integration at all. Third-party aggregators (Monarch Money, YNAB) report auth breaks and 2FA loops when syncing business chequing.14 These are launch-period growing pains — Wealthsimple has historically improved integrations within the first few months of a product release. Until the native connection stabilizes, the workaround is waiting for your end-of-month statement, exporting the CSV manually, and formatting it for a bulk QuickBooks import.

CSV exports need manual cleanup for now. Transaction exports strip counterparty names, replacing transfers with opaque codes like “TRFOUTTF” and “WD.” Importing into QBO’s required Date/Description/Amount format means manual scrubbing or Power Query templates until Wealthsimple improves the export format.

CDIC coverage at $100,000. Wealthsimple is not a chartered bank — it operates as a broker (Wealthsimple Investments Inc.) and money services business (Wealthsimple Payments Inc.), sweeping deposits into pooled trust accounts at Tier 1 CDIC-member banks. CDIC protects against partner bank failure, but not against ledger corruption at Wealthsimple’s level — a distinction that matters after the US Synapse/Evolve collapse froze customer funds in a similar pooled trust model.15 The $1 million multi-institution sweep available on personal chequing does not apply to business accounts.

Cheque deposits are mobile-only with friction. You can deposit cheques via the Wealthsimple app (no desktop option) up to $1,000,000 per day, but an algorithmic “instant deposit limit” varies per user — amounts above your invisible threshold face 4-8 business day holds. Cheques made out to the director (not the corporation) require exact endorsement syntax or they’re automatically rejected. USD cheques are prohibited entirely.16

Business Visa card coming — but it’s prepaid. The upcoming business Visa (Spring 2026) with 1% cashback draws from your chequing balance — a network shift from Mastercard (personal card) to Visa (business). It is not a credit card — no float, no working capital leverage. A separate Business Portfolio Line of Credit (announced May 21, 2026, launch TBD) lets you borrow against your corporate investment portfolio at rates as low as Prime −0.5% (3.95%) — extending the credit facility Wealthsimple has lacked, though it isn’t integrated with the business Visa.

How Do You Open a Wealthsimple Business Account?

Opening a Wealthsimple Business Account takes approximately 20 minutes for single-director CCPCs and uses your existing personal Wealthsimple login — no separate credentials needed.17

Required documents:

- Articles of Incorporation

- 9-digit CRA business number

- Personal ID for the Authorized Person (the director completing setup)

Multi-director setups face a delayed manual review with DocuSign verification — same-day onboarding is not guaranteed. Only the Authorized Person can open sub-accounts or link external banks after setup. If Plaid or Flinks fails to auto-connect your external business bank, manual linking requires a void cheque and takes 1-3 business days for Wealthsimple’s team to review before pending deposits can process.

The Wealthsimple Business Account is still technically in beta for some configurations. Simple single-director CCPCs get the streamlined experience. Multi-director structures or less common entity types (charities, associations) may encounter a waitlist or additional verification steps.

Can You Use a Referral Code for a Wealthsimple Corporate Account?

The standard Wealthsimple referral terms don’t explicitly exclude corporate entities — your corporation is a distinct legal entity that has never had a Wealthsimple account, even if you personally have been a client for years. The standard Wealthsimple referral terms use the word “individual” and require “age of majority,” but do not explicitly exclude corporate entities. The anti-gaming clause does not mention controlled entities, and the “Wealthsimple for Business” exclusion applies only to the Affiliate Program — not the standard referral program.18

The referral code 9C6DMQ gives your corporation a cash bonus on its first qualifying deposit. If you’ve already funded your business account, you may still be able to add a referral code after signup.

Frequently Asked Questions

Does the Wealthsimple Business Account work in Quebec?

Yes. Wealthsimple accepts businesses registered anywhere in Canada, including Quebec. EQ Bank and Float Financial both exclude Quebec businesses entirely, making Wealthsimple potentially the only $0 business chequing option for Quebec-incorporated CCPCs. The one caveat: Wealthsimple does not support Revenu Quebec payments (provincial corporate tax, QST) — only federal CRA payments.

Does the Wealthsimple Business Account support sole proprietors?

No. The Wealthsimple Business Account requires incorporation — only CCPCs, CRA-registered charities, and CRA-registered associations qualify. CRA does not mandate a formal “business” bank account for sole proprietors — just accurate segregation of business transactions. Using Wealthsimple Cash for business is technically fine for tax purposes, but it violates Wealthsimple’s User Agreement, which restricts personal accounts from commercial use. Low-volume service-based freelancers are unlikely to be flagged, but high-velocity e-commerce sole props risk compliance action.

Is the Wealthsimple Business Account covered by CDIC?

Yes, up to $100,000 per beneficiary through CDIC-member partner banks. Wealthsimple sweeps deposits into pooled trust accounts at Tier 1 banks. This is the standard CDIC limit — the $1 million multi-institution sweep available on personal chequing does not apply to business accounts.

Does CRA recognize Wealthsimple for corporate tax payments?

Yes. Corporate income tax (T2), GST/HST remittances, and payroll deductions can all be paid through Wealthsimple’s bill pay feature using your 15-digit CRA business number. All CRA payments are free.

Can you connect a Wealthsimple Business Account to QuickBooks?

Yes, but with caveats. QuickBooks Online and Wave connect via Plaid aggregator. Users report intermittent sync issues — connections establish but sometimes pull no transaction data. Xero has no Wealthsimple integration. All other accounting platforms require manual CSV import.

What is the difference between a Wealthsimple corporate account and business chequing?

Two separate products. The Wealthsimple corporate investing account holds stocks, ETFs, and bonds inside a CCPC. The Business Chequing Account (launched March 2026) handles daily operations — receiving payments, paying bills, managing cash. You can have both under one login, and combined assets across both determine your interest tier.

Does earning interest in a CCPC trigger the small business deduction grind?

Only at extreme balances. Passive income above $50,000 reduces the Small Business Deduction, but hitting $50,000 from Wealthsimple interest at 2.25% requires $2,222,222 in average daily balance. Interest earned inside a CCPC is taxed at approximately 50%, partially mitigated by the RDTOH mechanism when dividends are paid out. For most CCPCs, the SBD grind from chequing interest is not a realistic concern.

Can the Wealthsimple Business Account handle payroll?

Not directly. Wealthsimple has no native payroll engine. It integrates as a funding source for Wagepoint, ADP, Humi, Dayforce, and Rippling — these platforms pull funds from the Wealthsimple Business Account to distribute employee direct deposits.

Is there a separate login for Wealthsimple business vs personal?

No. The business account shares your existing personal credentials. Personal/Business tabs were added on the web in March 2026, but the tab separation has not been ported to iOS or Android. Anyone with business access sees personal balances (RRSP, TFSA, crypto).

When is the Wealthsimple Business Visa card coming?

Spring 2026 — no exact date confirmed. It will be a prepaid Visa (not credit) with 1% cashback on eligible purchases, $0 annual fee, and zero FX markup on cross-border transactions. The card draws from your chequing balance — there is no credit facility.

How much do businesses actually save switching from Big 5 to Wealthsimple?

$313–$438 in net Year One benefit for a CCPC holding $50,000 in operating cash (Core or Premium tier), compared to losing $72/year at a Big 5 bank paying 0% interest with $6/month fees. The gap widens with larger balances.

Does the Wealthsimple Business Account support multi-signer approval for payments?

No. There is no dual authorization or multi-signer workflow. Any authorized director has full unilateral access. No official roadmap date has been announced for multi-tier approval workflows.

Sources

Footnotes

Wealthsimple — Open a Business chequing account. Product features and fee structure confirmed via help center documentation. ↩ ↩2

Based on Wealthsimple help center eligibility requirements and “single layer of ownership” disclosure for business accounts. ↩

EQ Bank terms exclude Quebec residents from business products. Float Financial terms restrict service to provinces outside Quebec. Confirmed via product pages as of March 2026. ↩

EQ Bank Business Account offers flat 2.25% interest with no tiering. Comparison based on published rates as of March 2026. ↩ ↩2

Wealthsimple — Legal Disclaimers. $230 savings methodology based on average Big 5 entry-level business account fees. ↩

Year One projection based on published Wealthsimple interest rates and Big 5 monthly fees as of March 2026. Tax calculation uses combined federal/provincial corporate passive income rate of approximately 50%. ↩

Canada Revenue Agency — Pay taxes online through your financial institution ↩

Big 5 bill payment fees based on published standard business account fee schedules for TD, BMO, RBC, Scotiabank, and CIBC as of March 2026. ↩

BetaKit — Wealthsimple reveals first credit card, expanded chequing account at inaugural product showcase. Jeremy Black, VP of Product at Avara, on why traditional banks can’t compete on innovation. ↩

Float Financial interest rate tiers based on published rate card. The 4% headline rate requires meeting minimum monthly corporate card spend thresholds. ↩

Wealthsimple FX conversion spread based on user reports and help center documentation for incoming USD wire handling. ↩

QuickBooks and CSV integration issues compiled from r/Wealthsimple and r/SmallBusinessCanada user reports, March 2026. ↩

CDIC — Deposits held in trust. Business deposits insured up to $100,000 per beneficiary per CDIC-member institution. ↩

Wealthsimple — Deposit a cheque or bank draft. Mobile-only deposit, endorsement requirements, and instant deposit limit details from Finding your instant deposit limit. ↩

Setup time and process based on user reports from r/PersonalFinanceCanada (667 upvotes, 184 comments) and Wealthsimple help center documentation. ↩

Wealthsimple — Referral Bonus Promotion 2026. Terms use “individual” and “age of majority” language without explicit corporate entity exclusion. Affiliate Program terms (separate document) exclude Wealthsimple for Business — standard referral does not. ↩

About the Author

Isabelle Reuben is a specialized finance writer focused on Canadian investment platforms and bonus optimization. With 5+ years tracking robo-advisors, she stress-tests Wealthsimple's features to transform fine print into actionable blueprints.